Stagflation - Not Coming To An Economy Near You

Some analysts suggest that the pandemic and lockdowns will lead to a return to stagflation, last seen in the 1970s and very early 1980s. We don’t agree, which in some ways is a pity, as it might not be all that bad an outcome if it did happen.

Source: Shutterstock

Relative price increase possible, probable even...

High inflation is generally not regarded as a good thing, as it reduces the value of savings. Combine that with high unemployment and a stagnant economy, and you have all the ingredients for a nasty cocktail and also the making of a high “misery index”.

With many economies coming out of Covid-19 lockdown and demand likely to increase, but supply disruptions likely to linger, some pundits have been pointing to the likelihood of stagflation and wagging a warning finger.

It is, in our view, entirely possible, even probable that such conditions lead to short-term relative price increases in some areas, for example, supermarket staples, and healthcare items such as masks and sanitizers. But even with broader price increases, one of the unique features about earlier episodes of stagflation, was how supply shocks (oil in the 1970s and 1980s) became embedded. And for this to occur requires mechanisms that will be extremely hard to replicate today.

Things are very different to the 1970s

Accommodative central banks were partly blamed for earlier bouts of stagflation, and today, it is hard to argue that with QE becoming widespread, and more central banks knocking on negative rates, that monetary policy is not at least as accommodative as it was in the 1970s.

But for this to develop into stagflation requires a wage-price spiral that is hard to imagine occurring today, at least not in any developed market economy.

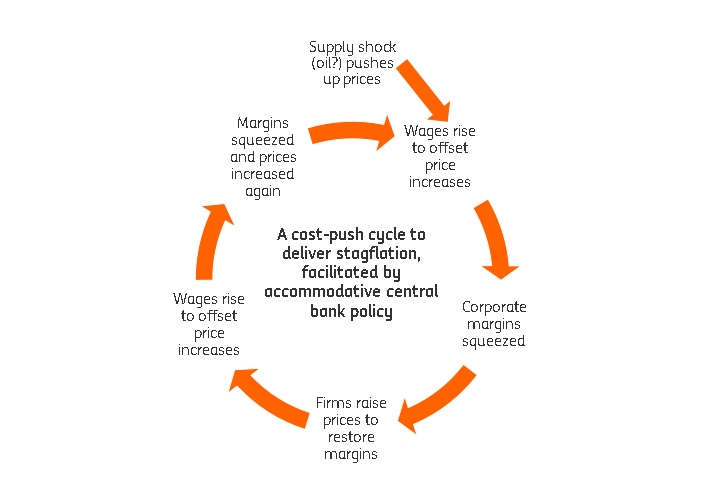

In the 1970s, with large manufacturing sectors and high domestic content to production, mass unionization, collective bargaining, and employees with high degrees of firm-specific skills a price shock could lead to wages being bid higher, squeezing corporate margins, and requiring an offsetting price increase from the firm to keep margins positive. That, in turn, would spark another round of wage increases, and then margins squeeze and price increases and so on (see stylistic diagram).

Another way of putting this is, easy money isn’t particularly inflationary without a high velocity of money – and this has collapsed across the developed world. It isn’t enough to just cut rates or print money – the real economy actually has to respond, not just financial assets, and that doesn’t happen much anymore.

Even with a little less help from globalization in the coming years than we may have become used to, the situation today and likely in future years too is far less prone to inflation than it once was. Labour has next to no say any more on its remuneration, irrespective of how low the unemployment rate falls. And manufacturing is a fraction of the importance for economies it once was, is largely automated, and uses workforces that have been de-skilled and become easily replaceable.

Stylistic diagram of how stagflation takes root

Source: ING - Stagflatoin cycle

A bit of inflation, even stagflation might not be all that bad...

Central banks, even using today’s policies, which would have been considered absurd in the 1970s, can’t often even get inflation high enough to hit the middle of their inflation targets when times are good. What hopes then of stagflation in a post-Covid19 world? The answer seems to us is, practically none.

And in some ways, this is a pity, because aside from the withering effect of inflation on household savings, inflation has exactly the same effect on debt. This enables governments to deflate away debt piles accumulated in bad times and enables households to borrow and spend, safe in the knowledge that rising wages will make debt service more manageable as time progresses, even if today it is a struggle.

Consequently, some have even suggested running inflation “high” deliberately after the pandemic has eased, just to reduce the debt pile, which otherwise, may weigh heavily on future growth prospects. Right now, however, such suggestions fall foul of the practical difficulties of making that happen, and in the end, some other approach is likely to be needed to reduce the inevitable debt burden stemming from the Copvid-19 pandemic. The “stag” bit of stagflation looks eminently achievable. The “flation” bit is another matter.

(This note is summarised from an earlier piece, and you may also like to see the linked video)

The problem that should be very obvious in that deadly circle is the reality that not all wages will rise. In fact, MOST wages will not rise. Profits will rise to placate the shareholders and assure bonuses for top management, but for all of those "others", the ones not getting the wage increase, it will be a case of inflation with no benefit at all. Unfortunately it is exactly the sort of thing that central banks would be happy to have happening.

The really bad news is that it is the sort of circle that initiates revolutions. Mostly, in our calmer society they are ballot box revolutions, in other times they have been fairly violent ones. Perhaps, somehow, greed by the central banking system can be reduced a bit. Avoid the revolution!

Thank you for this article. I saw that you wrote that you believe we will see an inflation in prices for regular healthcare home items- such as mask and sanitizers. Being that so many "Non-Mask" companies stepped up and made masks, why do you think this would be so, as this market potential has been realized and the supply should be quite high?