Monthly Dividend Stock In Focus: Choice Properties REIT

Income investors tend to be primarily looking for a high dividend yield, a safe and predictable dividend payment, and the possibility of dividend growth down the road.

It is hard to find stocks that possess all three characteristics. Some asset classes have a much higher probability of delivering on these goals than others.

Real estate investment trusts – or REITs, for short – can be a fantastic source of yield, safety, and growth for dividend investors.

Choice Properties Real Estate Investment Trust (PPRQF), (CHP-UN.TO) offers investors two of the three. The trust’s 5%+ dividend yield certainly allows it to satisfy the ‘high yield’ requirement.

Choice Properties also pays its dividends on a monthly basis, which is rare in a world where the vast majority of companies that pay a dividend, pay them quarterly.

Choice Properties’ high dividend yield and monthly dividend payments make it an intriguing stock for dividend investors, even though its dividend payment has been stagnant in recent years.

This article will analyze the investment prospects of Choice Properties.

Business Overview

Choice Properties is a Canadian real estate investment trust with concentrated operations in many of Canada’s largest markets.

Choice Properties is one of Canada’s premier REITs given its size and scale, and the fact that its operations are solely focused in Canada. The trust has bet big on Canada’s real estate market, and thus far, the strategy has worked.

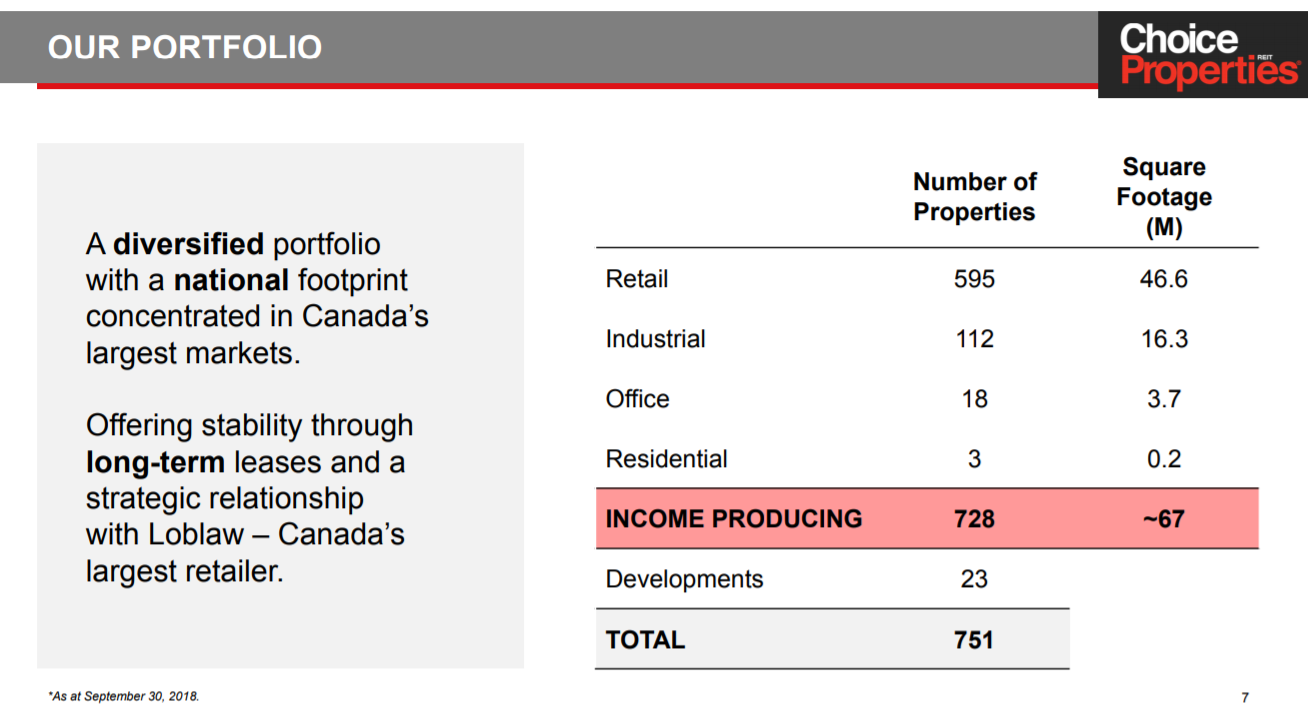

Choice Properties owns 751 properties, 728 of which are income-producing at this point. Its portfolio is worth in excess of $16 billion and it has more than 67 million square feet of space to lease.

Source: Investor presentation, page 7

The trust’s portfolio consists primarily of retail properties, but it also owns a significant amount of industrial real estate.

In addition, many of its new developments are focused on office and residential space, respectively, as it looks to diversify a bit in the coming years.

Source: Investor presentation, page 8

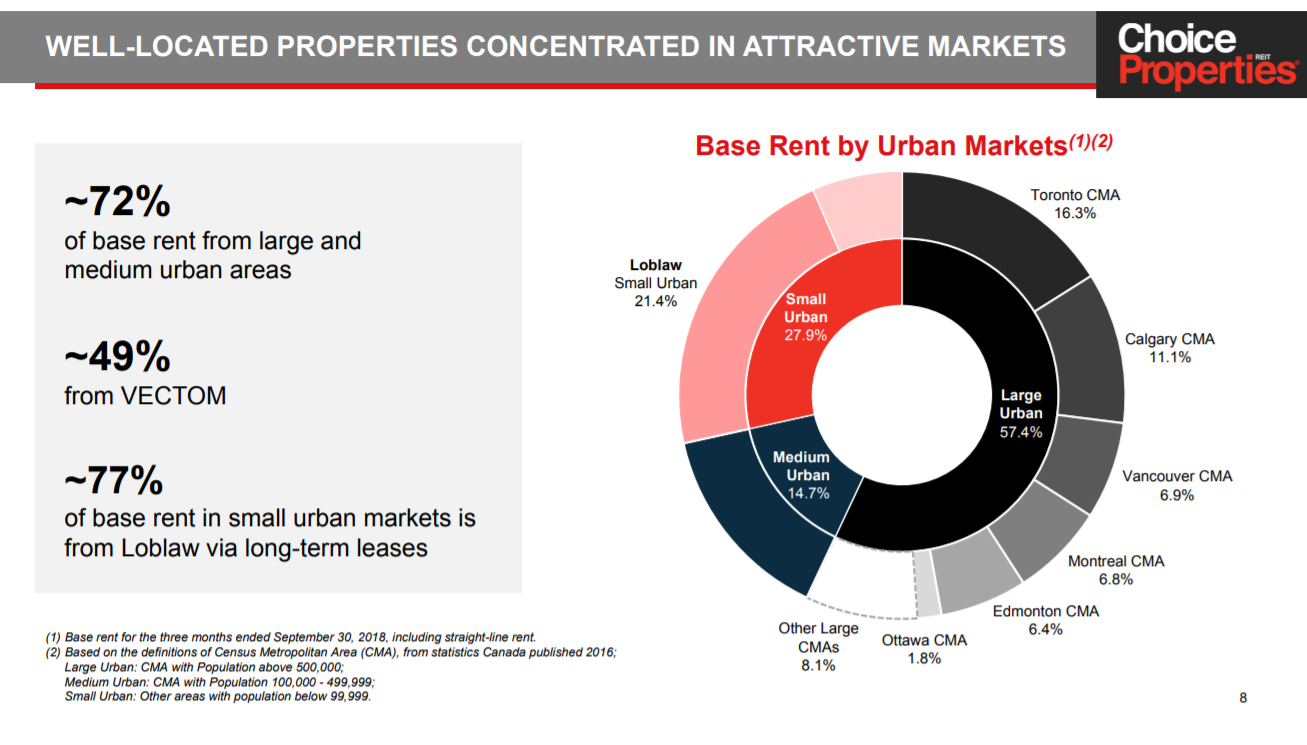

Choice Properties is present in multiple markets across Canada. The trust’s strategy is to focus on mid- to large urban areas in Canada, and it has resulted in the concentrations you see above.

More than half of the portfolio is concentrated in large urban areas, while the balance is a mix of small and mid-sized cities.

From an investment perspective, Choice Properties has some interesting characteristics, not the least of which is its yield. However, it also has an unusual dependency on one tenant, a lack of diversification that we find somewhat troubling.

Source: Investor presentation, page 9

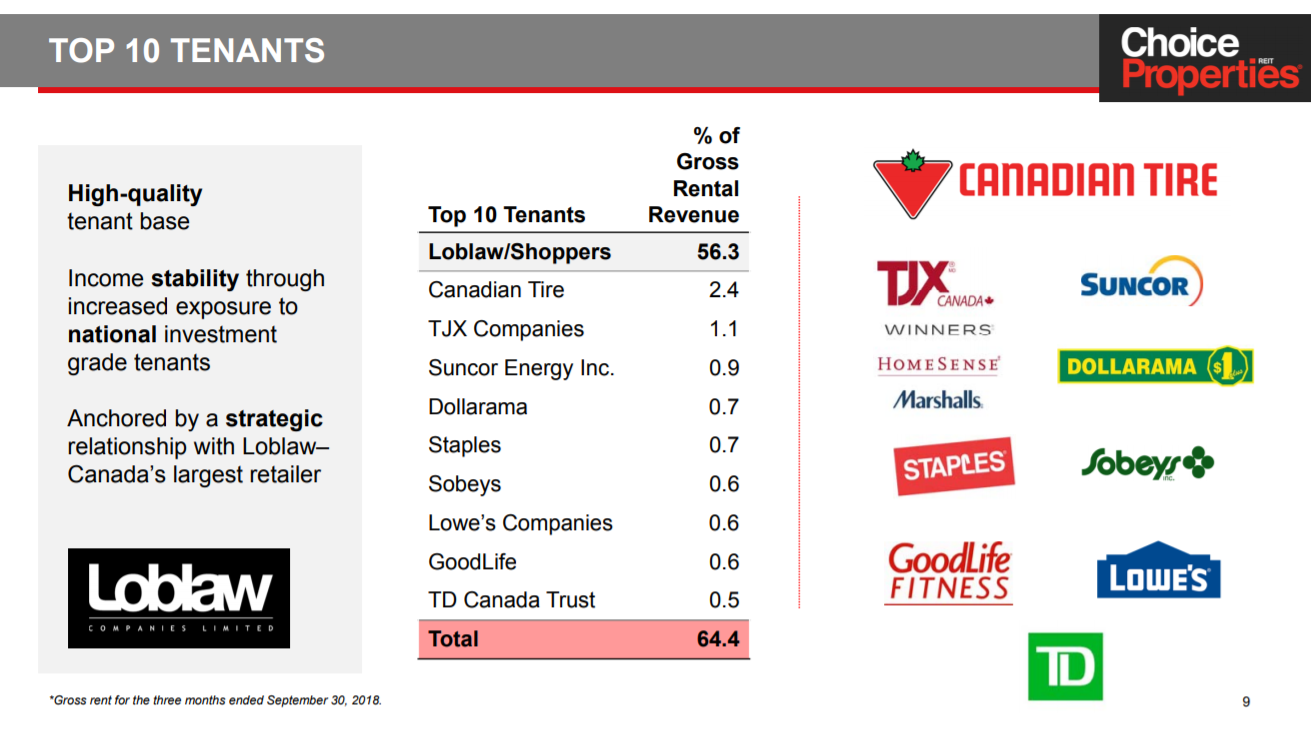

Loblaws and Shoppers combined make up a staggering 56% of Choice Properties’ gross rental revenue. The trust has taken care to diversify itself within Canada’s various markets but has bet in an enormous way on the future of Loblaws and Shoppers.

While grocery stores and drug stores, respectively, are generally quite stable, this level of concentration on what amounts to one tenant is very rare. This lack of diversification is a significant consideration for investors that are looking at Choice Properties.

While it would be preferable for the company to diversify to fix its concentration, that is a slow process.

Growth Prospects

Choice Properties has struggled with growth since it came public in 2013. Since the end of 2014, the trust’s first full year of operations as a public company, it has compounded adjusted funds-from-operations per share at a rate of just 2.6%.

The trust has grown steadily in terms of portfolio size and revenue, but relatively high operating costs and dilution from share issuances have kept a lid on returns for shareholders.

In 2018, Choice Properties showed strong growth characteristics consistent with prior years’ results, but once translated to a per-share basis, investors were left wanting.

Revenue rose a staggering 43% over 2017 thanks almost entirely to new properties. Net operating income rose 41% in 2018 but only 2% of that was due to comparable property net operating income growth.

In other words, Choice Properties’ organic growth rate has been and remains in the low single digits, although it does have a history of acquiring large amounts of growth.

The problem is that it acquires this growth largely via new shares, which dilutes away much of the potential gains for existing shareholders in terms of acquisitions. As an example, total adjusted FFO rose 36% on a dollar basis in 2018, but on a per-share basis, it fell over 4%.

Choice Properties hasn’t had a difficult time expanding, but when growth is largely financed by dilution, the impact on shareholders is sizable.

We see Choice Properties as continuing to grow very slightly, if at all, in the coming years. The concentration of the trust’s portfolio and constant dilution make Choice Properties unattractive from a growth perspective.

Dividend Analysis

For all of its growth woes, Choice Properties’ dividend appears to be secure for the time being. The 2018 payout ratio on adjusted FFO-per-share was just under 90%. While that is high, it is also true that REITs generally distribute close to all of their income.

Choice Properties’ current distribution gives the stock a 5.3% yield, which is quite good attractive high dividend yield.

Investors should not expect Choice Properties to be a dividend growth stock. The distribution has remained flat since May 2017.

Choice Properties hasn’t cut the distribution, and we don’t see an imminent threat of that right now. But it is worth mentioning that if FFO-per-share deteriorates significantly going forward, the trust will likely have to cut the distribution due to its high payout ratio.

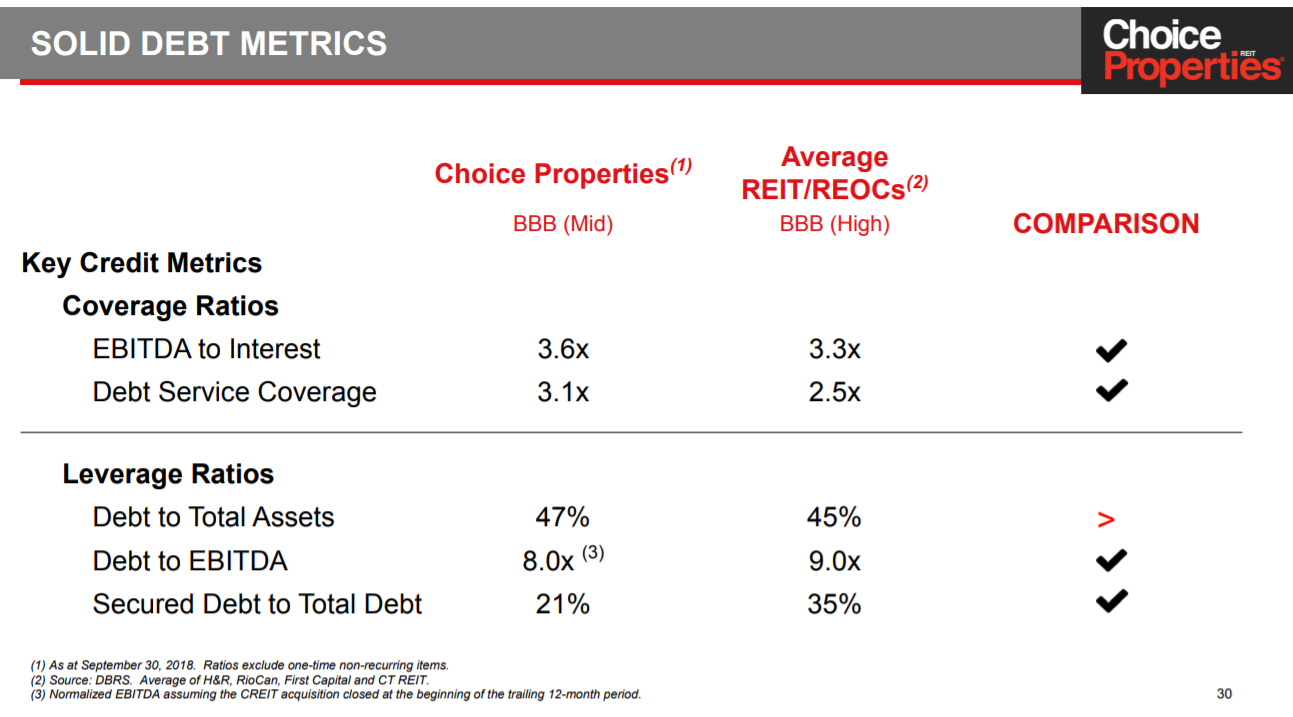

This is particularly true because we see Choice Properties’ borrowing capacity as limited, given its already-high leverage.

Source: Investor presentation, page 30

Choice Properties has debt to EBITDA of 8X, which according to the company is below the industry peers, but is still alarmingly high.

In addition, it has large amounts of debt coming due in stages in the coming years, so we see the trust’s debt financing as near capacity today.

Should it experience a downturn in earnings, Choice Properties would have to turn to more dilution for additional capital.

While we don’t see a dividend cut in the near future, the combination of a lack of adjusted FFO-per-share growth, the ~90% payout ratio, and a high level of debt as risky, despite the high dividend yield.

Final Thoughts

Choice Properties’ high dividend yield and monthly dividend payments make it stand out to high yield dividend investors. However, a number of factors make us cautious on Choice Properties today.

With the stock up more than 20% thus far in 2019 and a risky dividend, we view the stock as unattractive. Investors looking for a REIT that pays monthly dividends have much better choices with more favorable growth prospects, higher yields, and safer dividends.

Disclaimer: Sure Dividend is published as an information service. It includes opinions as to buying, selling and holding various stocks and other securities. However, the publishers of Sure ...

more