Image: Bigstock

The stock market took a much-needed breather from buying this week, and there could be more selling in the near-term considering the massive run the S&P 500 and the Nasdaq went on during the first five weeks of 2023.

The overall upbeat market action appears to be based in large part on the premise that the Fed’s inflation battle is essentially won and earnings will bottom out in short order.

The bullish start to the year is fantastic, and more investors are likely on the hunt for stocks to buy in February and throughout 2023. It is certainly time for long-term investors to reevaluate their portfolios and possibly get back in on the growth names that fell out of favor in 2022.

Instead of focusing on Tesla and other beaten-down growth names, especially after the wild year-to-date climb, a more prudent approach might be to buy stocks poised to thrive even if the U.S. economy doesn’t reach that goldilocks zone everyone is hoping for.

Today, we will dig into three highly-ranked stocks that outperformed the market in 2022 amid the turmoil and are primed to keep running higher in 2023, even if Wall Street is forced to take its foot off the growth pedal.

McKesson Corporation (MCK - Free Report)

McKesson is a healthcare products distributor that benefited both from the COVID-19 pandemic and a return to normalcy as more people start receiving regularly scheduled medical care, screenings, and more. McKesson partners with hospitals, doctors’ offices, pharmacies, manufacturers, and beyond to help deliver medicines, medical products, and healthcare services to consumers.

McKesson grows alongside the overall expansion of healthcare, pharmaceuticals, biotech, and medical products without having to undertake the massive amounts of research and development that many of the innovators in the space do. McKesson is the largest of the three major drug distributors in the U.S. alongside AmerisourceBergen and Cardinal Health. MCK has posted over 20 straight years of sales growth outside of one tiny (-0.1%) pullback.

Image Source: Zacks Investment Research

McKesson topped Zacks Q3 FY23 estimates on Feb. 1 and provided upbeat EPS guidance to help it land a Zacks Rank #2 (Buy) rating. Zacks estimates call for its sales to climb 4.3% in FY23 and another 4% in FY24 to $286 billion to help lift its adjusted earnings by 8% and 3%, respectively. MCK also lands an “A” VGM grade, and its industry is in the top 12% of over 250 Zacks industries.

McKesson shares have soared roughly 1,300% over the past 20 years vs. the S&P 500’s 395%. MCK has also jumped 100% in the past two years to destroy the benchmark’s 4% downturn and its industry’s 3% gain. MCK stock is up 35% in the last 12 months, yet it trades 18% below its average Zacks price target.

Wall Street is high on MCK stock and for good reason, with it recently trading near its own 10-year median and at a 25% discount to its industry despite its massive outperformance at 13.7X forward earnings. Also, its dividend yields 0.6%.

Jabil (JBL - Free Report)

Jabil provides manufacturing services with a client list that includes the likes of Apple, SolarEdge, and other giants in critical and game-changing industries. JBL has been a somewhat under-the-radar tech superstar during the last five years.

Jabil prides itself on operating in the background, working with hundreds of the biggest brands in the world to help make everything from smartphones and home appliances to healthcare tech. JBL is also set to benefit from a broader onshoring/reshoring push from U.S. companies and the federal government.

Jabil’s diversification has helped it grow steadily for years, including 14% growth in its fiscal 2022. Most recently, JBL topped our Q1 FY23 estimates in mid-term December, and it upped its guidance once again.

Image Source: Zacks Investment Research

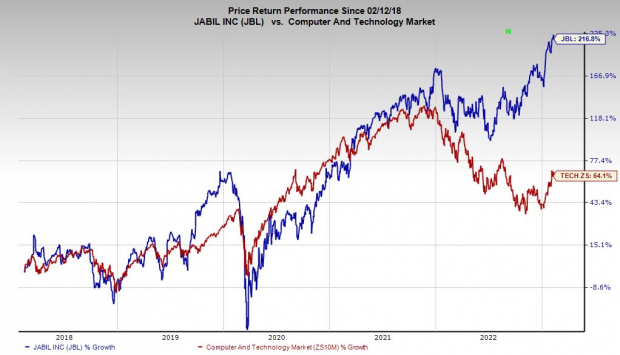

JBL stock has soared 215% over the last five years vs. the benchmark’s 55% and the Zacks Tech sector’s 64%. This run includes an 83% surge in the last 24 months as Tech tumbled 17%. Jabil has also managed to outpace tech in 2023 (up 20% year-to-date vs. 15%) to trade near fresh records.

Jabil’s valuation levels are somewhat stunning considering its outperformance. JBL trades at a 55% discount to the Zacks Tech sector at 10.1X forward 12-month earnings and 14% below its own 10-year median and 45% under its highs.

Zacks estimates call for JBL’s revenue to climb 3% in both FY23 and FY24 to hit $35.4 billion. This growth comes on top 12% average sales expansion over the last five years. Jabil’s adjusted earnings are projected to climb by over 9% and 6%, respectively.

JBL’s bottom-line positivity helps it land a Zacks Rank #1 (Strong Buy) rating. Jabil’s Electronics - Manufacturing Services segment is in the top 15% of all of the Zacks industries, and six of the seven brokerage recommendations Zacks has are “Strong Buys.” Also, Jabil pays a dividend.

Halliburton (HAL - Free Report)

Halliburton is an oil field services standout that works throughout the entire life cycle of a project. Halliburton’s products and offerings help oil and gas companies with everything from exploration and well construction all the way to abandonment activities. The entire oil and energy sector benefited from soaring prices last year, and oil prices are holding up better than some expected even though they are well off their records.

The ongoing Russian invasion has greatly disrupted global oil and gas supplies. More importantly, fighting and the sanctions have forced a reevaluation of the status quo. Oil exploration and drilling are gradually expanding after years of slowing output as more countries race toward greater energy independence, all of which is music to Halliburton’s ears.

Perhaps most importantly for near-term and long-term investors, oil is without a doubt going to play a vital role in the U.S. and around the world for years to come, even as alternative and renewable energy booms. Halliburton topped our EPS estimate once again on Jan. 24 and raised its outlook, with HAL executives calling for its “earnings power to strengthen in 2023 and beyond.”

Image Source: Zacks Investment Research

Zacks estimates call for Halliburton’s FY23 sales to climb 16% and another 11% in FY24 to $26.14 billion. Plus, its adjusted earnings are projected to soar by 43% this year and 22% in FY24.

This outlook showcases its growth runway, stability, and niche within the oil sector as many face a pending downturn after a blowout year. And Halliburton posted 33% revenue growth in 2022 and 99% adjusted earnings expansion.

Halliburton’s upward earnings revisions help it to land a Zacks Rank #2 (Buy) rating. HAL’s industry ranks in the top 32% of over 250 Zacks industries, and it recently raised its dividend by 33% to $0.16 per share. The stock sports an overall “A” VGM grade, and 13 of the 15 brokerage recommendations Zacks has are “Strong Buys,” alongside two “Buys.”

Halliburton stock has soared 99% in the past two years to blow away the Zacks Oil and Energy sector’s 55%. HAL shares have jumped 30% in the past six months, and they still trade 35% below their average Zacks price target at around $39 per share. On the valuation side, HAL trades at a 15% discount to its industry at 11.8X forward earnings. This also marks a 20% discount to its own five-year median.

More By This Author:

Bear Of The Day: 3M CompanyMeta And Amazon Earnings: Time To Buy These Beaten-Down Tech Stocks?

2 Market-Crushing Value Stocks To Buy For More Growth In 2023

Comments

Log in or sign up to join the conversation.