Image Source: Unsplash

The outlook for the Internet-Software & Services industry appears mixed. Estimates are showing a clear upward trend through the past year, driven by a business resurgence at some companies. Others were positively impacted by the pandemic and the rush-to-digitize trend that it gave rise to, but then fell into a tough spot as the market corrected itself.

The macro concerns are leading to increased caution at customers, reflected in shorter subscription contracts and moderation in backlog growth. As may be expected, companies with mega cap and large customers are doing better than those dependent on smaller customers. The diversity of players in this group leads to some dissonance.

Being the backbone of the digital economy, it’s hard to see this industry doing badly over time. Some of the long-term trends are playing out this year even as concerns of a slowing economy looms large. Improving economic indicators and continued geopolitical tensions affect most players, but some are better equipped than others to deal with the situation.

While its innovation-driven growth warrants a premium to key indexes, its dependence on a strong economy has contained prices over the past year. So now may be as good a time as any to buy some shares. Our picks are NetEase (NTES) and Okta (OKTA).

About The Industry

The Internet Software & Services industry is a relatively small industry, primarily involved in enabling platforms, networks, solutions and services for online businesses and facilitating customer interaction and use of Internet based services.

Trends in the Industry

- The level of technology adoption by businesses impacts growth. While some companies have already built their platforms to facilitate the development and use of artificial intelligence, others are scrambling to catch up in order to stay competitive. This is further accelerating the adoption of technology that can help collect and analyze data, whether on the premises or in the cloud. Additionally, today we have many more cloud-first companies than ever before. Therefore, there is steadily increasing demand for software and services delivered through the Internet.

- The last few years have been tumultuous for the industry, but the most recent inflation numbers have raised hopes that the Fed’s inflation fighting measures will at worst lead to a very mild recession this year. Unfortunately, geopolitical tensions in Europe have a bearing on oil prices and supply chains, and therefore, contribute to a certain amount of volatility within the economy. Since the industry thrives on a strong economy that continues to do increasing levels of business, the outlook for 2024 is cloudy.

- The current instability of demand is increasing uncertainties for players. Since software and services are of varying kinds, some players did well during the pandemic while others did well during the reopening. Players increasingly prefer a subscription-based model, which brings relative stability, especially when companies have critical offerings. The ability to retain subscribers and raise prices as necessary is proving to be the key to success in the current environment.

- The higher volume of business being operated through the cloud and the increasing demand for enabling software and services involves infrastructure buildout, which increases costs for players. This causes great fluctuations in profitability as new infrastructure is depreciated and fresh debt is serviced (particularly in a rising rate environment). So even for those players that see revenue growth accelerate, profitability is often a challenge.

Zacks Industry Rank Indicates Improving Prospects

The Zacks Internet – Software & Services industry is housed within the broader Zacks Computer and Technology sector. It carries a Zacks Industry Rank #61, which places it in the top 24% of more than 250 Zacks classified industries.

The group’s Zacks Industry Rank, which is basically the average of the Zacks Rank of all the member stocks, indicates that the industry is coping better than many others. Our research shows that the top 50% of the Zacks-ranked industries outperforms the bottom 50% by a factor of more than 2 to 1.

The industry’s positioning in the top 50% of Zacks-ranked industries is because the earnings outlook for the constituent companies overall is improving. The aggregate estimate revisions indicate a more or less steady upward trajectory through the past year, with the group’s earnings estimate for 2023 now up 40.9% from a year ago while the 2024 estimate is up 54.9%.

Before we present a few stocks that you may want to consider for your portfolio, let’s take a look at the industry’s recent stock-market performance and valuation picture.

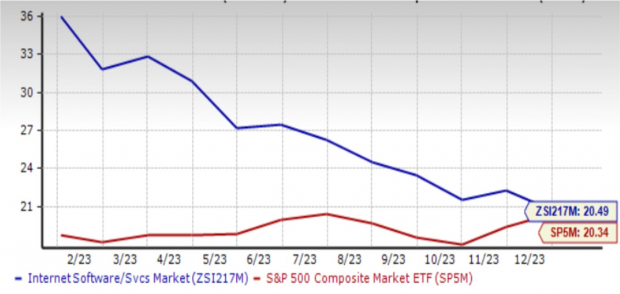

Industry's Stock Market Performance Remains Relatively Weak

The Zacks Internet – Software & Services Industry has lagged both the broader Zacks Computer and Technology Sector and the S&P 500 over the past year.

The aggregate share price of the industry increased 11.6% over the past year compared to the broader sector’s increase of 51.3% and the S&P 500’s increase of 24.4%. The industry was trading more or less in line with the S&P 500 until December, when analysts moderated estimates.

One-Year Price Performance

Image Source: Zacks Investment Research

Industry's Current Valuation is Fair

Given the weakness in prices despite the relative strength in the estimate revisions trend, the industry is now trading at a reasonable valuation. On the basis of forward 12-month price-to-earnings (P/E) ratio, we see that the industry is currently trading at a 20.5X multiple, which is a 23.3% discount to its median level of 26.7X over the past year. The S&P 500’s P/E is 20.34X (median value over the past year is 18.7X).

The industry is undervalued compared to the sector’s forward-12-month P/E of 25.8X. The current discount to the industry is 20.7%.

The industry has traded in the annual range of 20.5X to 36.1X, as the chart below shows.

Forward 12 Month Price-to-Earnings (P/E) Ratio

Image Source: Zacks Investment Research

2 Stocks Worth Considering

NetEase, Inc.: Hangzhou-based NetEase provides online services focusing on diverse content, including games, music, other services and education (dictionary, translation and including a range of smart devices) in China. Its products and services are focused on community, communication and commerce.

NetEase is currently building its international business through fresh gaming content that appeals to an international audience. For this purpose, it has also established its own studios in Japan, Europe and North America, and is building creative talent in these regions. It is also expanding reach beyond PCs and mobile devices to consoles that facilitate gameplay seamlessly across devices, which further helps to grow the user base.

In the last quarter, the company saw particular strength in gaming, on the back of new releases. With several other new games spanning different genres and geographies in the pipeline, management is optimistic about customer additions and growth prospects. The strength in Youdao was driven by its learning services (due to the consistent launch of high-quality courses and the human language coach ‘Hi Echo’), thus expanding the user base as well as its online marketing services. The cloud music business is undergoing a turnaround as management focuses on more profitable content and nurtures independent talent for the future.

Shares of this Zacks Rank #2 (Buy) company have gained 16.8% over the past year. The Zacks Consensus Estimate for 2023 has increased 30 cents (4.3%) in the last 60 days. The 2024 earnings estimate has increased 18 cents (2.3%).

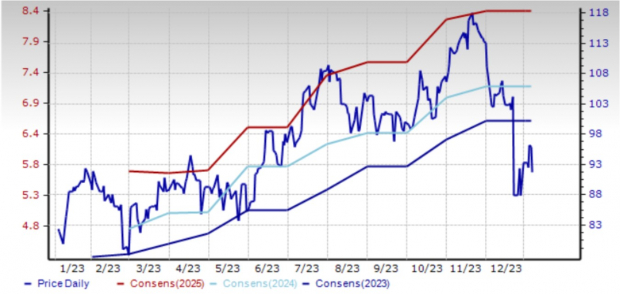

Price and Consensus: NTES

Image Source: Zacks Investment Research

Okta, Inc.: Okta provides a wide range of identity, access and authentication solutions for small and medium-sized businesses, universities, non-profits and government agencies within the U.S. and abroad. Its products are sold through a direct sales force and channel partners. It is headquartered in San Francisco, CA.

The company is on track to grow its business at a 37% CAGR between 2021 and 2024. Management estimates that the total addressable market for Okta is $80 billion and its innovative product portfolio of Privileged Access, Identity Governance and Access Management solutions (both workforce and customer) that are provided as a single platform positions it for rapid expansion.

While macro pressures are building up, secure access is vital to operations and the scope for growth substantial, which is likely what drove the increase in backlog and the improvement in revenue and profit outlook for the year. It is usually the larger customers that are able to continue capital investments in downturns and management commentary indicates that it is the customer cohort with $1 million plus annual contract value that grew the strongest. Okta generates 97% of revenue from subscriptions and has a customer retention rate in the mid-90s, which provides excellent visibility.

Shares of this Zacks Rank #2 company are up 24.9% over the past year. While estimates haven’t changed in the last 30 days, in the last 60 days, the 2024 (ending January) estimate increased 23.7% while the 2025 estimate increased 27.0%.

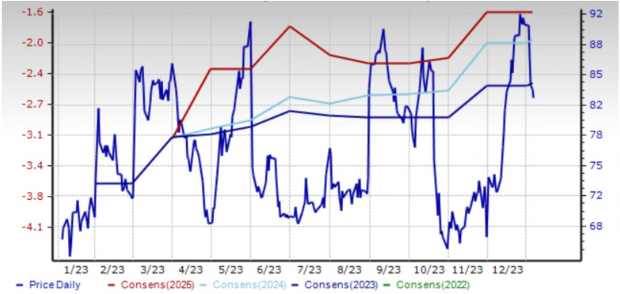

Price and Consensus: OKTA

Image Source: Zacks Investment Research

More By This Author:

Bull of the Day: NRG EnergyTime To Buy Lamb Weston's Stock After Solid Quarterly Results?

Insiders Are Buying These 3 Stocks

Comments

Log in or sign up to join the conversation.