22 Consecutive Years Of Dividend Growth And A Safe 3.8% Yield: TRI

Thomson Reuters (TRI) has raised its dividend for 22 straight years and is one of the most consistent free cash flow generators around. The company's business benefits from significant amounts of recurring revenue (87% of sales),

While TRI's rate of dividend growth is modest, we believe the company's 3.8% dividend yield and current valuation are attractive. For these reasons and more, we hold TRI in our Conservative Retirees dividend portfolio.

Business Overview

TRI was created when Thomson acquired Reuters (a 160-year-old global news and financial data service) for about $17 billion in early 2008. Many of the company's solutions were assembled through hundreds of acquisitions made over the years.

Today, TRI sells electronic content and services to professionals, primarily on a subscription basis. Its businesses provide solutions, software, and workflow tools which integrate its core data and information. Approximately 87% of TRI's revenue is recurring, and 92% of its revenue is from information delivered electronically, software, and services.

By geography, TRI generated 60% of its 2014 sales from the Americas, 30% from Europe, the Middle East and Africa (EMEA), and 10% from Asia Pacific.

Segments

Financial & Risk (52% of 2014 revenue; 39% of operating profit):provides critical news, information and analytics, enables transactions and brings together financial communities that connect trading, investing, financial, and corporate professionals. It also provides regulatory and operational risk management solutions. This segment achieved its first year of sales growth since 2008 in 2014. It has faced declining demand from bank clients, as firms have decreased expenses and cut jobs since the financial crisis.

Legal (27% of sales; 39% of operating profit): provides critical online and print information, decision tools, software and services that support legal, investigation, business, and government professionals around the world.

Tax & Accounting (11% of sales; 12% of operating profit): provides integrated tax compliance and accounting information, software and services to professionals in accounting firms, corporations, law firms and government.

Intellectual Property & Science (8% of sales; 10% of operating profit):TRI is in the process of divesting this business to sharpen its focus. This segment provided information and tools that enable the lifecycle of innovation for governments, academia, publishers, corporations and law firms to discover, protect and commercialize new ideas and brands.

Business Analysis

Thinking big picture, one of the first things we like about TRI's business is that professionals will always need more data and analysis. Knowing more about mission-critical topics (e.g. oil prices, geopolitical risks, currency movements, regulatory changes, etc.) helps people make better informed decisions, adapt to change, solve tough problems, and create successful outcomes.

TRI helps its customers accomplish these timeless objectives with its vast array of electronic content. As long as knowledge is valued by key decision-makers, there will be a need for TRI's type of solutions.

Over many decades of operation, TRI has established a strong position of trust with its customers. The Thomson Reuters brand ranked #57 on the list of Best Global Brands and has helped the company maintain #1 or #2 market share positions in most of the segments that it serves. For example, over 85% of Fortune 500 companies use TRI's legal research offerings.

TRI's deep industry knowledge, proprietary databases, trusted reputation, and embeddedness in customers' mission-critical workflows have all contributed to the company's strength.

New entrants struggle to match the breadth of TRI's enterprise solutions, which have been built up by hundreds of acquisitions over the last decade alone. Replicating TRI's unique databases, tools, features, and platforms would be an extremely costly and time-consuming endeavor. TRI has even stated that it probably has more company data than any other corporation in the world.

Customer contracts serve as another barrier, although the majority of them are up for renewal every year. Despite the short contract arrangements, TRI's existing customers would need to be willing to take a chance on a lesser-known vendor to part ways with TRI. Such a move could reasonably be deemed as "too risky" in many cases given the importance of customers' workflows and decision-making that has relied on TRI's solutions.

As a result of customers' dependence on its solutions, TRI has generally enjoyed 2% price increases each year. The company's continuously improving breadth, content, and capabilities help justify the price hikes and further strengthen long-term customer retention rates, which hover near 90% in its largest segment (Financial & Risk).

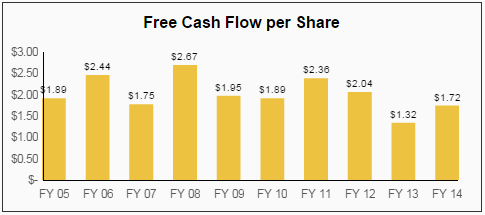

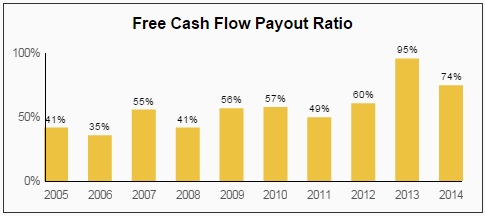

Thanks to TRI's recurring revenue, relatively fixed cost base, economies of scale, strong pricing power, great customer retention, and business diversification (no customer is greater than 1.5% of sales), the company has been a wonderful free cash flow generator over the years:

Source: Simply Safe Dividends

Despite TRI's strengths, the company's acquisition binge (TRI completed nearly 300 acquisitions between 2003 and 2013), growing collection of unrelated businesses, and weak customer growth trends following the financial crisis have resulted in several headaches.

The company's most notable acquisition by far was its $17 billion merger with Reuters in April 2008. The idea was to create a giant in the financial information market serving banks and investment managers around the world.

However, like many large deals, it came at a very inopportune time - right before the financial crisis. Macro challenges have caused TRI's financial segment to decline every year since 2008 up until last year, when it recorded its first growth. The Reuters acquisition resulted in cultural issues, failed product launches, management turnover, increased organizational complexity, and an incredibly disappointing stock.

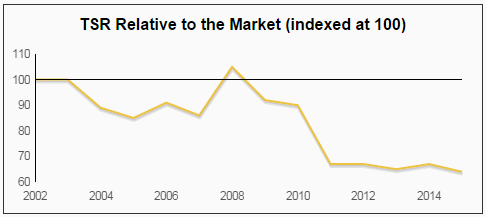

As seen below, TRI's total shareholder return (TSR) has substantially trailed the market since 2008 (a falling line means the market outperformed TRI's stock that year).

Source: Simply Safe Dividends

Much of the company's management team turned over during the past few years, including the CEO and CFO positions. TRI put together a turnaround plan in late 2013 to restore organic growth, simplify operations, capture true economies of scale, rely less on acquisitions, and improve profitability.

With a refreshing dose of humility, TRI acknowledged that its acquisition strategy has resulted in a complicated geopolitical infrastructure, an overgrown portfolio of products rather than an integrated enterprise, and a big company that lacks true scale.

As an example of TRI's transformation program at work, the company's financial segment had more than 850 products in 2013. That has been reduced to fewer than 200 today and will be reduced to three platforms once all of the work is done.

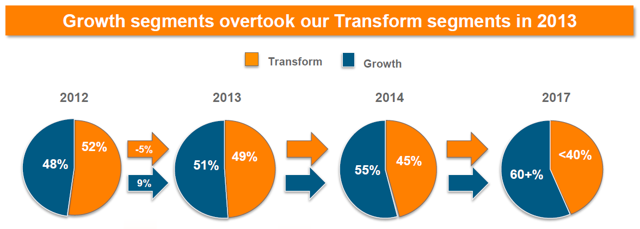

As TRI continues simplifying and unifying its products while divesting non-core businesses (e.g. TRI recently announced it is exploring strategic options for its intellectual property and science business, which accounted for 8% of sales in 2014), it hopes to show a meaningfully improved organic growth rate by 2017. As seen below, TRI is looking to generate 60% of its sales from "Growth" segments in 2017, up from just 48% in 2012. The company expects to return to organic revenue growth in fiscal year 2015 and should see its growth profile gradually improve as it allocates capital into faster-growing adjacent markets outside of its financial and legal research businesses.

Source: Thomson Reuters Investor Presentation

Product simplification is also improving TRI's cost structure and freeing up more cash to be returned to shareholders. TRI expects to achieve savings of $400 million by 2017 as its consolidated platforms capture economies of scale and fund ideas that can be better leveraged across the existing business.

By leaning more on organic growth rather than M&A, the company is also holding onto more cash to return to shareholders in the form of repurchases and dividends. For example, TRI completed just five acquisitions in 2014 for a total cost of about $167 million, which is significantly less than the 28 acquisitions it made in 2013 for $1.2 billion.

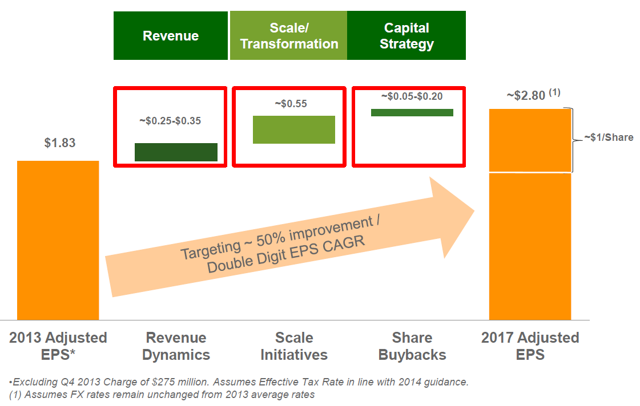

Putting it all together, management believes TRI can compound earnings at a double-digit rate from 2013 to 2017, resulting in total earnings growth in excess of 50%. The bulk of the increase is being driven by cost efficiency gains and incremental revenue growth (recall that TRI's cost base is largely fixed).

Source: Thomson Reuters Investor Presentation

Key Risks

As we hinted at above, TRI's M&A strategy has been a double-edged sword. On one hand, it has helped the company develop an extremely valuable asset base that is difficult to replicate.

On the other hand, it has clearly created an overly complex and fragmented product and cultural infrastructure. TRI is showing good progress on its 2017 plan, but it's still far from being a risk-free endeavor.

Beyond company-specific execution risk, TRI's markets are increasingly tech-driven. The reality is that data is becoming cheaper, information is more accessible than ever before, and low technology costs (e.g. the cloud) have resulted in thousands of fin-tech startups trying to disrupt the old incumbents like TRI, Bloomberg, and LexisNexis. These trends, which encourage more competition and innovation, will only intensify in the coming years.

Furthermore, some of TRI's larger markets (e.g. banks, big law firms) are struggling to grow headcounts due to heightened regulatory scrutiny and challenging economic conditions. Market saturation could lead to intensified competition and pricing pressures.

In other words, it's more important than ever before for TRI to stay reasonably ahead of customers' evolving needs to maintain its strong market share and profitability. We think the company still has a large advantage as the incumbent, but smaller players will always be much faster-moving.

If competitors begin eroding TRI's moat, it seems reasonable to expect a company as big as TRI to struggle with generating profitable organic sales growth. As of today, the business appears to be performing well.

TRI's Financial business has recorded six consecutive quarters of positive net sales (as of the third quarter of 2015). The Legal business also saw revenues grow by 1% and would have been up by 3% excluding print revenues. It's also worth mentioning that TRI's Financial & Risk segment posted its first year of sales growth since 2008 in 2014. Macro conditions have been strengthening, but TRI's initiatives have been driving some of the improvement.

For 2015, management expects positive organic revenue growth from all of its existing businesses and increased free cash flow generation compared to 2014. For now, it seems like TRI is keeping its competitors at a safe distance.

Dividend Analysis

We analyze 25+ years of dividend data and 10+ years of fundamental data to understand the safety and growth prospects of a dividend.

Dividend Safety Score

Our Safety Score answers the question, "Is the current dividend payment safe?" We look at factors such as current and historical EPS and FCF payout ratios, debt levels, free cash flow generation, industry cyclicality, ROIC trends, and more. Scores of 50 are average, 75 or higher is very good, and 25 or lower is considered weak.

TRI's dividend Safety Score of 54 suggests that its dividend's safety is about average. The company's payout ratios are a little higher than we prefer and it maintains a lot of debt on the balance sheet. However, its cash flows are very stable, and management is still squeezing out some earnings growth. It's also hard to ignore the company's commitment to the dividend with 22 consecutive years of growth.

Over the last four quarters, TRI's dividend has consumed 54% of its earnings and 70% of its free cash flow. As seen below, the company's free cash flow payout ratio has increased over the last decade from about 40% in 2005 to 60-70% more recently. Given the steadiness of TRI's cash flow, we aren't overly concerned by its payout ratio.

Source: Simply Safe Dividends

Looking at a company's performance during the financial crisis can also be helpful when evaluating the safety of its dividend payment. If earnings are highly cyclical, the company has greater risk of needing to freeze or cut its dividend if conditions unexpectedly turn south.

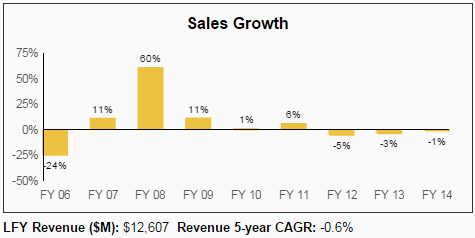

TRI's reported results are skewed higher because of its acquisition of Reuters, which closed in April 2008. Adjusting for the acquisition and currency headwinds, TRI's sales rose in 2008 and edged down by just 1% in 2009 despite meaningful weakness across many of its financial services customers. The company's stock also outperformed the S&P 500 by 12% in 2008.

Because a high proportion of TRI's revenues are recurring, its revenue patterns are generally more stable compared to other business models that primarily involve one-time product sales. TRI's sales are typically slower to decline when conditions worsen, but they are also slower to return to growth when the economy improves. We like these types of stable business models.

Source: Simply Safe Dividends

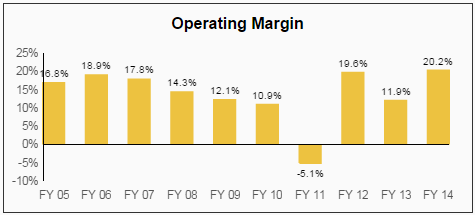

To go along with its stable sales growth patterns, TRI has maintained an attractive margin profile over the last decade. Steady sales and high margins are often the sign of an economic moat. As we previously mentioned, TRI has a relatively fixed cost base. With plenty of recurring revenue, an ability to push through modest price increases, and a gradually expanding platform of products, TRI is consistently very profitable.

Source: Simply Safe Dividends

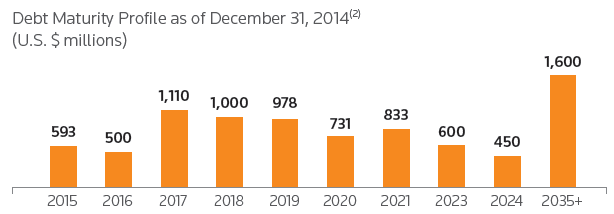

Turning to the balance sheet, TRI's stable business model allows it to maintain more debt than most companies. The company has over $10 of book debt for every dollar of cash, but its entire debt balance could be retired with cash on hand and three years of earnings before interest and taxes (EBIT).

TRI's average debt maturity is also 9 years, which provides plenty of flexibility for the company to meet its obligations.

Source: Thomson Reuters Investor Presentation

All things considered, we believe TRI's dividend payment is quite safe. However, we wouldn't mind seeing the company's debt balance reduced a bit - you just never know what could happen, and we sleep better at night with more financial flexibility.

Dividend Growth Score

Our Growth Score answers the question, "How fast is the dividend likely to grow?" It considers many of the same fundamental factors as the Safety Score but places more weight on growth-centric metrics like sales and earnings growth and payout ratios. Scores of 50 are average, 75 or higher is very good, and 25 or lower is considered weak.

TRI's dividend Growth Score is 32, suggesting that the company's dividend growth potential is below average. The company's score was reduced because of its above-average payout ratios, very low organic sales growth, and stretched balance sheet.

TRI targets a dividend payout ratio of 40% to 50% of its annual free cash flow and, assuming management hits its 2015 free cash flow guidance, the company is meaningfully above that range currently (closer to 60%). However, free cash flow available to shareholders should improve as TRI's spending on acquisitions remains much lower than it has been historically.

As seen below, the company's dividend has grown at a 2-3% annual rate over the last five years, and we wouldn't be surprised to see 1-3% annual growth continue until business growth accelerates.

While TRI's dividend growth rate is far from remarkable, it has been consistent. The company has paid out dividends consistently for over 30 years and increased its dividend for 22 consecutive years.

TRI is not eligible to join the S&P Dividend Aristocrats Index because it's not a member of the S&P 500, but it has been an extremely reliable dividend grower.

Valuation

TRI trades at 16x forward earnings and offers a dividend yield of 3.8%, which is about in line with its five year average dividend yield of 3.9% and represents solid income for investors living off dividends in retirement..

For a company with substantial recurring revenue, strong free cash flow generation, and reasonable business trends, the company's earnings multiple appears very reasonable.

If management can start generating 2-4% organic growth and high-single digit earnings growth in the next several years, the stock looks to have great value today and appears to offer 9-12% annual total return potential.

Conclusion

TRI shares many characteristics with our favorite blue chip dividend stocks. The company has a long history of strong profitability and dependable dividend increases, almost all of its revenue is recurring, and management is taking action to make the company more competitive for years to come.

While TRI's dividend growth rate is fairly low, its 3.8% dividend yield appears to be a very reliable source of income. Should management continue executing the turnaround plan and rejuvenate earnings growth, we think dividend growth could also improve over the next five years.

Disclosure: The author is long TRI.