The Zacks Mortgage & Related Services industry continues to suffer from the receding mortgage origination tide. Rising mortgage rates continue to affect mortgage volumes, particularly refinancing. While purchase origination is expected to drive overall volumes in the future, housing shortages and market volatility are near-term headwinds. The macro-economic scenario has also been unhelpful for the industry. The central bank is expected to increase rates amid rising inflation. However, uncertainties arising from the Russia-Ukraine war continue to drive market volatility in the near term.

Nonetheless, expectations of higher housing demand on growth in consumer spending should help mortgage-related stocks to generate higher returns in the near future. This, along with portfolio diversity and technological enhancements, is anticipated to keep Essent Group Ltd. (ESNT - Free Report) , Walker & Dunlop, Inc. (WD - Free Report) and Velocity Financial, Inc. (VEL - Free Report) afloat.

Industry Description

The Zacks Mortgage & Related Services industry comprises providers of mortgage-related loans, refinancing and other loan-servicing facilities. Numerous banks have been retreating from the mortgage business due to higher compliance and capital requirements. This provided an opportunity for non-banks to shore up the capacity to increase market share in the mortgage loans business, which accounts for the largest class of U.S. consumer debt. Players in the industry are somewhat dependent on the interest rates determined by the Federal Reserve, as prevailing rates influence customers' decisions to apply for mortgages. The companies also generate investment income from several financial assets such as residential or commercial mortgage-backed securities, and asset-backed securities. Further, the firms make equity investments in mortgage-related entities, among others.

3 Mortgage & Related Services Industry Trends to Watch

Rising Rates to Hinder Origination Volume: Amid the tight labor markets and all-time high inflation level, the Federal Reserve is in the midst of a shift from quantitative easing to tightening, with a reduction in asset purchases and rising short-term interest rates. These are likely to result in yield curve flattening, with a rise in short and intermediate-term rates. Also, the Russian invasion of Ukraine might influence Fed’s monetary policy decisions for the ongoing year. Since the yield curve impacts the path of mortgage rates, the macro-economic backdrop indicates that mortgage rates will witness an uptick in the upcoming period. These factors are likely to lead to lower origination volumes, especially refinancing, as incentives for borrowers to refinance loans are likely to fade. This might impede revenue growth.

Competition to Affect Pricing: House price appreciation, rebound in the economy, and continued GDP growth are likely to drive U.S. single-family mortgage debt outstanding in the upcoming years, underlining growth of the industry players’ single-family mortgage portfolios. Yet, customer acquisition for the mortgage services industry is becoming more competitive due to housing shortages. Notably, numerous companies have witnessed significant declines in gain-on-sale margins and lower weighted average rate on loans originated. With tighter margins, many originators might struggle to remain profitable in the upcoming period, especially with trending mortgage rates.

Regulatory Changes Might Limit Origination Capacity: Mortgage originators are significantly dependent on the government-sponsored enterprises' (GSEs) programs for the origination of a majority of loans for sale. Hence, any change to the conservatorship of Freddie Mac and related actions, or a revamp in regulations (affecting the relationship between Freddie Mac, other GSEs and the federal government) might affect the mortgage service providers. Further, since a significant chunk of the substantial majority of the industry players' servicing portfolios represents loans serviced through the GSEs' programs, changes in the business charters, structure, or the existence of Freddie Mac or other GSEs could reduce the number of loans that originators can produce with the GSEs. This might reduce revenues from loan originations and servicing fees, affecting business and financial performance.

Zacks Industry Rank Reflects Dismal Prospects

The Zacks Mortgage & Related Services industry, housed within the broader Zacks Finance sector, currently carries a Zacks Industry Rank #207, which places it in the bottom 17% of more than 250 Zacks industries.

The group's Zacks Industry Rank, which is basically the average of the Zacks Rank of all the member stocks, indicates bleak prospects in the near term. Our research shows that the top 50% of the Zacks-ranked industries outperforms the bottom 50% by a factor of more than 2 to 1.

The industry's positioning in the bottom 50% of the Zacks-ranked industries is a result of a negative earnings outlook for the constituent companies in aggregate. Looking at the aggregate earnings estimate revisions, it appears that analysts are gradually losing confidence in this group's earnings growth potential. Over the past year, the industry's earnings estimates for the current year have been revised 37.6% downward.

Before we present a few stocks that you may want to consider for your portfolio, let's take a look at the industry's recent stock market performance and the valuation picture.

Industry Underperforms Sector and S&P 500

The Zacks Mortgage & Related Services industry has underperformed the broader Zacks Finance sector and Zacks S&P 500 composite over the past year.

The industry has declined 49.4% during this period against the broader sector's rise of 3.5%. The S&P 500 composite has grown 6.2%.

One-Year Price Performance

Image Source: Zacks Investment Research

Industry'' Current Valuation

On the basis of the price-to-book ratio (P/B), which is commonly used for valuing mortgage loan providers, the industry currently trades at 1.35X compared with the S&P 500's 6.35X.

Over the last five years, the industry has traded as high as 2.43X, as low as 0.78X, and at the median of 1.84X, as the chart below shows.

Price-to-Book Ratio (TTM)

Image Source: Zacks Investment Research

As finance stocks typically have a lower P/B ratio, comparing mortgage loan providers with the S&P 500 may not make sense to many investors. But a comparison of the group's P/B ratio with that of its broader sector ensures that the group is trading at a decent discount. The Zacks Finance sector's trailing 12-month P/B of 3.19X for the same period is above the Zacks Mortgage & Related Services industry's ratio, as the chart shows below.

Price-to-Book Ratio (TTM)

Image Source: Zacks Investment Research

3 Mortgage & Related Services Stocks to Keep a Close Eye on

Essent Group is engaged in providing private mortgage insurance for single-family mortgage loans in the United States. The company offers private capital to mitigate mortgage credit risk, facilitating lenders to make additional mortgage financing available to prospective homeowners.

Last month, the company cheered investors with a 5.3% sequential dividend hike. By leveraging programmatic reinsurance, the company has transformed its business model from “Buy and Hold” to “Buy, Manage & Distribute.” This helps shape the portfolio risk profile and mitigate return volatility during down cycles. Also, macro tailwinds like a rebound in homeownership rates and encouraging first-time buyer activity are aiding ESNT.

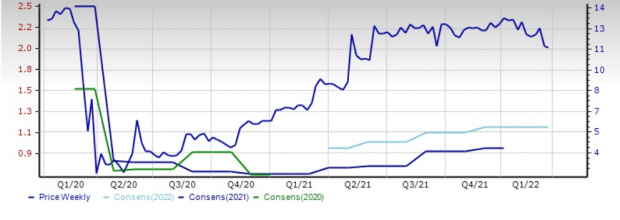

Zacks Consensus Estimate for ESNT’s 2022 earnings has been revised marginally upward over the past month. Also, its earnings for the ongoing and the following year are projected to witness year-over-year growth of 7% and 0.7%, respectively. The company currently carries a Zacks Rank of 2 (Buy).

Price and Consensus: ESNT

Image Source: Zacks Investment Research

Velocity Financial: Based in Westlake Village, CA, Velocity Financial is a vertically integrated real estate finance firm, which offers and manages investor loans for 1-4 unit residential rental and small commercial properties. VEL originates loans across the United States through its extensive network of independent mortgage brokers.

Considering the increased economic activity, supported by market normalization and the reopening of the economy, the demand for investor properties is anticipated to remain robust. This is expected to drive investor loan demand. Given Velocity Financial's expanded liquidity capacity, it is well-poised to capitalize on growth in the addressable market and, thereby, fund loan volume in the upcoming period.

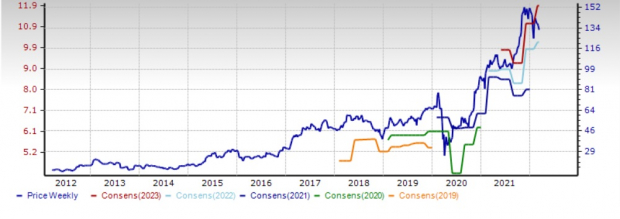

The Zacks Consensus Estimate for VEL's 2022 and 2023 earnings has been unchanged over the past month. Also, for the ongoing and the next year, its revenues are expected to increase 12.8% and 26.4%, respectively. The company carries a Zacks Rank of 3 (Hold) at present.

Price and Consensus: VEL

Image Source: Zacks Investment Research

Walker & Dunlop: Based in Bethesda, MD, Walker & Dunlop is one of the largest U.S. providers of capital to the multifamily industry and the fourth-largest lender for all commercial real estate, including industrial, office, retail and hospitality. The company's expansion strategies, and strengthening of the online lending platform through acquisitions are likely to drive the top line. Further, Walker & Dunlop's commitment to capturing market share on the back of heavy investments in artificial intelligence and machine-learning capabilities is commendable.

Of late, the company has been making expansion moves, including acquisitions and additional hirings. Last month, WD closed a deal to acquire GeoPhy, a commercial real estate technology company.Walker & Dunlop paid $85 million in cash in addition to $205 million in cash earn-out potential. The cash earn-out potential is structured to directly align with the company’s Drive to '25 goals of growth in appraisal revenues, loan volumes and mortgage banking gains.

The Zacks Rank #3 company’s earnings estimates have been revised upward 7.9% and 10% for 2022 and 2023, respectively, over the past month. Walker & Dunlop's earnings for the ongoing and the following year are projected to witness year-over-year growth of 25% and 16.4%, respectively.

Price and Consensus: WD

Image Source: Zacks Investment Research

Comments

Log in or sign up to join the conversation.