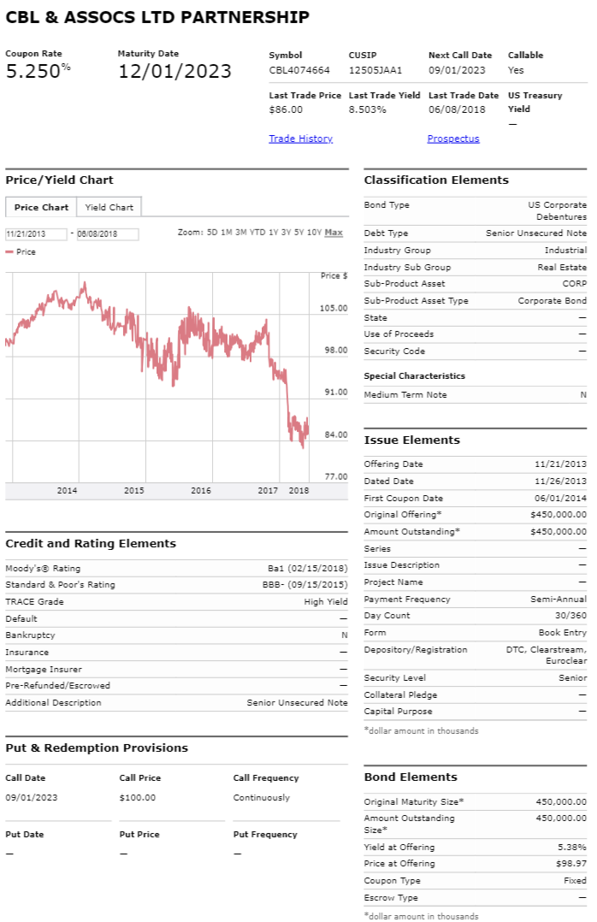

CBL's High-Yield Bonds Are Increasingly Attractive (6.1% Yield + Price Appreciation)

Every investor has their own unique needs and tolerance for risk, and no one has a working crystal ball. Nonetheless, by assembling a prudent mix of portfolio investments, every individual can increase their odds for success.

And depending on your situation, the 6.1% yield coupon payments on CBL’s 2023 bonds (they pay a 5.25% coupon at par, but currently trade at a discounted price of 86 cents on the dollar, 5.25% / 0.86 = 6.1%), may be a far better investment option than CBL’s equities (common and preferred), especially considering the bonds recently fell sharply to less than par (i.e. the 86 cents on the dollar thing) thereby providing the opportunity for a double digit percentage gain in price (perhaps sooner than later) and that’s in addition to the 6.1% yield, paid semiannually.

Note: This report was originally released to Blue Harbinger members on June 8th.

CBL & Associates Properties, Inc (CBL)

If you don’t know, CBL is one of the largest owners and developers of malls and shopping centers in the United States. And performance for this REIT has been terrible, as shown in the following chart.

CBL’s Common Equity (CBL), Yield: 13.9%

CBL has been dealing with a variety of challenges that have caused the price to decline dramatically. For starters, shopping malls have been facing new, growing, disruptive online competition from the likes of Amazon, for example. And it doesn’t help that CBL’s properties are not the attractive experiential A-class properties that command higher rents, more foot traffic, and less rent concessions.

Rising interest rates pose another challenge for REITs like CBL. Because they are required to pay out most of their income as dividends, REITs rely heavily on borrowing to fund their businesses; therefore REITs (like CBL) can be particularly sensitive to rising rates (i.e. it increases their significant borrowing costs). Compounding this challenge, many market participants had been utilizing REITs as a bond-like proxy considering bond yields were so low and REITs offer relatively high income. But as bond yields rise, REITs become less attractive to many investors, thereby putting further pressure on the market price of REIT securities.

Finally, as many investors are painfully aware, CBL reduced its big dividend recently. And considering the shares have fallen so far, and the yield is so high, many investors are worried another dividend reduction (or worse) could be on the horizon. We’ll have more to say about CBL’s cash flows later in this report.

CBL’s Preferred Stock, Yield: 9.6%

With so much fear surrounding CBL’s common equity, some investors are considering CBL’s preferred stocks. CBL’s series D preferred shares trade at a discounted $19.50 per share and offer a 9.6% dividend yield. And the series E trades at $17.52, also offering a 9.6% yield.

After all, the preferred shares offer attractive yield, less historical volatility, and they’re higher in the capital structure. And while all of these things are true, that doesn’t mean the preferred shares won’t get completely wiped out in a bankruptcy situation. Sure, the preferreds are technically safer than the common, but not that much safer, in our view. Plus the preferreds don’t offer the same upside potential as the common if CBL actually is able to pick itself up by its bootstraps. Further still, the preferred shares are particularly sensitive to rising interest rates considering the share price will fall as interest rates rise, ceteris paribus. However, unlike bonds, there is no stated maturity on the preferreds, so they can be even more sensitive to rising interest rates than bonds maturing in the nearer future.

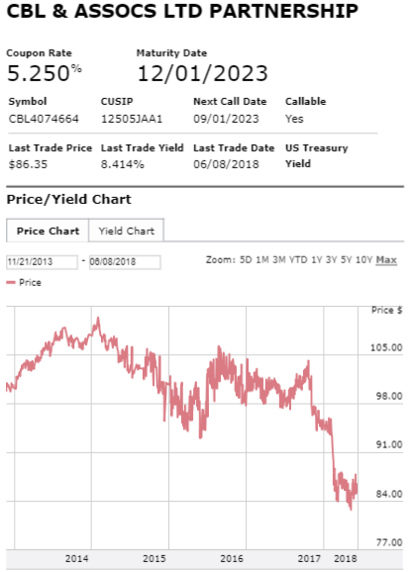

CBL’s 2023 Bonds, Yield: +8.5%

One attractive quality of CBL’s bonds is that when they cut the common equity dividend, it freed up more cash to support the bonds. Like preferred shares, bonds are higher in the capital structure than common stock. However, unlike the preferred shares, the bonds higher position in the capital structure (higher than even the preferreds) does make a significant difference because in a bankruptcy situation bondholders are far less likely to get completely wiped out, and they may even be made whole if the equity shares are completely wiped out. The higher position in the capital structure for CBL’s debt is actually worth something quite significant, in our view.

Before taking a position on the attractiveness of the various CBL bonds, it’s worth considering the company’s current and historical cash position.

CBL’s Cash Position:

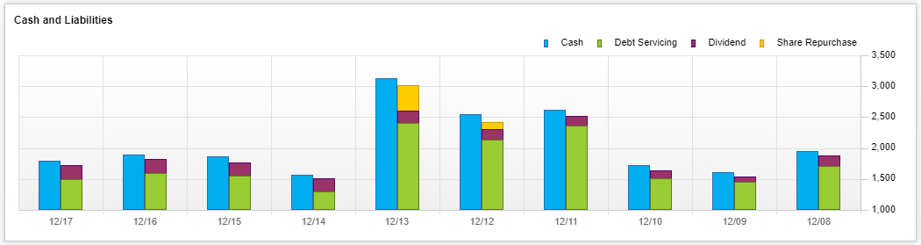

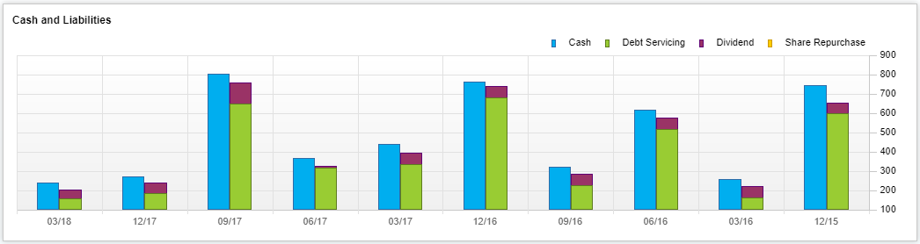

Cash flow levels are critically important to consider when dealing with increasingly challenged companies, like CBL. And for starters, here is a look at CBL’s historical cash relative to debt servicing, dividend payments.

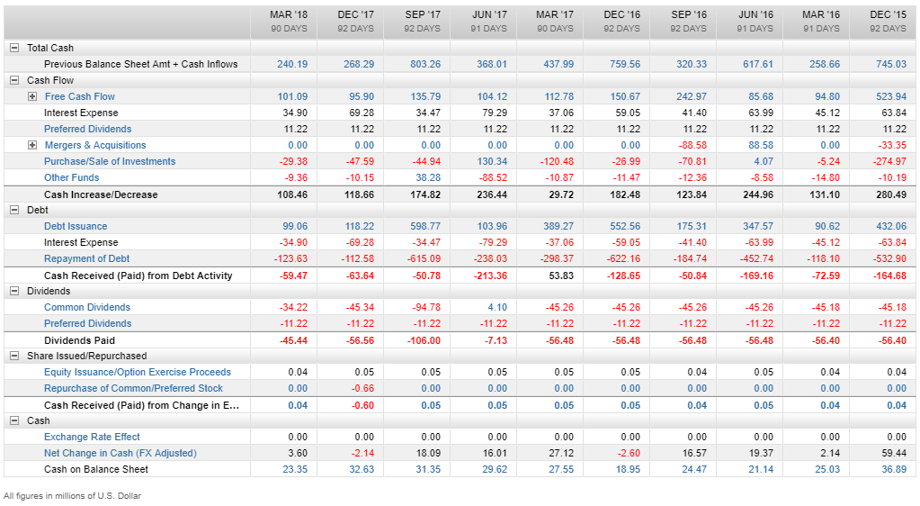

As would be expected, the margin of cash after dividend payments has historically been tight. And for more detail, here is a look at the same data, only on a quarterly basis (instead of annual) and with more detail (including preferred versus common dividends, and debt issuance and repayments, for example) in table format.

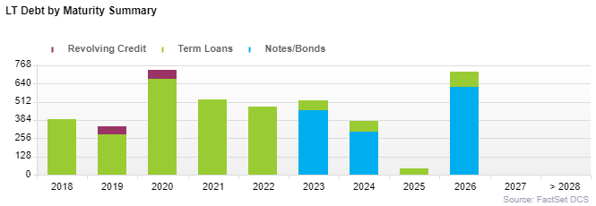

Worth noting, the above table shows the ongoing outflows of cash related to debt (after netting debt issuances, interest expense, and debt repayments). This outflow becomes more concerning when considering interest rates are expected to keep rising (debt will become more expensive) and CBL has considerable debt coming due in future years, as shown in the following table.

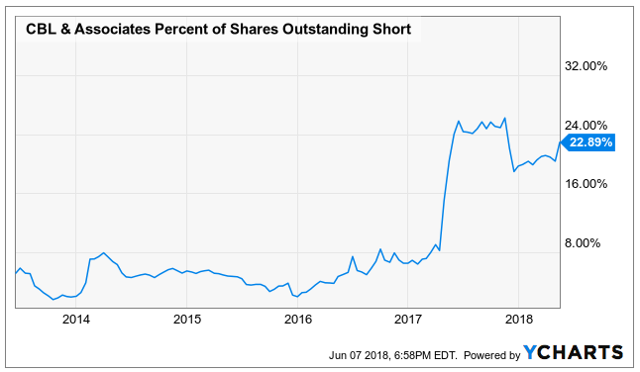

Worse still, cash flows will be challenged going forward as online sales continue to disrupt “brick and mortal” sales (e.g. CBL) thereby forcing continued retailer bankruptcies and rent concessions for many of those that maintain a brick and mortar presence (i.e. CBL tenants). These very real challenges, combined with considerable market fear, are a big part of the reason why short interest is so high for CBL.

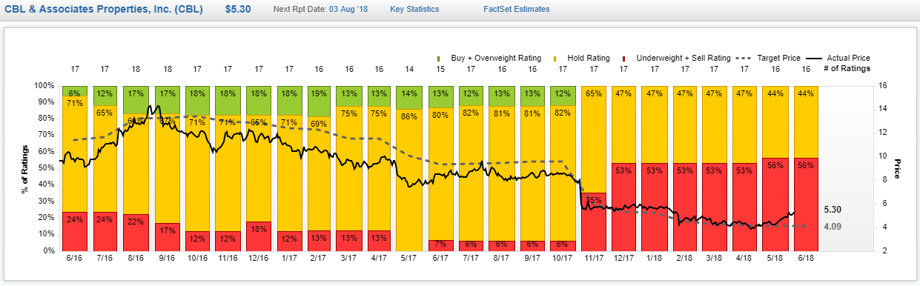

Further, most of the 16 Wall Street analysts covering the stock have a “sell” recommendation, and the group continues to lower its CBL price targets, as shown in the following graphic.

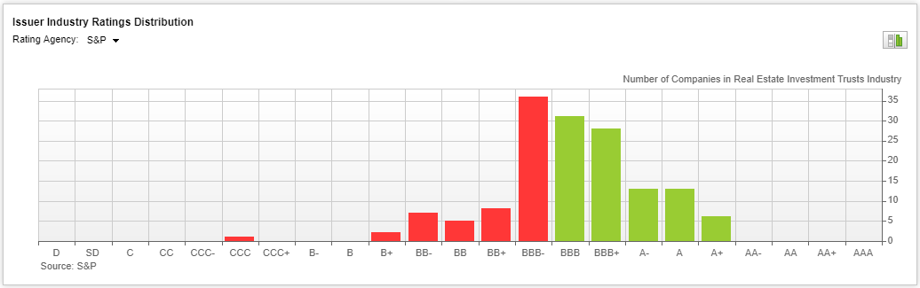

CBL’s challenges are also why the rating agencies have a negative outlook for the debt.

And worth noting, the debt is already rated low compared to other REITs.

Why CBL’s High-Yield Debt Is Worth Considering:

So given all of the negative and concerning CBL metrics, why would anyone consider investing in the bonds? Here are three important reasons...

1. The dividend provides cushion for the bonds:

If you’re worried CBL will run out of cash to pay the bonds, remember they’ve already reduced the dividend once to free up cash, and the can sill do it again. Here is a look at recent quarterly cash versus debt servicing and the dividend. It’s a little lumpy depending on the date when the quarter ends versus when the payments are made, but the point is the dividend continues to provide cushion for the debt.

CBL’s shopping malls aren’t all just going to be shut down overnight. They’re going to keep operating for years, and they’re going to keep providing cash flow for years. And that cash flows goes to the debt first because it’s highest in the capital structure.

2. CBL Bonds Have Just Gotten Cheap: As shown in the following chart, CBL’s bonds have sold-off recently:

The sell-off has to do with fear. Specifically, the bonds sold off in sympathy with the equity when the equity dividend was cut. In reality, the dividend cut was a good thing for the bonds, in our view (because it frees up cash). Also, we suspect the bonds will rebound closer to par long before they mature in 2023. To put that in perspective, if these bonds rally back to just $98 (a price they traded near all of last year) that’s a 14% price gain. And that’s in addition to the big coupon payments you are buying at a discount.

3. Management is still fighting, and optimistic...

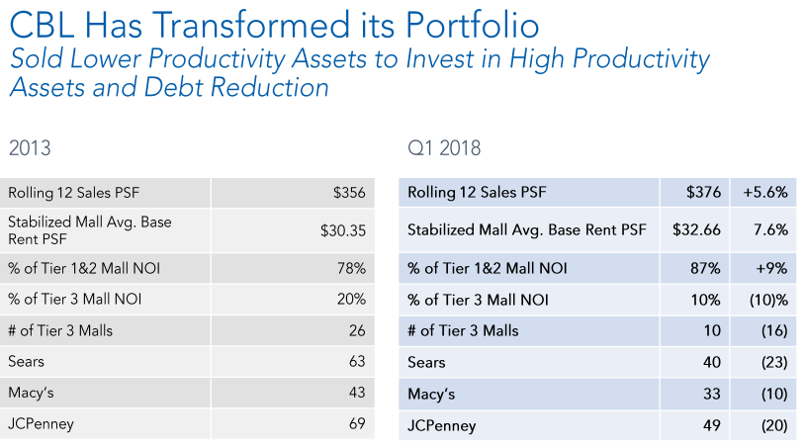

According to CBL’s latest investor presentation, management is still fighting hard (i.e. this does not sound like a business that is going to disappear overnight). For example, here is a look at CBL’s strategic priorities (note, enhancing the balance sheet is a priority—good news for bondholders).

And specifically, CBL has been selling lower productivity assets to help increase productivity and reduce debt (again, good for the bondholders).

These are not the actions of a company that is going to disappear overnight. CBL is woking to improve its long-term position, and this is very good for the bonds. As another good sign, CBL announced this week that it was able to obtain a 5-year extention of over $110 million in debt. This is another good sign for CBL’s outstanding debt, such as the 2023 bonds, for example. Plus, retailer bankruptcies are expected to lessen from last year, and retail sales have been surprisingly strong.

Conclusion:

The market is overly fearful about CBL bonds, and the recent sell-off has created an attractive entry point, in our view. We acknowledge CBL's common equity could have much more upside, but it also comes with much more risk. And while some investors like the preferred shares, we're not comfortable that the preferreds won't get entirely wiped out in the unlikely case of a bankruptcy, whereas the bonds would likely be made whole or at least very close to whole (i.e. we expect the bonds to pay in full).

And if you're looking for an attractive coupon payment with prospects for some healthy price appreciation too (perhaps far sooner than the bonds mature), CBL's 2023's are worth considering. For the reasons described in this article, we've added these CBL bonds to our ranking of 5 increasingly attractive high-yield opportunities (which includes preferred stocks, bonds, and common equity), and we continue to believe it can be very worthwhile to consider opportunities from all across the capital structure, particularly if you are an income-focused investor.

Disclosure: I am/we are long CBL BONDS.

Disclosure: None.

Thanks for sharing this, you seem to really know your stuff and hit on a good find with $CBL. I will check out your site for more pearls of wisdom.