Why The Market Is Worrying Too Much About A Rate Hike

I really don’t get it. Stock market players are entirely too focused on when the Fed will raise interest rates and what effect the rate increase will have on stock values. Just the expectation of a tiny, little increase in the Fed Funds rate can send the market down by a significant amount. Except, history shows that this is probably not what will happen.

The U.S. economy and markets have existed in a very unnatural world since December 2008. That was when the Federal Reserve Board reduced the Fed Funds Target Rate to a range of 0% to 0.25%, which was essentially zero percent. In the markets, the majority of short-term interest rates derive from where the Fed sets its target rate. The zero interest rate policy (ZIRP) of the Fed has ruled the financial markets for over 6 1/2 years. The investing experts and public have gotten used to a base short term interest rate that sits at 0% and does not change. This comfort zone has led to the fear that when the Federal Reserve Board finally gets around to raising interest rates, the higher rates can only be bad news for the stock market and stock prices will drop significantly. A little history lesson will show how these fears are very misguided.

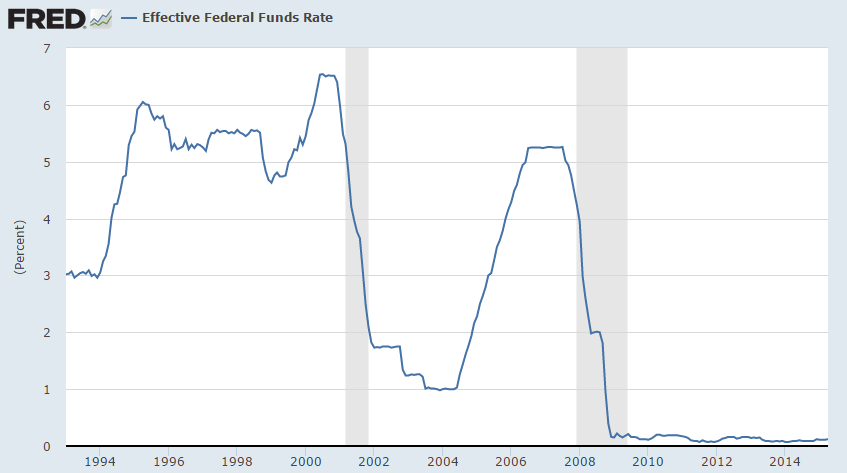

Historically, the Fed was very willing to change the Fed Funds rate in reaction to economic growth and inflation projections. Here is a chart of the rate for about the last 20 years.

Note a couple of things on this chart. First, over that period of time, the Fed Funds rate changed a lot. And guess what, the financial world did not come to an end. Next, notice that the average rate prior to the end of 2008 was about 3%. Again, the economy and markets worked fine, even though interest rates were not at or near zero percent. The final point that you need to know is that in the decades prior to 2009, the Fed changed interest rates regularly throughout the year, between two and 10 times per year, with an average of about four rate adjustments per year. Each change was usually an adjustment of 0.25% or 0.5%. The Fed gave up all of its interest rate ammo with the December 2008 move to lower the Fed Fund rate by a full 1.0% down to the near zero area that we now live under.

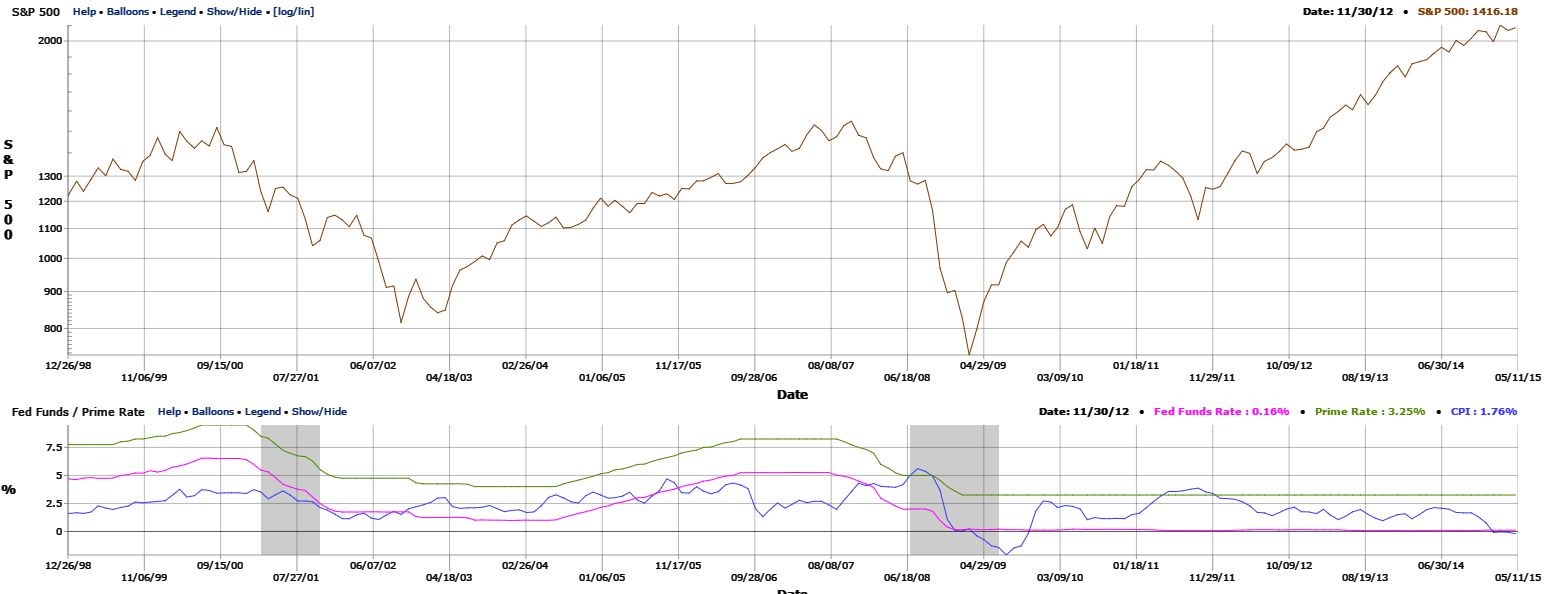

Next up in the following graph is the S&P 500 in the upper box and some interest rates in the lower section. The Fed Funds Target Rate is the pinkish line. This graph shows that in the previous two stock bull markets, interest rates generally moved upward right along with the stock market. When the economy slowed and the market started to go down is when the Fed would start to lower its target interest rate. The point to understand here is that if the Fed raises rates it is not an automatic downer for the stock market.

I cover and recommend higher yielding, dividend paying stocks, which many assume would be most affected by a rate increase. I find it difficult to imagine that a one-half percent increase in the Fed funds rate all the way up to 0.50% would have a large effect on quality stocks yielding 5% to 8%. A significant number of the stocks. One group that comes to mind are the commercial mortgage REITs.

There will be some stocks hurt by even a small interest rate increase. The group in the most danger are the residential mortgage backed securities (MBS) owning REITs. These REITs use massive amounts of leverage, 6 to 8 times their equity, to turn 2.5% MBS yields into 10% plus dividend yields. This business model uses variable rate borrowing to finance portfolios of fixed rate mortgages. Rising interest rates will not be good to this group of REITs. Unfortunately, residential mortgage REITs are popular with a lot of individual investors who don’t understand the interest rate game and the huge risk they’re taking on with these investments.

The points of today’s lesson are: rising rates historically go along with a rising stock market, and a small interest rate increase from the Fed will not crash the market. In the high-yield finance REITs space, there is a big difference between the commercial mortgage lenders and the residential mortgage investing REITs. Own the former and dump the latter.

High-yield REITs with a solid track record of increasing dividends are one of the core investments we use in my Monthly Dividend Paycheck ...

more