The ‘Everything Trade’

Expectations for a (relatively) calm, the upward-grinding market did not disappoint.

A bit over a month ago in a note called $20 ANOTHER BEAR MARKET RALLY? I underscored how technical (i.e., investor positioning, options positioning, corporate buyback flows, seasonality and midterms) and fundamental (i.e., earnings season and monetary policy / Fed) factors were conspiring for a “tactically constructive [view] on risk” leading me to “favor this outcome (bounce) in the short term”. S&P is up almost 5% since, VIX down ~20%.

That same note provided color on what would happen once markets sniffed out “peak inflation”:

The infamous ‘Fed pivot’ narrative (i.e., deceleration / pause in hiking, lower terminal rate or rate cuts / end of QT soon after terminal) could take off again, should peak inflation be re-established. […] If terminal rate peaks, […] it will drive what I call ‘The Everything Trade’ (i.e., long bonds, short USD, long equities, long gold).

It was followed up with an explainer of the ‘Everything Trade’ that would follow terminal rates peaking, including when to historically expect this / what to look for:

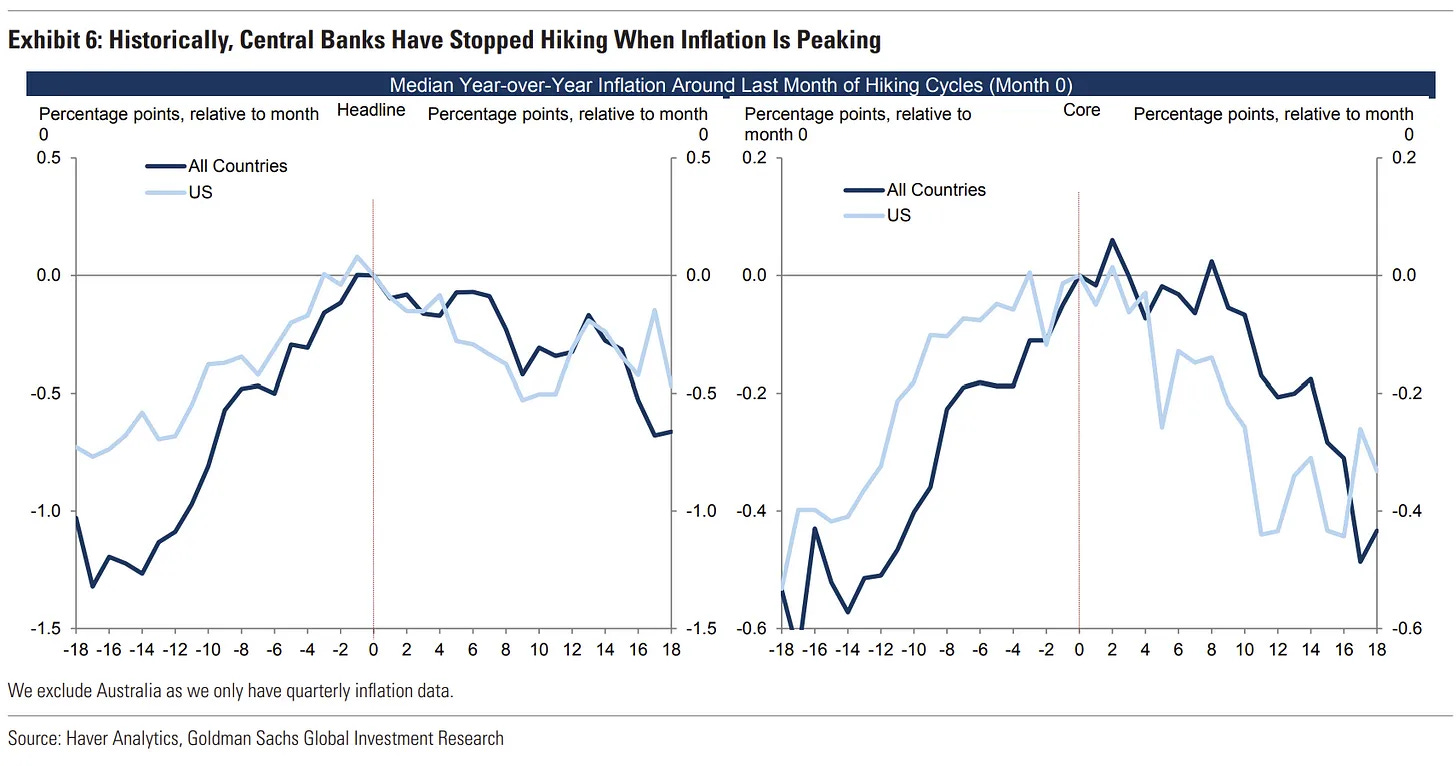

CBs often stop hiking around the same time—at / close to the peak in headline and core inflation (YoY)—and anticipate substantial declines in inflation by several months.

Source: Goldman Sachs

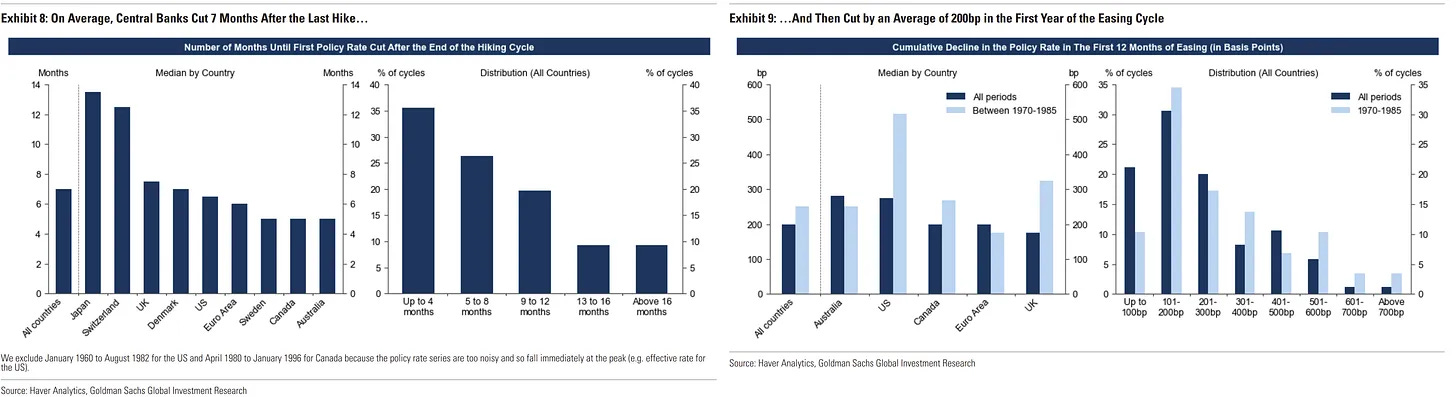

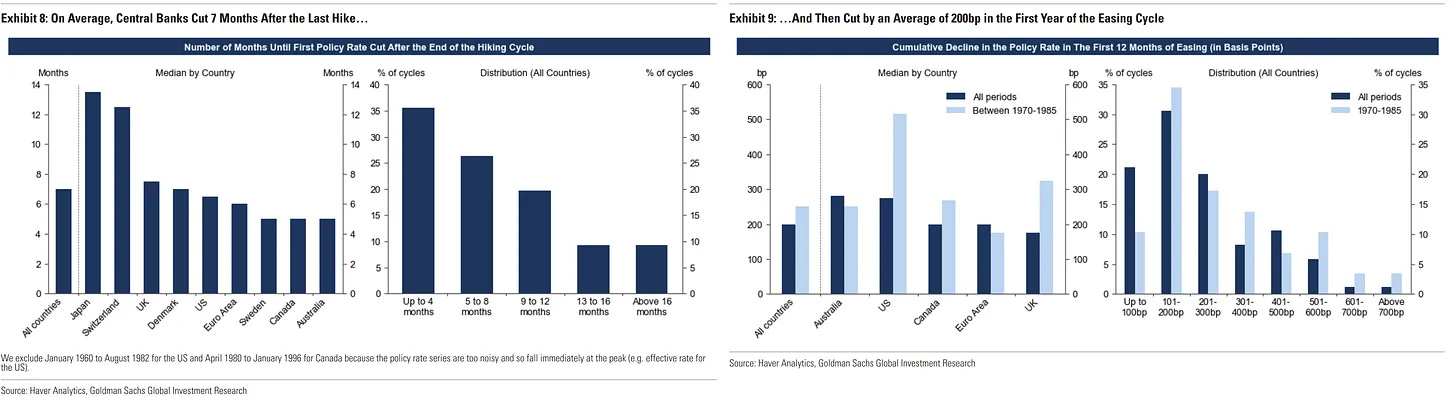

In 75% of cycles CBs cut within the first year since the last hike. Cuts generally arrive arrive 5-7 months from that last hike and average 200bps, with Canada and Australia generally leading the cutting cycle timing-wise. Inflationary periods exhibit only slightly larger cuts over the first year, despite averaging double the cumulative hikes.

(Click on image to enlarge)

Source: Goldman Sachs

Read more: $21 THE ‘EVERYTHING TRADE’

Source: Goldman Sachs Source: Goldman Sachs

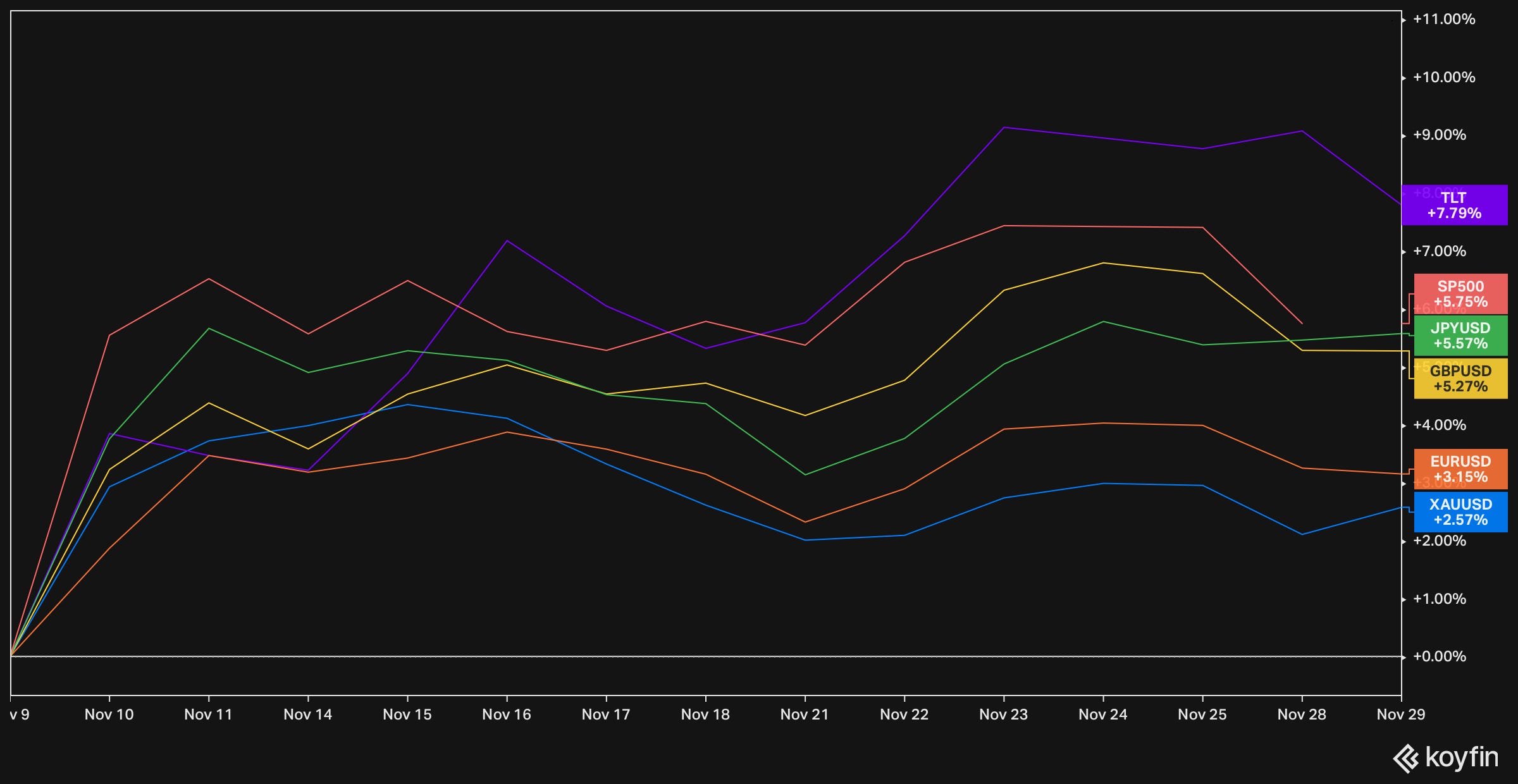

Enter October’s CPI miss—7.7% YoY and 0.4% MoM (vs. 7.9% and 0.5% estimated). Markets matched ‘peak inflation’ and ‘Fed pivot’, fuelling the ‘Everything Trade’. All positions touted in previous notes responded as expected.

Source: Going John Galt

Now, where from here?

Dr. Strangelove or: How I Learned to Stop Worrying and Love the Fed Pivot

The TL;DR of this is that I’m not sure I’m there yet. Loving the Fed pivot, that is. Doubts are starting to creep into my forecast for ‘lower lows’. Hear me out.

There’s a good chance this is just a relief rally built on top of some strong—yet temporary—technical and fundamental factors:

-

There certainly was a cathartic feel to this rally. Markets found the relief they were looking for. Expectations of further rate hikes repriced down significantly in the aftermath of the CPI print, driving a sharp relief rally. But expectations have since trended up again toward the ~5% mark, peaking in June 2023.

-

It historically takes a few months (5-7) from the last hike to the full pivot (i.e., rate cuts), making me skeptical of this rally. It's simply too early. Normally, lows align with actual Fed pivots following proper economic pain. Today's Fed is still working on their controlled demolition of demand!

The problem however is that we have seen Mr. Market look past these kind of issues before, anticipating an often wildly distant recovery.1 Some elements supporting the reflation narrative include:

-

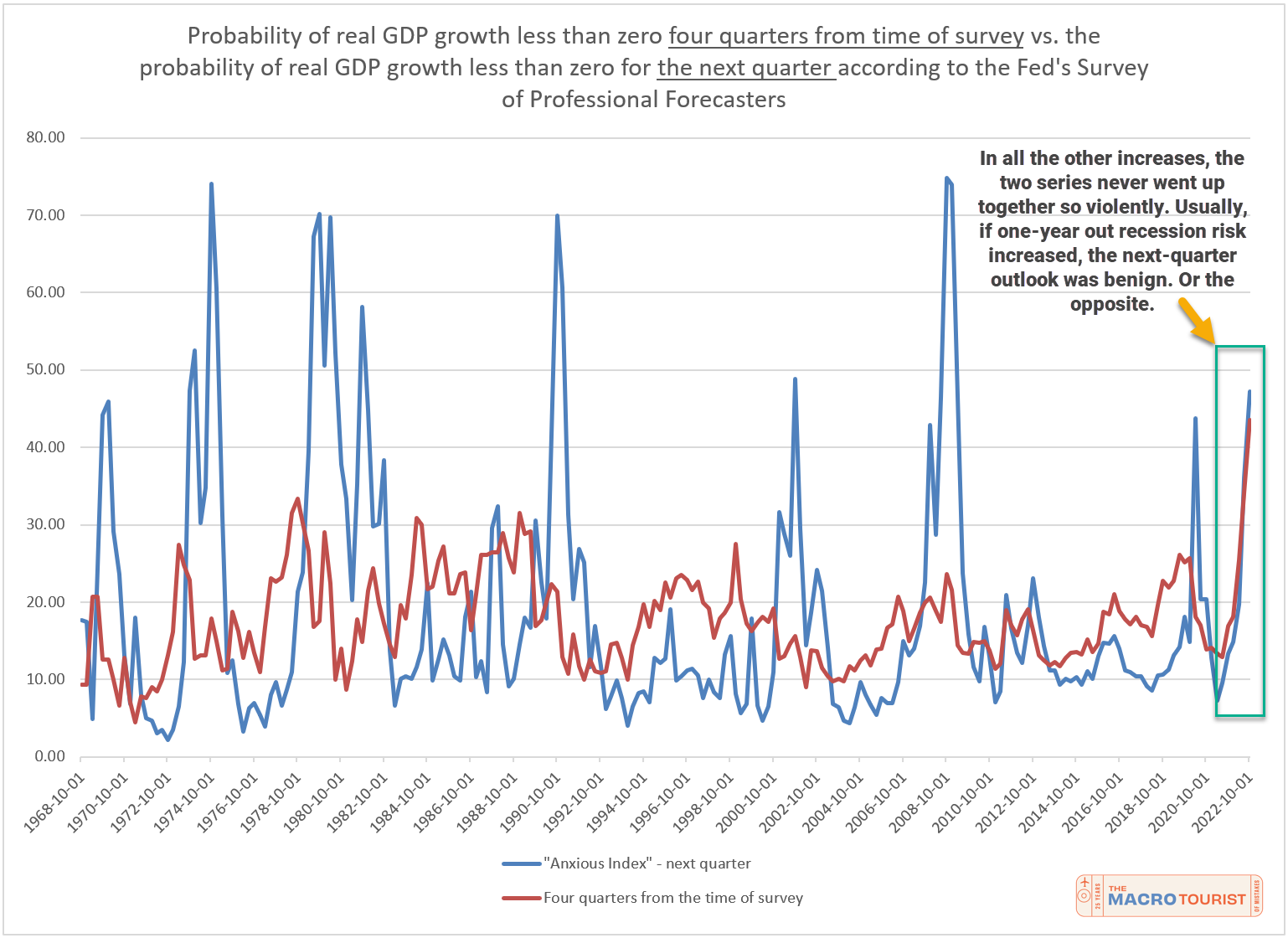

Markets have dropped quite a bit already, including one of the largest unwinds across fixed income in history. Everyone is already expecting earnings to drop on the back of next year’s recession, it may be priced in. Ask your banker / dentist / mechanic—they know this, too.

Source: The Macro Tourist

-

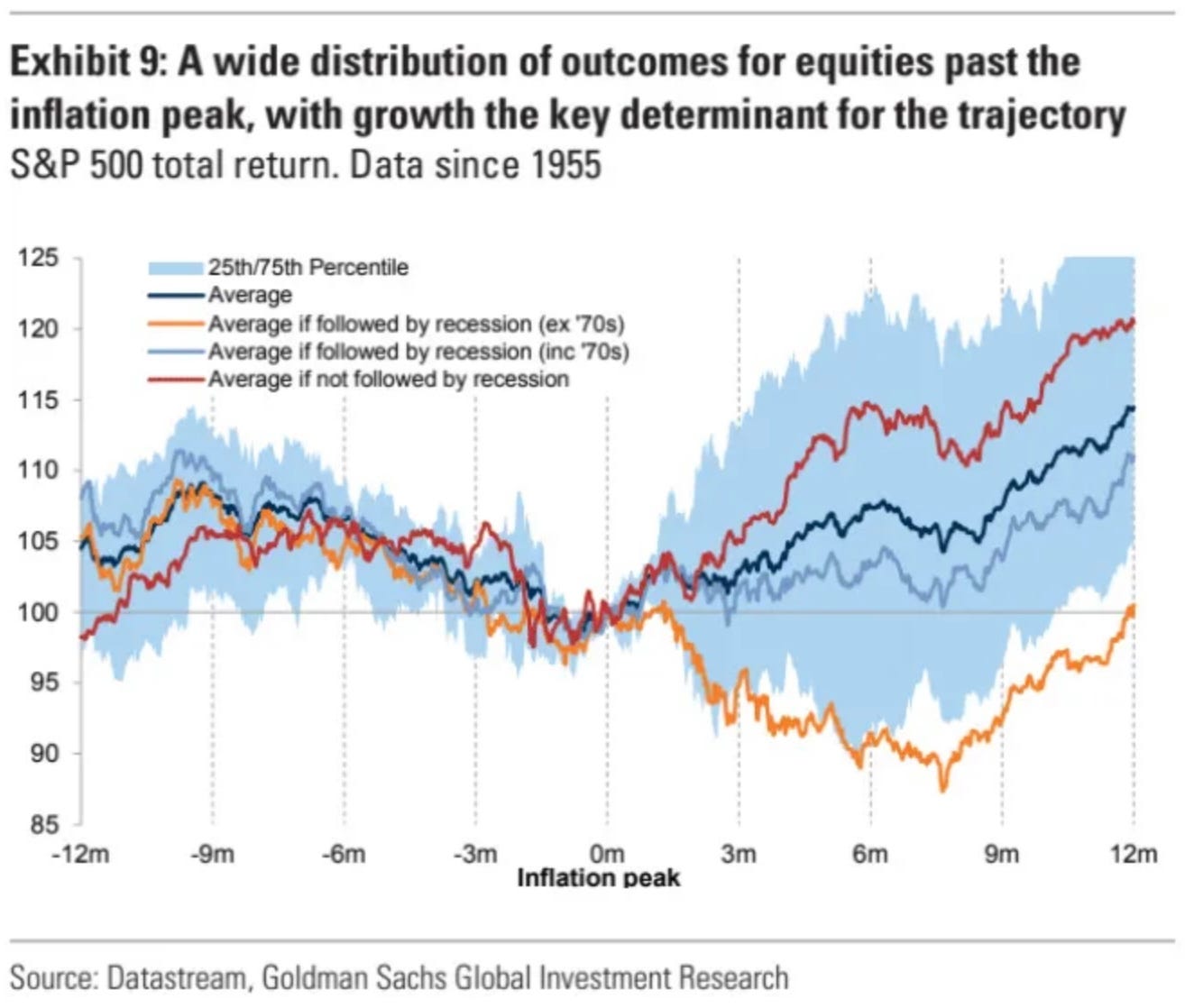

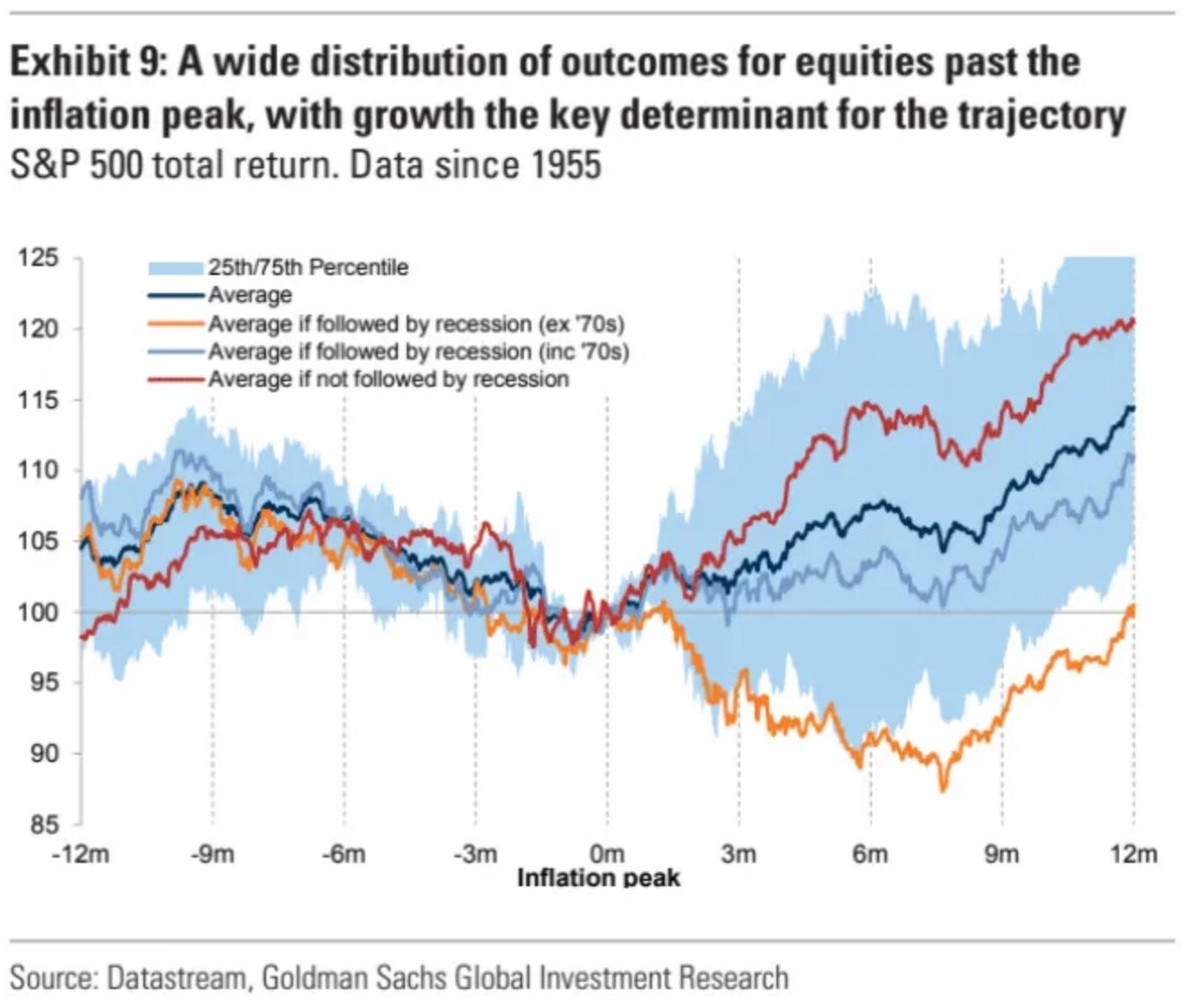

If inflation has peaked, every in-line, downward-trending, monthly datapoint for CPI / PCE will fuel the market recovery. By the time we find a floor for inflation (i.e., a hard-to-break level, perhaps in the 3-4% range), the market may have run substantially.

Source: Goldman Sachs

Furthermore, I didn’t expect Fed officials to take it seriously when I half-jokinglyhinted in a previous note they might be willing to “move the inflation target / goalposts from the arbitrary 2% in a dispassionate exercise of cold, economic realism”. From the Fed Whisperer himself…

-

China’s reopening is happening—I feel very strongly about this. Extrapolating the South Korean and Taiwanese re-opening experience, we might see some initial supply disruption from early wave of infections, but domestic demand will swiftly ramp up afterwards. China’s re-opening thesis turbocharged by fiscal / monetary stimulus underwritten by globally decelerating inflation could put a floor on global demand and somewhat offset the lack thereof elsewhere, as seen post-GFC.

As investors, when facts change we need to reassess.

After recent events I'm leaning toward a more balanced approach vis-a-vis my ‘lower lows’ forecast for equities. I'm no longer as convinced of seeing a big drop below the previous lows (~3,500 on the S&P500) and acknowledge increasing odds of a range-bound / slowly upward-sloping grind with substantial rotation within equities2.

From a long-term perspective, the current situation makes me a tad more comfortable with my current equity longs and happier to add opportunistically, if I find a right price for a great asset3:

-

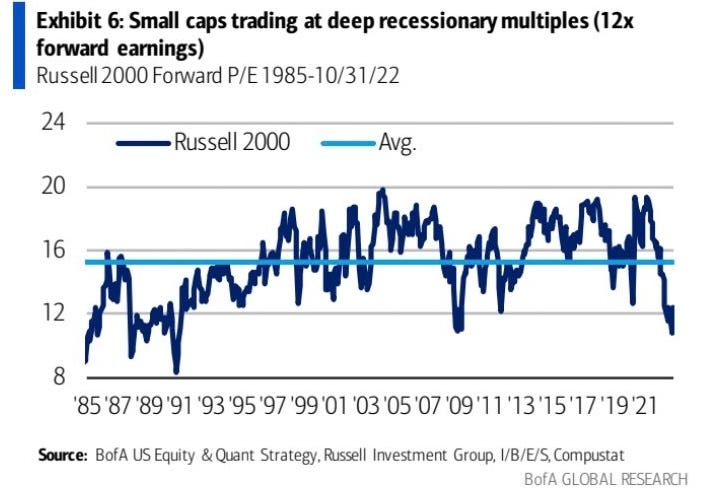

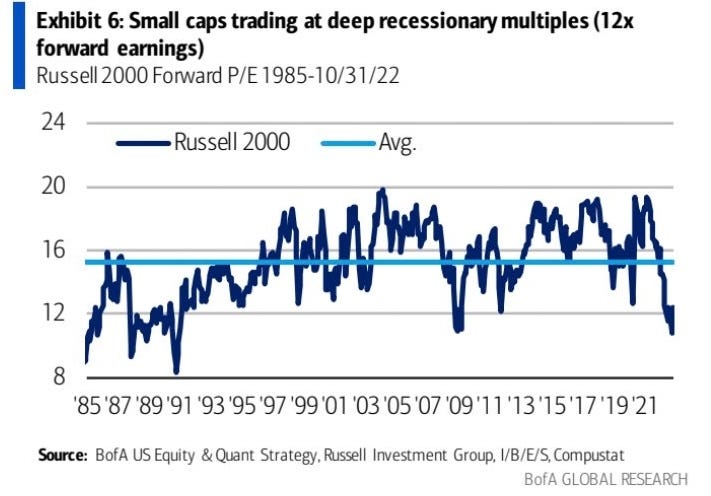

In general, I’m starting to like small caps here—they seem particularly inexpensive relative to historical valuations. They also outperformed their large-cap counterparts over the inflationary mid-70s and early-80s.

For reference, the Russell 2000 (i.e., the main US small-caps ETF) trades at >30Y lows in terms of forward P/E at ~12x, in line with GFC lows and below COVID and 2001 lows. I get that earnings can get scary fast, yet this seems overdone. The simplest way to play it is via the iShares Russell 2000 ETF (ticker: IWM), but there are some great industrials, mining and energy names trading fairly cheap, too.

Source: BofA

-

On the other hand, I increased my exposure to uranium (ticker: SRUUF, U-UN.TO), as explained in my last piece titled $22 “IT’S PRONOUNCED NUCULAR". I also remain bullish oil names as laid out in $13 THE BOOK OF MUIR.

-

I ringed the register on some ChinaTech on the way up—the main ETF is ~33% up since my original piece $19 CHINATECH: RETESTING CYCLE LOWS—and started reloading a couple of days ago, when news out of China (i.e., public revolt and subsequent shift in their COVID policy stance) proved they were running against their material constraints. Papic.

I wish I could offer a cleaner narrative—one which unequivocally hints in one direction, but unfortunately it would be intellectually dishonest to do so. That's not how markets work, it's often about probabilities and paths. I can only offer you my thought process.

In the face of uncertainty we all need to re-assess our views. Shifting toward a more balanced stance seems the right move for me, today. Let’s see what happens with Thursday’s PCE figure...

1 Many of us still seem to have PTSD from the incredible two-year, post-COVID rally. This likely includes Stan Druckenmiller, by the way.

2 We have already seen this equity rotation. Earnings were roughly flat this quarter, with energy and some defensives outperforming vs. InfoTech for instance. We may see more of these offsets, with less of an impact impact on index-level earnings.

3 In a range-bound market as I envision it (think: S&P trading from 3,500 to 4,100, I know it's a wide range but the bulk of trading would be in between) some assets can still lose 10-20% from here, but the downside is more capped.

With a longer term perspective, buying some assets within that range increasingly seems attractive. I'm afraid some great assets might have seen their lows, such as Vonovia (ticker: VNA) when we flagged at $19.2 (now ~$25).

More By This Author:

Comments

Log in or sign up to join the conversation.