Image Source: Unsplash

Motivation for turning family offices into investment banks

Real estate investment trusts (REITs) have recently outperformed other conservative investment strategies focused on income and wealth preservation, offering both dividend payments and capital appreciation. Even considering the recent increases in interest rates, REITs have continued to perform well.

Amid the growing volatility sweeping through the markets daily, diversification has become more important than ever, and real estate is an important part of diversification. However, investing in real estate doesn't necessarily mean owning properties, which is what many investors think of when someone suggests that they invest in the sector.

REITs outperform private real estate holdings

A study conducted by the pension benchmarking firm CEM Benchmarking looked at the performance of pension fund investments between 1998 and 2019, including various methods of investing in real estate. The study was published in October 2021 and cited by Wealth Management.

Researchers found that publicly traded REITs outperformed all other types of real estate investments over those 22 years. In addition to REITs, they looked at directly owned real estate, real estate funds of funds, value-added or opportunistic real estate funds, and core real estate funds. For the purposes of this article, we will only look at REITs and directly owned real estate.

The researchers found that REITs generated an average annual net return (excluding managers' fees) of 10.68%. Internally managed, directly owned real estate generated an average net return of 10.1%, while funds holding externally managed, directly owned real estate averaged an annual net return of 8.34%.

The differences between these real estate investment types might not seem like much, but when you add them up over 22 years, the gap is significant.

Importantly, the study also found that all the methods of investing in real estate included in the study offered comparable benefits in terms of diversification. Volatility of returns was also similar across all types of real estate investments after adjusting for lags in reporting. This is also a key finding because conventional thinking suggests that private real estate investments are significantly less volatile than publicly traded REITs.

While this study may be meaningful for retail investors (who may not be looking at their management fees!), we would like to show how a little financial engineering can yield dramatic results for family offices that lever their real estate investments and use those investments to originate publicly traded REITs, especially in an environment where the forward-looking yield expectation for REITs is 3%, not 10%.

The Family Office Perspective: Turning private real estate portfolio investments into REITs

Now let's look at the REIT versus direct real estate holdings comparison from a different perspective. Let's say we buy a $100 million real estate portfolio consisting of hotels or multifamily residential units. Typically, deals of this type are highly levered.

For example, if we are acquiring $100 million in real estate with $10 million in fees and capital improvements, we would typically seek to arrange about $70 million in bank financing and $30 million in preferred equity. The actual equity investment ends up being only $10 million, which means we are using over 90% leverage on this transaction.

Let's say the portfolio’s net operating income is $10 million a year in aggregate, and we manage to boost the net operating income to $12 million a year. We will soon discover that the $10 million equity investor actually enjoys a sizable return.

In this article, we will explore the underlying financial engineering of REITs and compare it to the returns enjoyed by real estate investors who go the private equity route. We will consider the differences to see why it might be a wise move to take your private real estate portfolios public through the creation of publicly listed REITs.

Since COVID shut down hotels, and many multifamily residential properties saw a dramatic rise in rent delinquency, landlords have experienced stress in meeting their debt obligations and return expectations.

However, we are now witnessing a rapid return to normal in travel heading into the summer, and with record-low unemployment, rent delinquency is also returning to normal levels. Consequently, on a forward-looking basis, we believe that hotel operating income and multifamily property yields should return to historical norms.

In speaking with investors in these real estate asset classes, we believe that significant portfolios of mid-tier properties can be purchased with an eight- to 12-cap valuation (e.g. the acquisition price is based on discounting net operating income at an 8% to 12% discount factor) on a medium-term, forward-looking basis, including modest capital investment.

When constructing an illustrative real estate portfolio acquisition, we can learn a lot by looking at how a deal can be structured to show the different returns expected by the various investor classes. Let’s examine the expected returns to:

a) 70% bank debt with 30-year amortization at 4% interest,

b) Preferred equity with 10% interest-only annual payments and a 10% equity kicker

c) Equity investor with subordinated return of investment at exit, plus 60% equity in the project, and

d) The management team with a 5% management fee and 30% residual equity upon exit.

Summary of Deal Terms:

The power of compounding interest is clear.

A portfolio expected to produce $10 million per year in cash flow on a steady-state basis when discounted at a 10% discount factor is valued at $100 million. This comes out of the formula for a perpetuity (a bond that has a steady cash flow forever), where the value of the bond is calculated as the cash flow divided by the discount factor (e.g. $10 million per year cash flow / 10% discount factor has a present value of $100 million).

By improving the asset to $12 million per year in net operating income and selling to an investor that values net operating income at a 7% discount factor, the asset would have a valuation of $171 million ($12 million net operating income / 7% discount factor).

In the REIT world, where REITs are valued at a 3% discount factor, the same portfolio would be valued at $400 million ($12 million net operating income / 3% discount factor)!

In this illustration, we are acquiring a portfolio for $100 million, and investing $10 million in fees and capex. Over the course of the three years, the income increases to $12 million.

To simplify the illustration, the portfolio throws off a net income of $10 million / year for three years, at which time the portfolio is sold at a seven-cap rate on $12 million / year net income, with 5% in fees, resulting in net proceeds of $162.9 million, providing $65.7 million available to be distributed among the equity participants.

This payout analysis shows how the different investor classes are compensated:

Payout Analysis:

In this illustration, the equity investor is receiving a 70% investment rate of return after a three-year exit while still leaving a healthy return for the preferred equity and a rich payout for the deal team. A key driver of this outsized return is the 90% leverage enjoyed by the equity investor.

The purpose of this article has been to explain and motivate owners of private real estate portfolios to form public REITs to enable:

a) Maximum valuation

b) Monetization over time while also planning for taxes and distribution of assets among family members, and

c) Maintaining management control, leveraging of equity investment and creation of a platform to make acquisitions and aggregate assets under management through investment from public investors.

This article presents the analysis underlying a presentation I gave on March 30 at the Family Office Experiences conference in Dubai. The title of the presentation was: “Strategies for Leveraging U.S. Capital Markets: Turning family offices into investment banks.”

The Vanguard Real Estate Index Fund ETF (NYSE: VNQ) helps put the industry in perspective. It basically represents direct ownership in the largest REITs and currently has over $83 billion in assets with a yield of just over 2%.

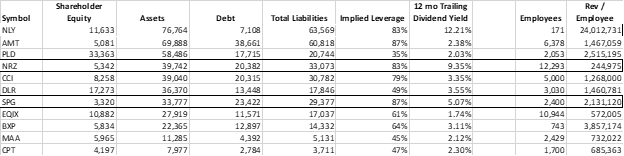

This grid shows the performance of a few REITs, ordered by total assets under management:

Source: Yahoo Finance, 27 Mar 22. All financial numbers are $ million

Two interesting REITs are NLY and NRZ. Both have outsized yields (12% and 9%) relative to the industry, where the shares have been pricing approximately a 3% yield.

A statistic that jumps out from the table is the number of employees and revenue per employee. NLY and NRZ are the opposite, with NLY having the smallest number of employees and highest revenues per employee, while NRZ has the largest number of employees and lowest revenue per employee while still enjoying a yield three times higher than the typical REIT. Both NLY and NRZ primarily invest in mortgages and financial instruments and are not direct holders of real estate assets.

Simon Property Group (SPG), a leading operator of premier shopping, dining, entertainment and mixed-use destinations, is a direct owner and operator of real estate assets and also has a significantly higher yield than the other REITs, although not in the same category as leveraged financial asset investors.

These examples illustrate the two approaches to achieving high returns: a) financial engineering with leverage and low-cost capital and b) boots on the ground with excellence in branding and operations management.

Summing it up: The benefits of public offerings

The dramatic rise in U.S. stock market valuations has prompted many to be concerned about the risk/ reward of being invested at record-high valuations, not just on high-flying tech stocks, but as illustrated by the low REIT yields, even in real estate investment vehicles.

Source: Yahoo Finance, 28 Mar 22

The purpose of this article is not to provide directional advice on going long the market or picking tops. We all know the adage of the economist who predicted 10 of the last five recessions. Historically, picking tops and bottoms is not a winning strategy. The analysis above has shown that:

a) There is a significant gap between private and public valuations, which motivates taking investment portfolios public, and

b) Using simple financial engineering, returns to equity investors can be significantly increased.

Comments

Log in or sign up to join the conversation.