-

Investor sentiment is the worst since the pandemic lows among real estate investors

-

Global REITs have suffered – first from rising rates, now from geopolitical fears

-

Investor allocations are somewhat light vs history, suggesting opportunities could arise in the coming weeks and months

The S&P Real Estate sector is the second-worst performer so far this year. Only Consumer Discretionary has a lower YTD total return. The 13% drop comes as homeowners around the world bask in the bliss of surging home price indexes.

Just last week, the US S&P CoreLogic Case-Shiller Home Price Index notched another all-time high in its December reading. Interest rates did not begin to tick up with earnest until mid-December, so it will be interesting to see the next handful of monthly figures on house prices.

Sour Sentiment

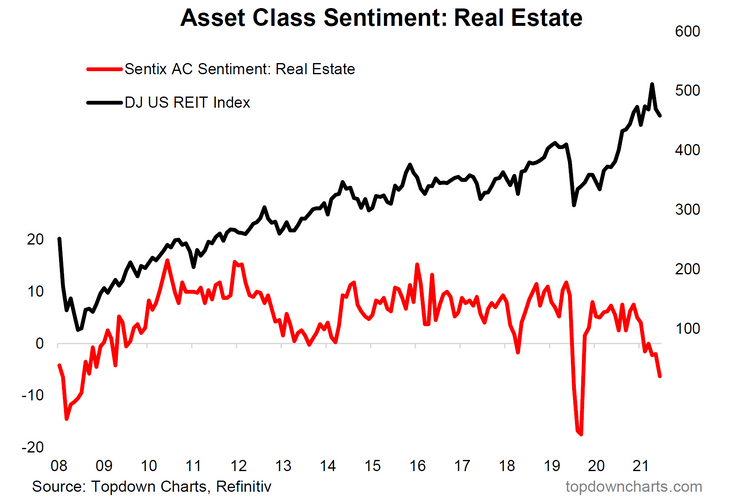

Meanwhile, real estate equity investors are in the dumps. The most recent Sentix sentiment survey on real estate assets dropped again in February. Our featured chart below illustrates that the mood has not been this bad since the depths of the pandemic. Before 2020, you have to go way back to the global financial crisis to find a worse reading.

Featured Chart: Real Estate Asset Sentiment Sharply Lower

REITs Reverse After a Strong 2021

This week’s Global Cross Asset Market Monitor assesses the state of the real estate market around the world. We also look at REITs – a key high yield asset space for many investors. REITs had a stellar 2021. The S&P sector ETF, XLRE, returned more than 46%. It was second only to Energy in terms of sector performers last year. Even amid a dreadful start to 2022, the Real Estate sector is second-best year-on-year at +24%.

Bad Global Breadth

Outside of the US, global REITs have suffered too. Geopolitics, inflation fears, Fed tightening prospects, and a bond market selloff (up until recently) all dinged real estate equities. We find that breadth has tanked. Fewer than 25% of global REITs now trade above their 200dma. That, too, is the lowest since the pandemic.

Rising Rates Were a Headwind, Geopolitical Risks Now Front & Center

Typically, you would expect real estate to hold up well during inflationary times. The problem is higher inflation often means rising interest rates. Higher yields can hurt real estate. So, there is a degree of nuance to that thesis. The jump in yields has been dramatic over the short- and intermediate-terms across developed global markets. The average DM 10-year yield surged to just shy of 1.5% but has since pulled back hard amid intense bond buying this week.

Laying A Bullish Foundation?

The upshot? Our weekly report sent to clients each Monday morning includes some optimism. US ETF market share remains light compared to history. We are monitoring the space for opportunities despite lingering headwinds. Also in the property space is the worsening downturn in the Chinese property market - a potential harbinger of things to come for US markets as the central bank of China tightened monetary conditions last year.

Bottom Line: Real estate has been hit hard in 2022. Only discretionary stocks have fared worse amid rising interest rates through early March. Unfortunately, the latest flight to safety in bonds did not benefit the sector or global REITs either. We want to be patient for opportunities as sentiment seems to only be getting worse.

Comments

Log in or sign up to join the conversation.