NRZ's 12.5% Yield: A Deeper Dive

As a follow-up to our article on New Residential at the beginning of this week, this article takes a deep dive into a variety of big risks as well as reasons to be optimistic (and we're not only talking about the big dividend yield).

New Residential (NRZ) is a real estate investment trust (REIT), and its big 12.5% dividend yield is viewed as a red flag by some investors, and as an attractive opportunity by others. After reviewing the evolving real estate investment industry and NRZ’s opportunistic business model, this article describes a variety of big risks facing the company, and then shares multiple reasons to be optimistic. And we conclude by sharing our views on why New Residential is absolutely worth considering for an allocation within your income-focused investment portfolio.

The Industry and New Residential Are Evolving

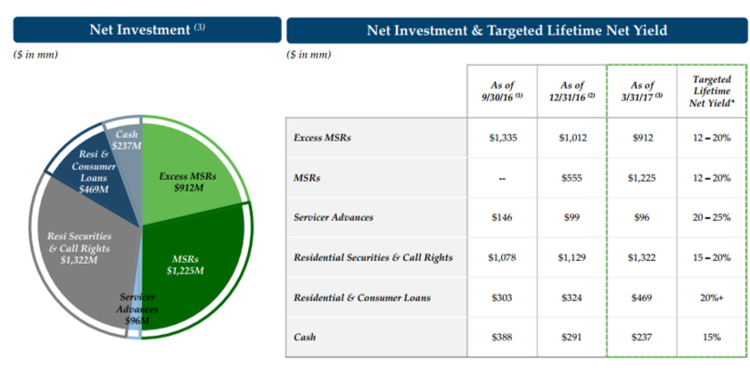

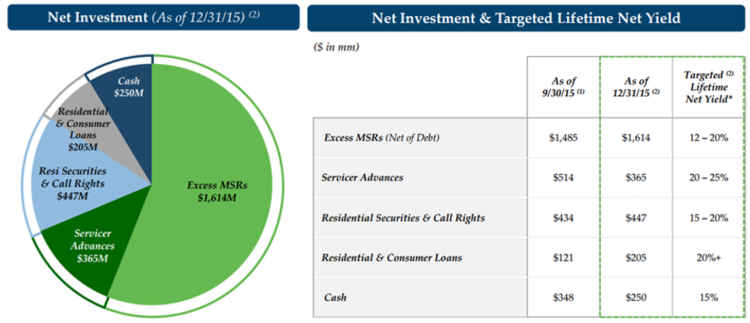

For starters, here is a look at the breakdown of NRZ’s investment portfolio now (3/31/17), followed by NRZ’s investment portfolio just 15 months earlier (12/31/15).

A few things stand out. First, the amount of Excess Mortgage Servicing Rights (Excess MSRs) has dramatically declined. Excess MSRs are basically the right to service a pool of mortgages that the primary mortgage servicer cannot handle (they’re overflow), and as you can see in the table they have very high expected returns (+12-20%) for NRZ. And especially important, MSRs and Excess MSRs tend to rise in value as interest rates rise (our current market environment) because mortgage prepayment speeds slow (people don’t want to refinance at higher rates) and this a good thing for NRZ.

However, even though Excess MSRs are lucrative for NRZ, the company is doing less of them because the industry is evolving. The Excess MSR concept took off during and following the housing crisis because the industry became increasingly complex, and NRZ was there to profit handsomely from the opportunity. However, as the housing crisis moves further into the rear view mirror, the opportunity for Excess MSR investments has slowed (less mortgages require distressed servicing), and as a result NRZ has opportunistically entered the MSR business.

In August 2016, NRZ made its inaugural full MSR purchase, and continued its momentum of investing in MSRs from multiple sellers throughout the remainder of that year, as shown in the following table.

This is an example of NRZ opportunistically taking advantage of the changing residential mortgage environment to deliver more high returns to its investors (+12-20% net yields).

Other noticeable changes are NRZ’s dramatically reduced investments in servicer advances (per our earlier pie chart). This is important because there is increasing counterparty risk with some of NRZ’s counterparties, and NRZ has proactively reduced exposure.

Further still, NRZ dramatically increased its exposure to residential securities and call rights. This reason is because the company needed to do something with all the cash it generates, and they have expertise in this area. As we’ll cover more later, there are also significant risks to these types of investments.

Again, as we mentioned earlier, the industry is changing as there is less distress as the housing crisis moves further into the rear view mirror. This means less lawsuits and more visibility into the future for NRZs service providers, and new opportunities with MSRs (instead of only Excess MSRs) and residential securities trading. And in many regards, all of this is good for NRZ as we will discuss more later.

Before getting into all of the good things about NRZ, it’s prudent to consider the risks. We have highlighted eight big risks that we believe NRZ investors should be aware of and monitoring. Here is the list:

NRZ’s Big Risks

1. NRZ is in big trouble if its mortgage servicers go bankrupt

According to NRZ’s annual report: “We rely heavily on mortgage servicers to achieve our investment objective and… It is expected that any termination of a servicer by mortgage owners (or bondholders) would take effect across all mortgages of such mortgage owners (or bondholders)… Therefore, it is expected that all investments with a given servicer would lose all their value in the event mortgage owners (or bondholders) terminate such servicer. Nationstar, Ocwen and Ditech Financial LLC (“Ditech”) are the servicers of most of the loans underlying our investments in MSRs and Servicer Advances, and Nationstar and Ocwen are the servicer or master servicer of the vast majority of the loans underlying our Non-Agency RMBS to date.”

And what makes this risk particularly concerning is that NRZ’s servicers are distressed, particularly Ocwen and Ditech (more on this later).

2. NRZ has no servicing platform

Because NRZ has no servicing platform, they rely on outside servicers in which they have very little influence. In some regards, this has been a good thing because it has protected NRZ from some of the lawsuits and regulator scorn that have plagued the servicers. However, it’s also been a negative because NRZ is not an attractive buyer for sellers of MSRs that prefer to sell MSRs and their servicing platform in a single transaction. The separation of MSR owners and their servicing platform adds significant complexity and makes operations more challenging for NRZ.

3. Ocwen is in big trouble

One of NRZ’s biggest service providers, Ocwen (OCN) is in big trouble. Specifically, its net income is consistently negative, its debt is getting close to 100% of its assets, its credit rating has been downgraded and is low, it continues to deal with regulators and lawsuits, and its stock price is down about 95% since 2013.

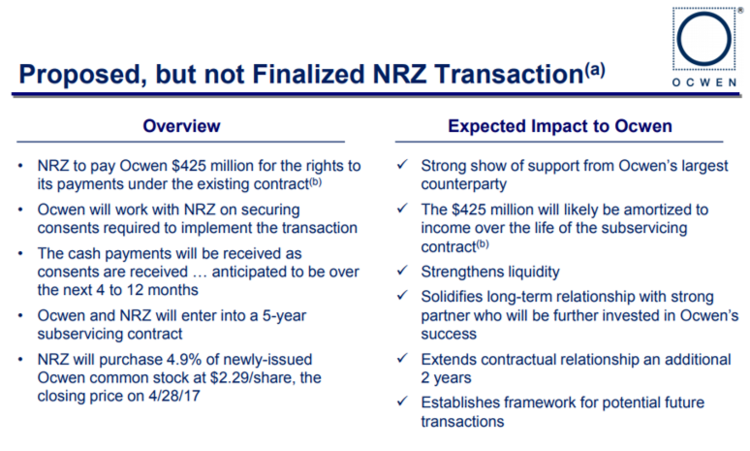

Recognizing the dangers to NRZ if OCN goes out of business, NRZ management has recently proposed a transaction whereby they’ll paying OCN a proposed $425 million in exchange for rights and newly issued OCN shares as described in the following graphic.

When asked about the transaction, NRZ’s Michael Nierenberg explained: “Quite frankly, we will continue to work with Ocwen, any which way we can but being mindful that we need to protect our shareholders.”

Basically, Michael is acknowledging the risk that if OCN goes bankrupt then NRZ is in big trouble because a lot of their rights become worthless (as described in risk #1, above). But at the same time, NRZ wants to be carefully not to expose its shareholders to the legal and regulatory risks that Ocwen continues to face. It’s a tricky situation.

Nierenberg went on to explain “We believe this [transaction] is the best for us, the best for Ocwen and the best for the entire system. And… if you think about it, there is a number of winners in this transaction. First and foremost, the mortgage loans do not get moved from one servicer to another. So we think from a consumer perspective that’s a great thing. That’s one. Two is, from a liquidity perspective, this gets Ocwen on the right track.”

If Ocwen doesn’t get back on the right track, NRZ is in big trouble. And this is both an opportunity (for NRZ to opportunistically increase its investments by purchasing things from Ocwen at fire sale prices), and a big risk (if OCN doesn’t survive) that NRZ investors should be aware of.

4. Walter Investment Management is in big trouble.

Walter Investment Management, (WAC) the owner of Ditech (another one of NRZ’s largest servicers) is also in distress, and this is a big risk for NRZ investors. Similar to OCN, WAC is consistently delivering negative net income, its share price has declined dramatically, and the company continues to deal with lawsuits and regulator scorn.

Further, NRZ has recently acquired investment from WAC (see our earlier MSR Overview graphic for recent WAC acquisitions) as both an opportunistic investment opportunity, and as a way to support WAC because NRZ doesn’t want WAC to go bankrupt (this would be very bad for NRZ and bad for the whole system). Worth noting, NRZ does less business with WAC than it does with OCN, and therefore WAC poses a less risk to NRZ than does OCN (but it is still significant).

5. Changing Prepayment Speeds

Another risk to NRZ is if prepayment speeds accelerate. As mentioned previously, rising interest rates help NRZ’s MSR portfolio because less people refinance their mortgage when interest rates have gone up, and this means NRZ get to make money for a longer period of time for owning MSRs and Excess MSRs. However, any significant change to prepayment speeds (caused by lower interest rates, new regulation, or simply more defaults) could have a significantly negative impact on NRZ.

6. Overconfident Securities Trading and Leverage

Another growing risk for NRZ is simply overconfidence in trading residential securities. As noted previously, the residential securities holdings of NRZ have increased dramatically in recent years, and this increases some risks. For example, according to NRZ’s quarterly report; “We leverage certain of our assets through a variety of borrowings.”

Leverage can make magnify returns in the good times, but also magnify losses in the bad times. According to NRZ’s quarterly report “our determination of how much leverage to apply to our investments may adversely affect our return on our investments and may reduce cash available for distribution.” Further: “Our investment guidelines do not limit the amount of leverage we may incur with respect to any specific asset or pool of assets. The return we are able to earn on our investments and cash available for distribution to our stockholders may be significantly reduced due to changes in market conditions, which may cause the cost of our financing to increase relative to the income that can be derived from our assets.” Simply, the growing size of NRZ’s residential securities portfolio combined with its use of leverage creates very significant and growing risks for shareholders.

7. Wells Fargo Recently Withheld Money

Another risk was recently introduced when three weeks ago Wells Fargo surprised investors by holding back over $90 million from buyers of pre-financial-crisis residential mortgage-backed securities. The funds were withheld after NRZ exercised a “clean up call” on the debt. Basically, Wells Fargo has been named as a defendant in some lawsuits, and is holding back funds for legal expenses. This is a new risk for NRZ, and (according to Bloomberg) some experts expect Wells to withhold more money as NRZ exercises more clean up call rights.

8. External Management Team

Another risk for investors to keep in mind is that New Residential is externally managed by an affiliate of Fortress Investment Group (Fortress is also the majority shareholder in Nationstar Mortgage, one of New Residential’s largest servicers). This is important because there are conflicts of interest. For example, according to New Residentials’s annual report: “Our Management Agreement with our Manager was not negotiated between unaffiliated parties, and its terms, including fees payable… may not be as favorable to us as if they had been negotiated with an unaffiliated third party.” Further still, in February, Fortress announced it will become a wholly owned subsidiary of a SoftBank affiliate. All of these items are important because it can be a distraction to management, and it can create conflicts of interest in the way the companies are operated.

Reasons to be Optimistic

1. Housing crisis impacts continue to shrink

Despite the big risks facing NRZ as described above, there are also a variety of reasons to be optimistic. For example, the housing crisis is further in the rear view mirror. This means less distress across the industry (for both MSR owners and servicers). And this means less volatility and less risk.

2. Improved Servicers

Another reason to be positive is because servicers (e.g. Ocwen, WAC) have significantly cleaned up their act in recent years. For example, conditions at these servicers have improved after many lawsuits and regulatory requirements. Even though the prices are way down, there is good reason to believe there will be far less distress going forward than in recent history.

3. Industry Cooperation

Another reason to be positive is that NRZ is helping its servicers, and we’ll probably learn of more examples in the near future. For example, we described earlier how NRZ provided liquidity for Ocwen and WAC by acquiring investments. This was good for the servicers (they need the support), good for NRZ (the prices were very attractive), and good for the system (it’s mutually beneficial for NRZ to work with its servicers because they need each other to survive). Further still, it’s good for mortgage owners because they don’t need the headaches of a servicer bankruptcy either.

Worth noting, the details have been light since last quarter’s announcement that NRZ was working on a deal to support Ocwen. NRZ announces earnings again on July 31st, and we expect to receive more details. Further, we won’t be surprised to learn that NRZ may have expanded the deal significantly to provide more support to Ocwen. This could be good for all parties involved.

4. Opportunities for Good Deals

Yet another reason to be optimistic about NRZ is that, to some extent, it is in a position of power relative to its servicers, and this will help enable NRZ to make some really good deals whereby they have the upper hand. For example, if NRZ continues to purchase investments from Ocwen and Ditech, they’ll be doing so at discounted prices. As 18th century British nobleman Baron Rothschild is purported to have said: “buy when there is blood in the streets.”

5. Investors are afraid

Sticking with the theme of “buy when there is blood in the streets,” another reason to be optimistic is that a lot of fear has already been baked into NRZ’s price. The shares fell significantly in June, and they’ve not yet fully recovered as investor fear remains high.

6. The Dividend is Strong

NRZ’s dividend also remains high and it is well covered. For example, last quarter, NRZ’s core earnings of $155 million, or $0.54 per diluted share exceeded the first quarter dividend of $0.48 per common share. Further still, NRZ has increased its dividend two quarters in a row in a sign of confidence to investors (it’s currently $0.50 per share).

Conclusion:

NRZ management won’t just buy its service providers outright if they can avoid it because they want to protect NRZ shareholders from all the legacy (and potentially new) risks (regulatory and legal risks), but they probably will buy them if they have too because NRZ is in big trouble if mortgage holders (and bond holders) fire the servicers (because then NRZ’s MSRs have no value). Plus this situation would be bad for mortgage owners because they don’t necessarily want to go through the added headache of dealing with a new servicer.

We can speculate that we’ll get a lot of big news within the next few weeks (earnings season) about new deals that will be good for NRZ because they’ll reduce the chance of service provider bankruptcies, and NRZ will probably be getting some good “fire sale” prices on investments acquired. The big question though is, will it be enough to keep the service providers out of bankruptcy without acquiring pieces of business that put NRZ shareholders at risk (i.e. NRZ doesn’t want to acquire the legacy liabilities of wrongdoings by service providers). Overall, we take a positive view of the situation because the industry has been cleaned up a lot since the financial crisis (less lawsuits and regulatory risks) and because it’s in the system’s best interest to not create new turmoil for mortgage holders and bondholders. We’ve owned shares of NRZ within our prudently diversified Blue Harbinger Income Equity portfolio since May 2016. The dividend yield on our initial purchase price is now 15.7%.

Disclosure: None.