Image Source: Nick Youngson CC BY-SA 3.0 Alpha Stock Images

We’ve got more merger and acquisition (M&A) activity to talk about today. Last week, when I wrote that “M&A Is Back in Play,” I was fairly focused on Blackstone (BX), the world’s largest alternative asset manager. It has a history of buying up real estate investment trusts (“REITs”), my area of expertise.

So naturally, I was interested in analyzing what it might set its well-funded sights on in the near future. I never recommend a company on takeover possibilities alone, but there is major profit potential in evaluating quality candidates, nonetheless.

Today, though, I want to look at AT&T (T). The cell carrier giant announced last week that it will buy the majority of EchoStar’s (SATS) low-band and mid-band spectrum. Fifty megahertz, to be specific, for $23 billion.

Spectrum is the range of frequencies used to carry wireless signals, the type that AT&T’s customers use daily. In essence, AT&T bought more “real estate” to help with throughput for its users.

EchoStar, which owns Dish Network, has had problems since 2020, when it first entered the cell-carrier space. That was after regulators put strict stipulations on T-Mobile’s (TMUS) merger with Sprint.

In order for that deal to happen, EchoStar would have to enter the game to keep the playing field suitably diverse. So the company did exactly that. But then interest rates climbed, subscriptions declined -- and by June 2025, it admitted it didn’t think it could pay its July loan obligation of $114 million. Obviously, $23 billion will cover that, complete with late fees and any other penalties it may have incurred.

“This transaction puts our business on a solid financial path,” EchoStar CEO Hamid Akhavan explained, “further facilitating EchoStar’s long-term success and enhancing our ability to innovate and compete as a hybrid network operator.”

While not an acquisition of the company itself, such a large purchase is more evidence that deal-making is back on the table.

Investors have since jumped all over EchoStar, sending the stock higher. But if you’re looking for exposure in the telecom space, I might suggest a few other routes.

Put These Wireless Network Landlords on Your Radar

I’ve long been bullish on the telecom/wireless network space, although my interests have largely been on the REIT side.

REITs cover a wide variety of sectors, including cell-tower properties. These companies establish and maintain the infrastructure that AT&T, Verizon (VZ), T-Mobile, EchoStar’s Boost Mobile, and their smaller competitors hang their transmission hardware on.

This model can pay off quite well. After all, between our phone calls, browsing, and shopping, we’re increasingly reliant on cell service. As Statista writes, it’s “hard to picture a day without a smartphone – no quick calls to friends, no music on the go, no late-night social media scrolls.”

In short, we’re addicted. That obsession has created quite a business for cell-tower REITs like American Tower (AMT), Crown Castle (CCI), and SBA Communications (SBAC). Out of these, I prefer American Tower.

It has a global reach and exposure to the booming data-center sector. Plus, as shown below, its shares have been trading with a wide margin of safety: 19.3 times adjusted funds from operations (“AFFO”) versus its normal valuation of 22.2 times. Analysts are forecasting 7% growth in 2026.

Source: FAST Graphs

That’s one investable link in the chain. Another, of course, is smartphone manufacturers like Apple (AAPL) and Samsung – with iPhone sales alone topping $200 billion last year. And then there are the service providers I already listed – the ones that rent way-up-high space from the cell-tower REITs I cover. They make a pretty penny, too.

Take T-Mobile, the smallest of the big-three providers by far, with “just” $81.4 billion in profits last year. It still netted income of $11.3 billion in 2024, with diluted earnings per share of $9.66.

But of the major carriers, T-Mobile isn’t my favorite.

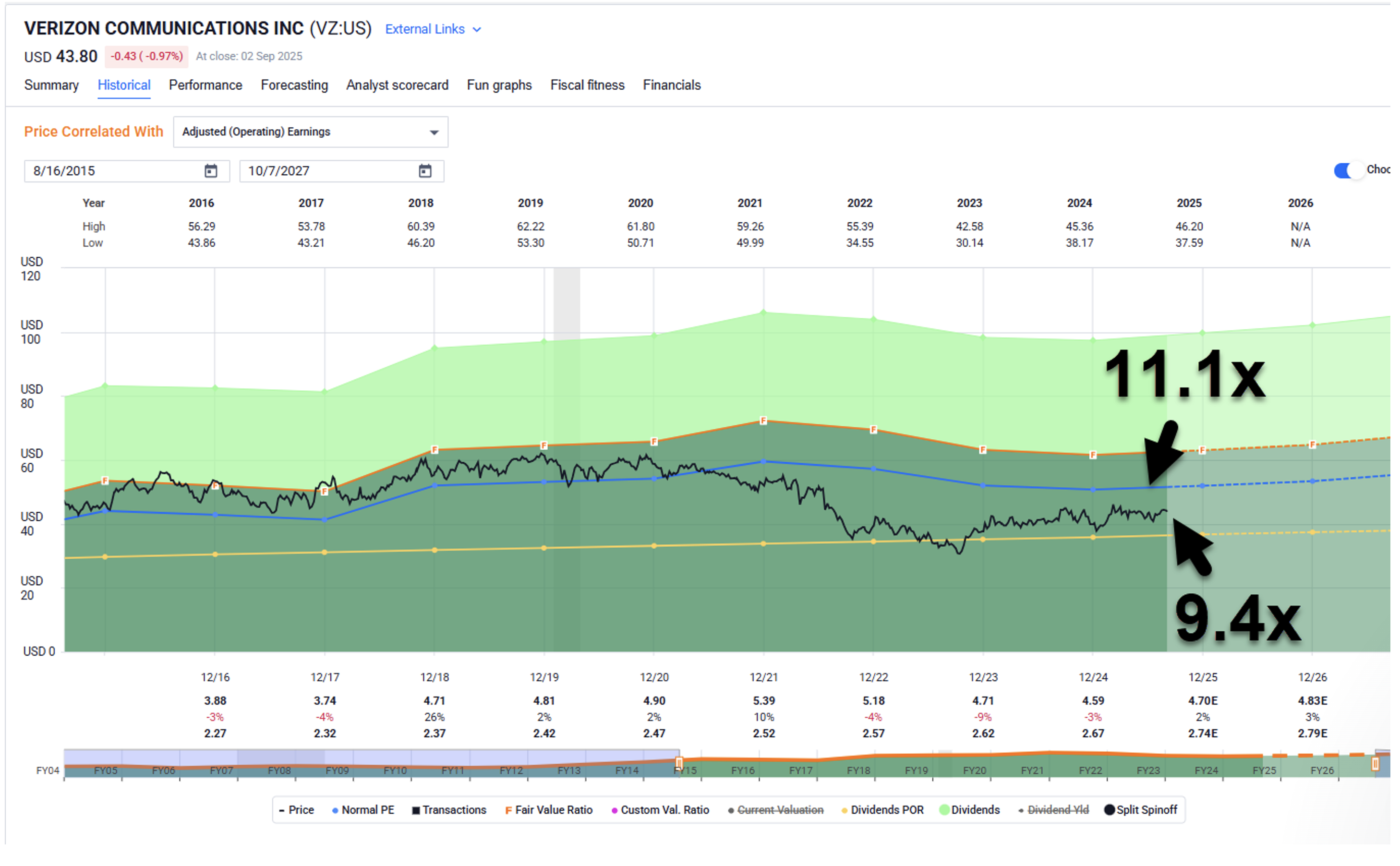

Verizon Is the Value Play

Verizon has lagged AT&T year-to-date, making it a value play consideration. At 9.4 times forward earnings, Verizon has been trading at a massive 30% discount to AT&T. So, it should be no surprise that it’s also the highest yielder in the sector, with a 6.1% yield. That’s the 11th highest in the S&P 500.

That’s something to keep an eye on. And with a payout ratio of around 63% and the predictable nature of its earnings (people have to pay their phone bill every month), that dividend should be fairly safe.

And it’s also important to realize how important its dividend is to Verizon. The company has raised its dividend for 18 years straight, putting it on track to become a dividend aristocrat in seven more years. We’re expecting another dividend boost in September.

Plus, Verizon won regulatory approval in May for the $20 billion purchase of Frontier Communications. That acquisition will add new fiber-based broadband customers to its Fios base, further boosting its appeal.

As mentioned, shares have recently been trading at 9.4 times compared with its normal valuation of 11.1 times. And although analysts expect just 3% growth in 2026, we consider Verizon an attractive value that could generate returns of around 15% over the next 12 months when accounting for earnings growth, the dividend, and modest multiple expansion.

Source: FAST Graphs

A Riskier Telecom Poised to Profit

If you’re interested in a greater-risk, greater-reward opportunity, I do have one final suggestion to consider.

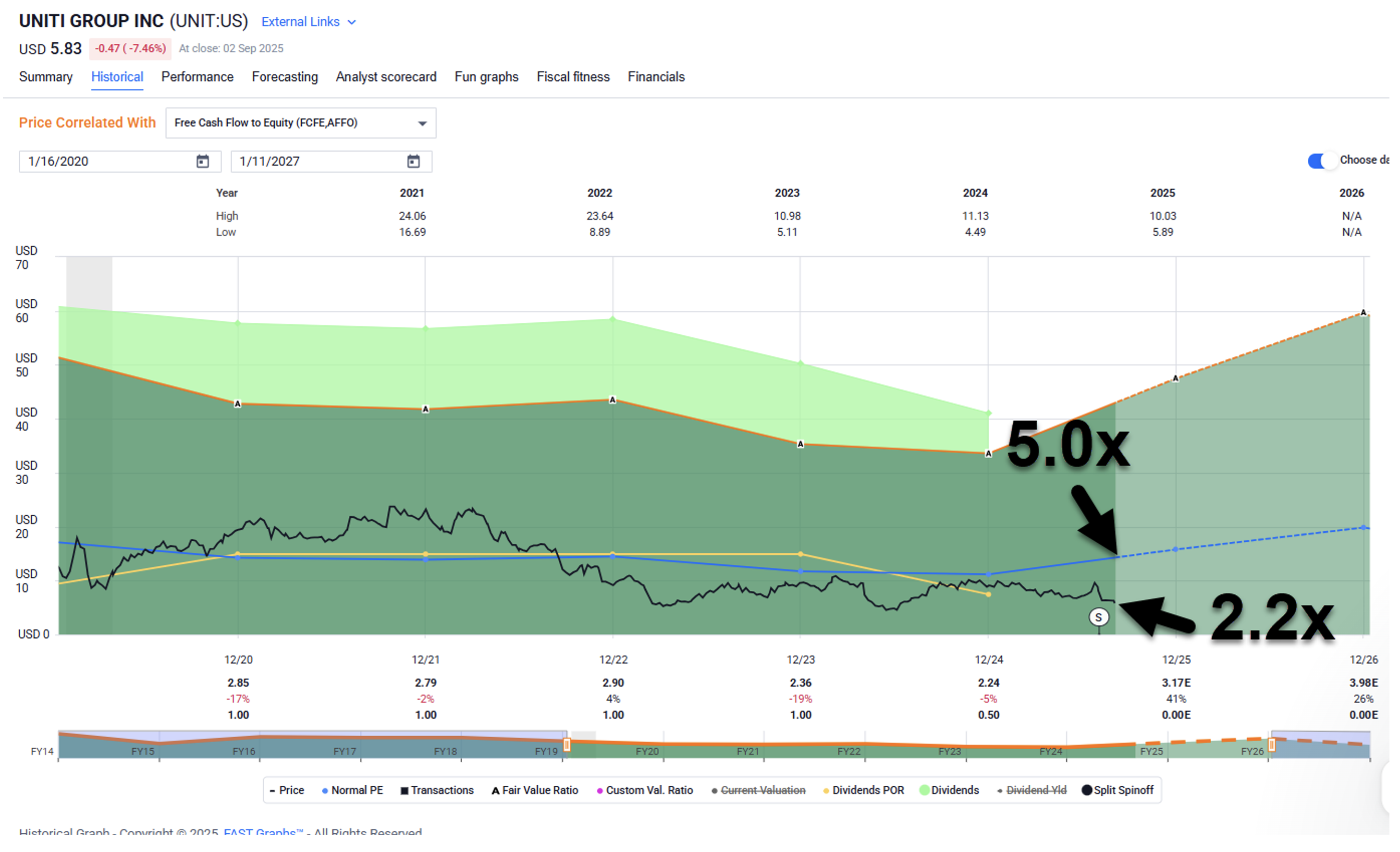

Uniti (UNIT) is a small-cap REIT I’ve been following for years. It completed its merger with Windstream just last month, laying the foundation for a copper-to-fiber transition. This combination makes Uniti look a lot more like Frontier Communications, which Verizon acquired earlier this year. And this could lead to it being snapped up itself.

With all that in mind, I’m excited to add the company back to our small-cap coverage.

Uniti’s recent valuation is 2.2 times price to adjusted funds from operations (the REIT equivalent of price to earnings). And analyst consensus puts its 2026 growth at 26%. As such, we believe shares could fetch $10, which translates into annualized returns of 50% or higher.

Source: FAST Graphs

It’s your call, of course. But if you’re looking for exposure in the telecom space, I’d start here.

More By This Author:

Inside The Portfolio: Top Dividend & Tech Stocks For The Perfect MixIf I Were Blackstone, I Would Buy These Three REITs

4 Real Estate And Energy Stocks Powering The Next Big Wave Of The AI Boom

Comments

Log in or sign up to join the conversation.