Image: Bigstock

The market’s performance has been stellar as of late. After a rough start in the first half, investors have undoubtedly welcomed the rally with open arms. The ongoing war in Ukraine, rising costs, and a hawkish Fed have all been components of the dark fiscal cloud hovering above us.

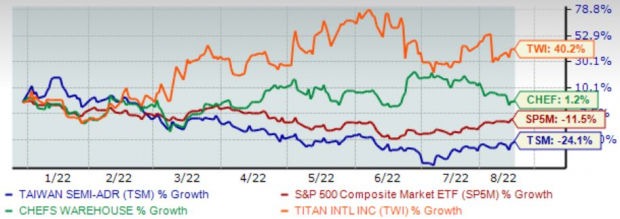

With buyers reappearing, a few highly-ranked stocks with excellent growth prospects that could take off include Titan International (TWI - Free Report) , Taiwan Semiconductor Manufacturing (TSM - Free Report) , and The Chefs’ Warehouse (CHEF - Free Report) .Below is a year-to-date chart of all three companies while blending in the S&P 500 as a benchmark.

Image Source: Zacks Investment Research

All three companies sport the highly-coveted Zacks Rank #1 (Strong Buy). Let’s take a closer look at each company’s growth prospects and a few other aspects a little closer.

Taiwan Semiconductor Manufacturing

Taiwan Semiconductor Manufacturing (TSM - Free Report) , the world’s largest circuit foundry, is responsible for supplying microchips globally to an elite list of companies, including Nvidia (NVDA - Free Report) and Advanced Micro Devices (AMD - Free Report) .

The company has stellar growth prospects, and analysts have been bullish across all timeframes over the last 60 days.

Image Source: Zacks Investment Research

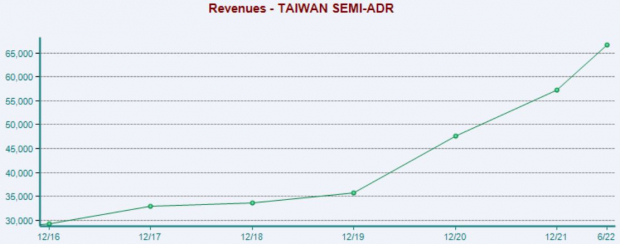

TSM is forecasted to generate a mighty $78 billion in revenue in FY22, penciling in a rock-solid 37% year-over-year uptick. And in FY23, the top-line looks to add an additional 15%. Below is a chart illustrating the company’s revenue on an annual basis.

Image Source: Zacks Investment Research

Bottom-line projections are also rock-solid; the Zacks Consensus EPS Estimate of $6.30 for FY22 reflects a massive 53% year-over-year increase in earnings. Furthermore, the bottom-line looks to tack on a respectable 3.5% in FY23.

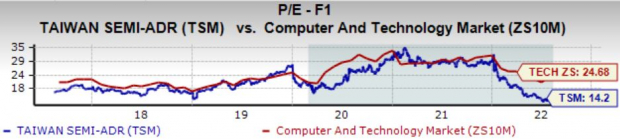

TSM’s valuation levels sit enticingly as well. Its 14.2X forward earnings multiple is nowhere near its five-year median of 19.9X and represents a steep 42% discount relative to its Zacks Sector.

Image Source: Zacks Investment Research

Titan International

Titan International (TWI - Free Report) globally produces a broad range of products to meet original equipment manufacturers' specifications (OEMs) and aftermarket customers in the agricultural, earthmoving/construction, and consumer markets.

Analysts have substantially raised their earnings outlook across all timeframes.

Image Source: Zacks Investment Research

Top-line growth projections are remarkable – Titan’s annual revenue is forecasted to climb to $2.2 billion in FY22, reflecting a substantial 24% year-over-year increase. In FY23, the company’s top-line looks to add an extra 4% of growth.

Below is a chart illustrating the company’s revenue on an annual basis.

Image Source: Zacks Investment Research

For the current fiscal year, the company’s bottom-line is projected to skyrocket – the Zacks Consensus EPS Estimate of $2.19 pencils in a staggering 157% triple-digit year-over-year uptick. And in FY23, the bottom-line is forecasted to expand an additional 5.3%.

In addition to inspiring growth prospects, the company also rocks solid valuation levels. Titan’s 0.4X forward P/S ratio resides on the low side and represents a deep 81% discount relative to its Zacks Sector.

Image Source: Zacks Investment Research

The Chefs’ Warehouse

The Chefs' Warehouse (CHEF - Free Report) is a distributor of specialty food products in the United States, focused on serving the specific needs of chefs who own and/or operate restaurants, fine dining establishments, country clubs, hotels, caterers, culinary schools, and specialty food stores.

Like TSM and TWI, analysts have substantially raised their earnings outlook across all timeframes.

Image Source: Zacks Investment Research

Look out, as the Zacks Consensus EPS Estimate for FY22 of $1.36 reflects a mind-boggling 2,820% year-over-year bottom-line expansion. The next fiscal year’s earnings are forecasted to climb an additional double-digit 16%.

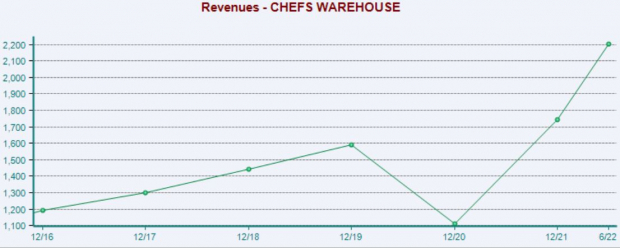

Of course, the growth doesn’t stop there – CHEF is forecasted to generate a strong $2.5 billion in revenue throughout FY22, good enough for a rock-solid 40% year-over-year uptick. And in FY23, the revenue projection of $2.7 billion pencils in an additional 10% uptick.

Image Source: Zacks Investment Research

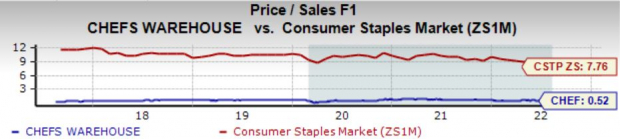

CHEF’s forward price-to-sales ratio resides at 0.5X, just below its five-year median value of 0.6X. Still, the value represents a deep 93% discount relative to its Zacks Sector. In addition, the company sports a Style Score of a B for Value.

Image Source: Zacks Investment Research

Bottom Line

The market’s rebound as of late has been remarkable. After a brutal start to the year, we’re finally seeing some consistent green, and investors are ecstatic.

Of course, in times when the market is roaring, investors want to have strong stocks in their portfolios. All three companies above sport a Zacks Rank #1 (Strong Buy) and have rock-solid growth prospects, making them perfect for investors who target growth.

More By This Author:

Bull Of The Day: TTM Technologies

Illumina Q2 Earnings and Revenues Lag Estimates

4 Large-Cap Value Mutual Funds For A Stable Portfolio

Comments

Log in or sign up to join the conversation.