Real Corporate Profits Are Now The Lowest Since The Financial Crisis

Ask any Wall Street analyst why stocks are at all-time highs and the instant answer will be because profits and net income are similarly at or near all-time highs, which means that the multiple needed to justify an S&P around 3,150 is not all that egregious. But is that really the case in a world where virtually everything is fake or otherwise "adjusted" to fit a given narrative?

First, consider that one of the more surprising revelations in the aftermath of WeWork's "community adjusted" EBITDA debacle is that there is never just one cockroach and that virtually all companies are just as guilty of aggressively abusing GAAP accounting standards. Case in point, a few weeks ago, the WSJ reported that nearly all big companies now use at least one non-GAAP financial metric. In fact, last year 97% of S&P 500 companies used non-GAAP metrics, up from 59% in 1996, according to Audit Analytics.

Last week, Factset picked up on this point in a report showing that while all publicly traded U.S companies report EPS on a GAAP (generally accepted accounting principles) basis, most US companies also choose to report EPS on a non-GAAP basis.

To be sure, we have reported in the past that there are "mixed opinions" in the market about the use of non-GAAP EPS. Supporters of the practice - typically the very management teams that hope to paint their results in a far stronger light - argue that it provides the market with a more accurate picture of earnings from the day-to-day operations of companies, as items that companies deem to be one-time events or non-operating in nature are typically excluded from the non-GAAP EPS numbers.

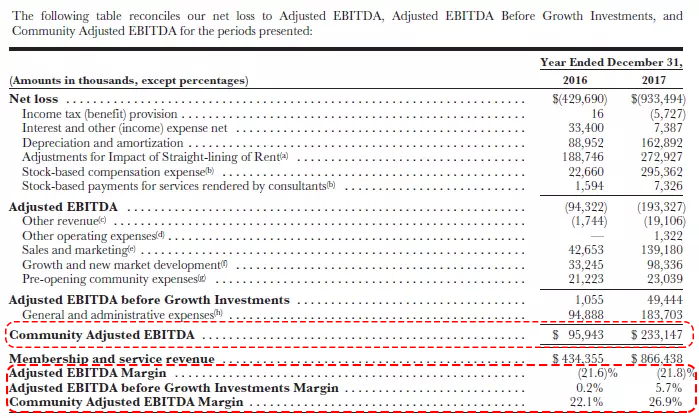

On the other hand, critics of the practice including such iconic names as Warren Buffett (even though his own companies aggressively engage in non-GAAP fudges), argue that there is no industry-standard definition of non-GAAP EPS, and companies can take advantage of the lack of standards to exclude items that (more often than not) have a negative impact on earnings to boost non-GAAP EPS. WeWork's "community adjusted" EBITDA is just one example:

(Click on image to enlarge)

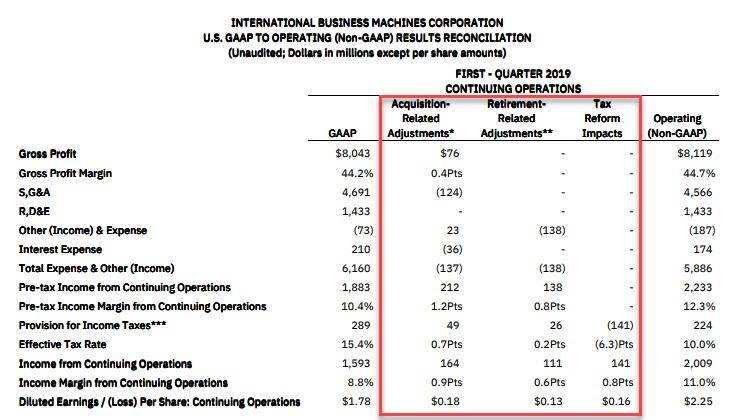

Others include serial abusers IBM (whose recent GAAP to Non-GAAP reconciliation is shown below)...

(Click on image to enlarge)

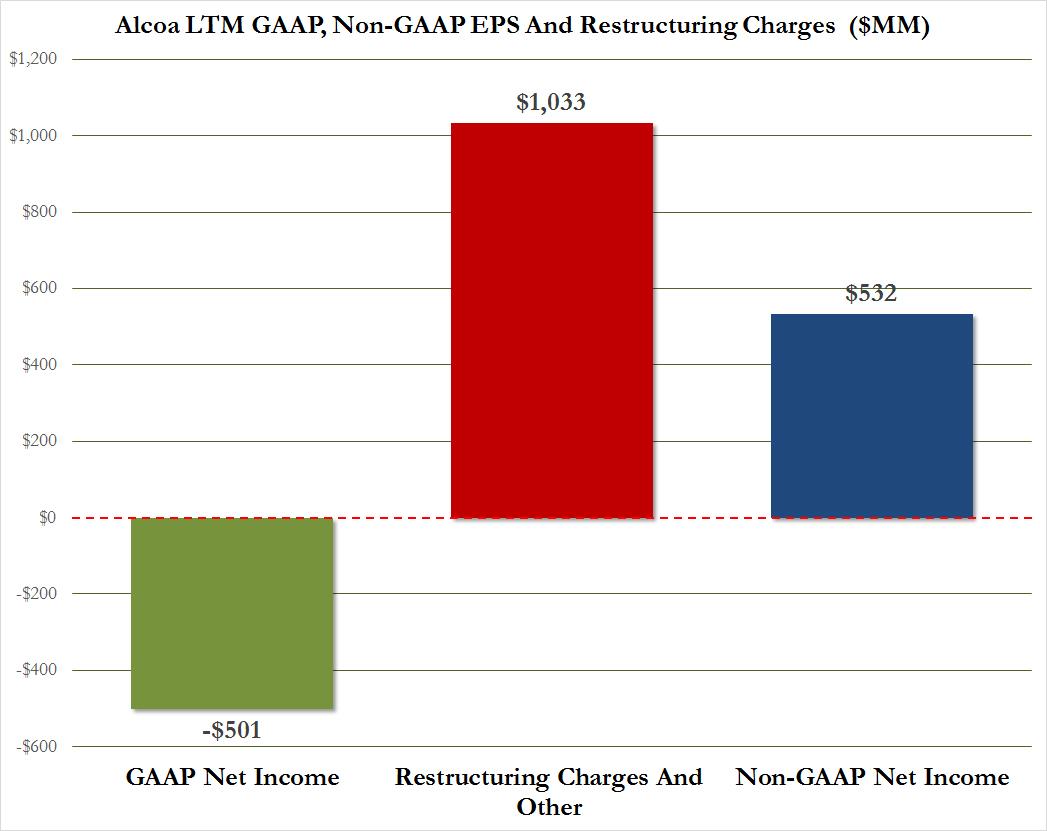

... and Alcoa AA, which every quarter roughly double their non-GAAP net income by recurringly adding back "one-time, non-recurring" items.

(Click on image to enlarge)

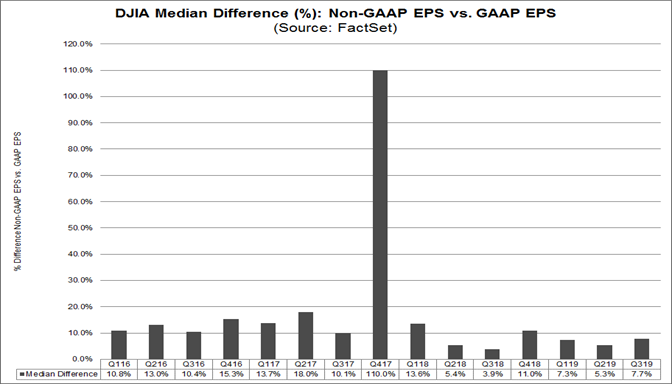

Here a quick case study: now that Q3 earnings season is over, what percentage of the companies in the Dow Jones reported non-GAAP EPS for Q3 2019? What was the median difference between non-GAAP EPS and GAAP EPS for companies in the DJIA for Q3 2019? How did these differences compare to recent quarters?

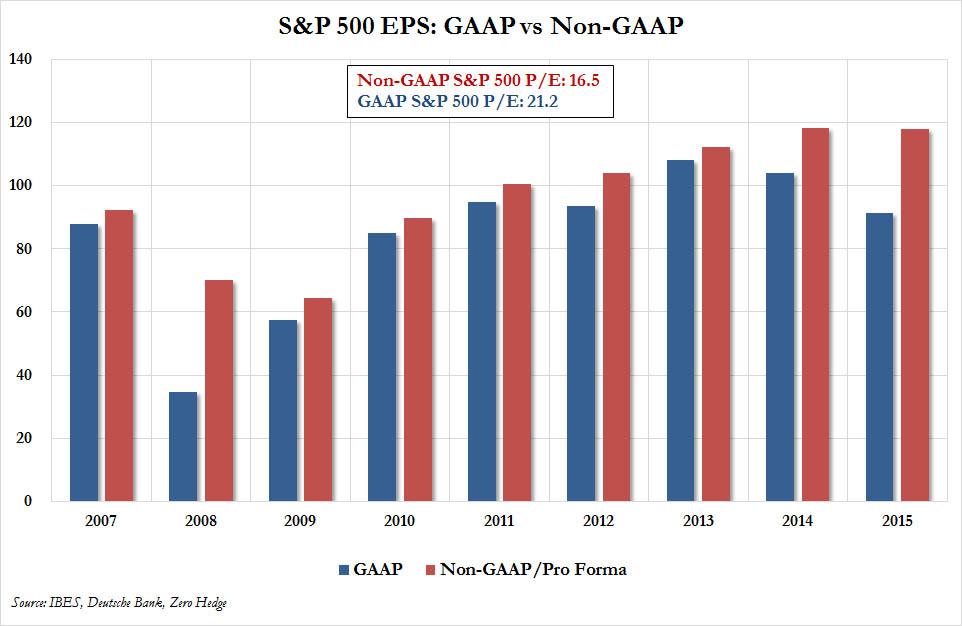

An analysis we conducted not too long ago of GAAP vs non-GAAP EPS showed a dramatic divergence between the two series, with the former peaking in 2013 and declining ever since, even as non-GAAP profits have continued to rise.

(Click on image to enlarge)

Fast forward to today, when FactSet points out that since 2016, 73% of companies in the DJIA have reported non-GAAP EPS in addition to GAAP EPS on average. Of these 20 companies, it will not come as a surprise to anyone that since 2016, 75% of companies in the DJIA reported non-GAAP EPS that exceeded GAAP EPS on average. The median difference between non-GAAP EPS and GAAP EPS companies was 7.7%. Since 2016, the median difference between non-GAAP EPS and GAAP EPS has been 10.9%.

(Click on image to enlarge)

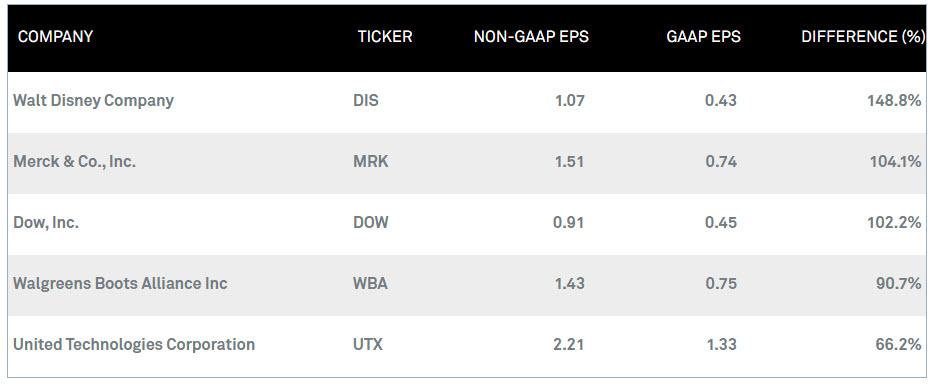

While the median number may not be so shocking, the top 5 outliers surely are. Indeed, when looking at the five biggest non-GAAP adjusters in the DJIA, Factset found that in Q3 2019, the average difference between GAAP and Non-GAAP EPS is about 100%, with Walt Disney DIS the most flagrant abuser, pumping up its GAAP EPS of $0.43 into a non-GAAP EPS of $1.07, some 149% higher!

(Click on image to enlarge)

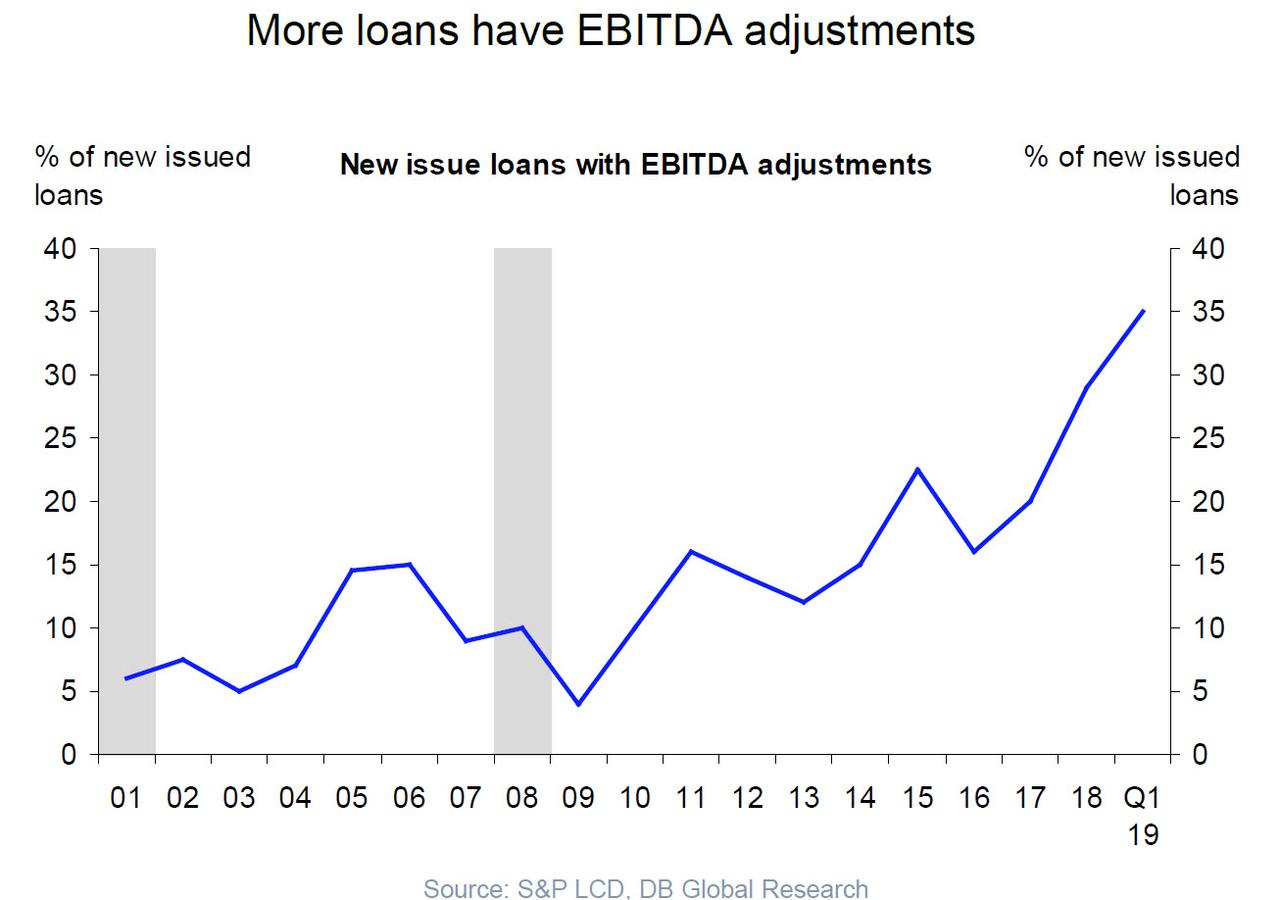

Of course, corporations adjust their results not only when reporting earnings - for many of them, a stronger adjusted EBITDA also means the difference between locking in that much-needed loan or bond offering or facing insolvency. It is here that the abuse of GAAP reality is even more dramatic: the following chart from S&P LCD showing the percentage of new issue loans that come with EBITDA adjustments speaks for itself.

(Click on image to enlarge)

Fine, so most companies are "putting lipstick on themselves" and lying about how financially viable they really are. That is hardly a surprise - what is far more surprising is that this practice continues unabated, and that "adjusters" continue to get full credit for their EBITDA adjustments. Interestingly, such flagrant adjustments as "community-adjusted EBITDA" continue to take place long after the SEC launched a crackdown on non-GAAP accounting gimmicks. As we reported back in 2016, the SEC's chief accountant said that "we are going to look harder at the substance of what companies are presenting, rather than what the measures are called."

Alas, after looking, the SEC appears to have done nothing because it was just a few months ago that WeWork's "community adjusted" EBITDA farce was still gracing the pages of its financial presentations in order to justify its $47 billion valuation. And more shockingly, nobody on Wall Street cared, until a few weeks ago when the collective psychosis suddenly ended, and WeWork went from one of the world's most valuable companies to insolvent and needing a bailout from SoftBank in a matter of days.

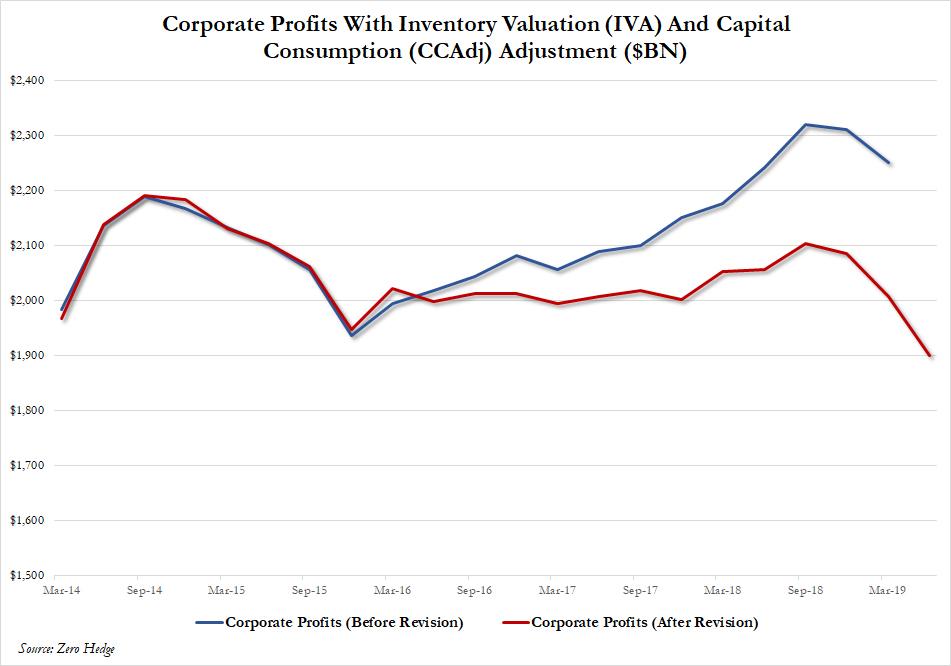

Ok, but there has to be some measure of corporate profitability that avoids all these non-GAAP adjustments and one-time addbacks. After all, profits are the lifeblood of a nation's GDP.

Conveniently, there is precisely such a data set tracking corporate profitability without the benefits of non-GAAP adjustments, and it is reported by the BEA in its purest form as Corporate profits with inventory valuation (IVA) and Capital Consumption (CCAdj) adjustments. Such operating profits, or profits from current production, are the purest form of corporate earnings since this series puts all firms on the same accounting framework - it avoids non-GAAP adjustments - and the profit numbers are not adjusted for the number of shares outstanding.

Yet even here something shocking took place this past July when a wholesale revision of the economic data revealed something shocking: according to the annual GDP revisions operating profits for 2017 were lowered by $93 billion, or 4.4%, and profits for 2018 were reduced by a whopping $188 billion of 8.3%.

(Click on image to enlarge)

Disclosure: Copyright ©2009-2019 ZeroHedge.com/ABC Media, LTD; All Rights Reserved. Zero Hedge is intended for Mature Audiences. Familiarize yourself with our legal and use policies every ...

more