Image Source: Pixabay

High-yield stocks pay out dividends that are significantly higher than the market average. For example, the S&P 500’s current yield is only ~1.2%.

High-yield stocks can be particularly beneficial in supplementing income after retirement. A $120,000 investment in stocks with an average dividend yield of 5% creates an average of $500 a month in dividends.

Next on our list of high-dividend stocks to review is Apple Hospitality REIT Inc. (APLE).

Business Overview

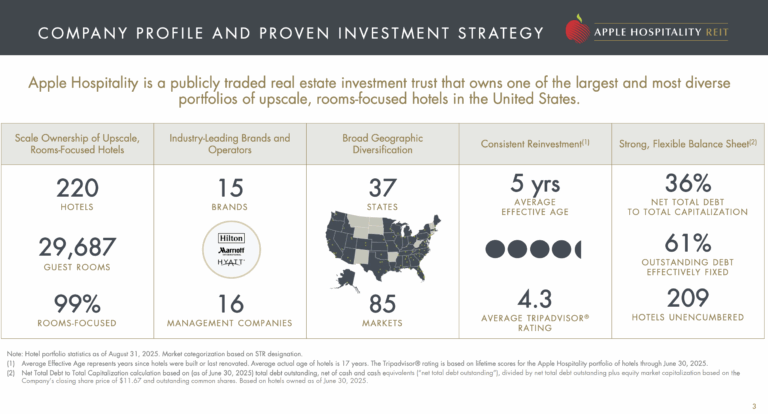

Apple Hospitality REIT, Inc. (NYSE: APLE) is a publicly traded real estate investment trust focused on owning and operating upscale, rooms‑focused hotels across the United States.

Headquartered in Richmond, Virginia, the company’s portfolio includes 221 hotels with nearly 30,000 guest rooms in 37 states and the District of Columbia, primarily under Marriott, Hilton, and Hyatt brands.

The company emphasizes geographic diversification, disciplined capital allocation through acquisitions and dispositions, and consistent distributions to shareholders, aiming to generate both income and long-term capital appreciation from strategically located lodging assets.

Financially, Apple Hospitality has demonstrated resilience in hotel operations, with net income of approximately $214 million and operating income of $292 million in 2024, supported by modest gains in occupancy, average daily rate, and revenue per available room.

As of early 2025, the company carries around $1.5 billion in debt with a debt-to-capital ratio of 33%, providing some financial flexibility.

While the diversified, branded hotel portfolio offers yield potential for investors, risks include sensitivity to economic cycles in travel demand, rising operating costs, and interest rate fluctuations, which may impact overall performance.

Source: Investor Relations

The company reported Q3 2025 results with net income of $50.9 million, down 9.6% year over year, and EPS of $0.21, which slightly missed expectations.

Revenue totaled $373.9 million, slightly above estimates, while comparable hotel metrics showed minor declines: ADR of $162.68 (-0.6%), occupancy of 76.2% (-1.2%), and RevPAR of $124.01 (-1.8%). Adjusted EBITDAre was $122.1 million, and MFFO was $100.5 million, both reflecting year-over-year decreases. Distributions remained steady at $0.24 per share.

During the quarter, the company acquired the 126-room Homewood Suites Tampa-Brandon and entered contracts for future acquisitions, including a dual-branded Las Vegas development.

Three hotels were sold for $37 million, with four more under contract for $36 million. Capital improvements totaled $50 million year-to-date, with projected 2025 expenditures of $80–90 million.

Apple Hospitality maintains financial flexibility with $50.3 million in cash, $1.515 billion in total debt, and a net debt-to-capital ratio of 34%.

The company repurchased 3.8 million shares year-to-date for $48.3 million and continues to pay monthly distributions, yielding ~8.6% annually.

Management remains confident in the long-term outlook, citing a strong branded hotel portfolio and disciplined capital allocation.

Growth Prospects

Apple Hospitality REIT’s growth prospects reflect a shift from its earlier rapid expansion to a more moderate pace in the current hospitality landscape.

Historically, the company delivered impressive annualized FFO per share growth, driven by strategic scale increases—including a major merger in 2015—an efficient operational model, and favorable economic conditions in the U.S.

However, recent years have been marked by slower growth, primarily due to the COVID-19 pandemic’s severe impact on travel and hotel demand, compounded by competition from alternative lodging platforms like Airbnb.

Looking forward, analysts project more modest growth, with FFO per share, NAV per share, and dividends expected to grow at approximately 1% CAGR.

While this represents a slowdown from the company’s earlier trajectory, Apple Hospitality’s established portfolio of branded hotels, disciplined capital allocation, and ongoing development and acquisition initiatives provide a foundation for stable, incremental growth.

The company’s focus on optimizing operations and selectively expanding into high-potential markets positions it to generate consistent shareholder returns despite a challenging macroeconomic environment.

Source: Investor Relations

Competitive Advantages & Recession Performance

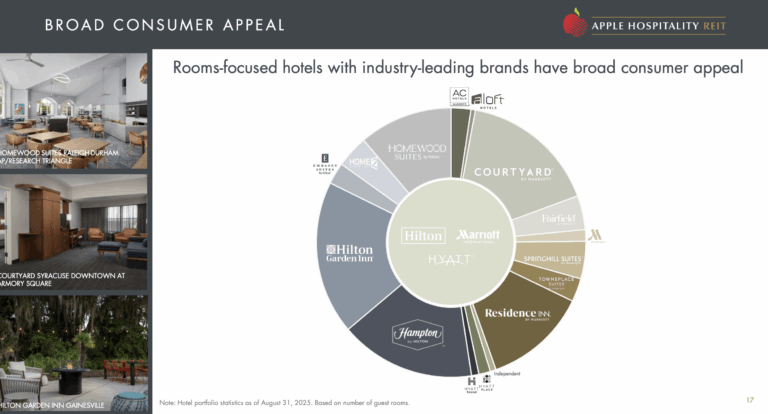

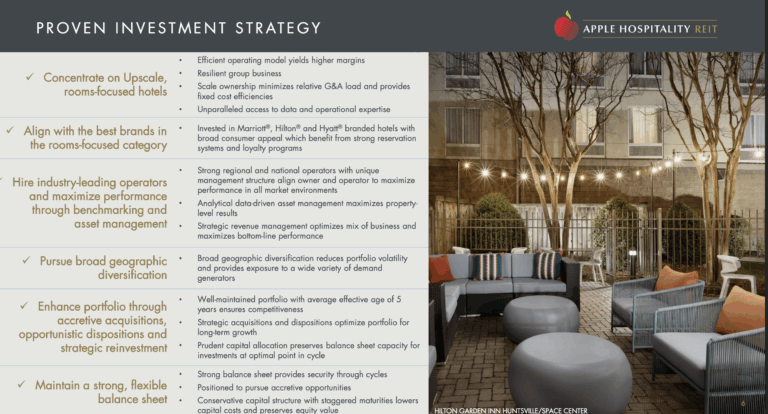

Apple Hospitality REIT’s competitive advantages stem from its large, branded hotel portfolio—including Marriott, Hilton, and Hyatt—which provides strong brand recognition, geographic diversification, and appeal to both business and leisure travelers.

Its scale enables operational efficiency, centralized management, and disciplined capital allocation through acquisitions, dispositions, and selective development, supporting consistent cash flow and investor returns.

The company has shown resilience during economic downturns. By focusing on well-located, branded properties across diversified markets, Apple Hospitality mitigates the impact of recessions on occupancy and RevPAR.

Its strong balance sheet, flexible capital structure, and consistent distribution strategy allow it to navigate volatility while maintaining long-term shareholder value.

Source: Investor Relations

Dividend Analysis

The company has a relatively short dividend history, having gone public in 2015. It pays dividends monthly, which appeals to income-focused investors.

The company significantly increased its annualized dividend in 2016 from $0.80 to $1.20 per share, but the payout remained flat until 2020, when the COVID-19 pandemic forced a reduction to $0.30 for the year. Dividends resumed in 2021, and APLE currently pays $0.08 per month, or $0.96 annually.

The company’s strong balance sheet supports its dividend, with low debt-to-equity, ample liquidity, and a well-structured debt maturity profile.

The projected 2025 dividend payout ratio of roughly 61% of FFO suggests the dividend is secure under normal conditions, though a severe recession could pressure it.

While APLE lacks a long track record of navigating recessions, its portfolio of well-located, branded hotels, solid balance sheet, franchising model, and focus on value should allow it to outperform peers in downturns, even if the hotel sector typically faces significant income declines during economic slowdowns.

Final Thoughts

Apple Hospitality REIT is a leading player in the hotel sector, supported by strong brand recognition, a conservative balance sheet, and a portfolio of high-quality assets. Its current dividend yield of 8.9% also appealing to income-focused investors.

While we project annualized returns of approximately 10.3% over the next five years, the stock receives a sell rating due to its lack of consistent dividend growth, though its total return potential remains reasonable.

More By This Author:

High Dividend 50: Atrium Mortgage Investment Corporation10 Best Dividend Stocks For Reducing Risk

High Dividend 50: Cardinal Energy

Comments

Log in or sign up to join the conversation.