Image Source: Skodonnell-iStockPhoto

Alternative Investments Up 10% in Five Years; Shift to Private Alternatives

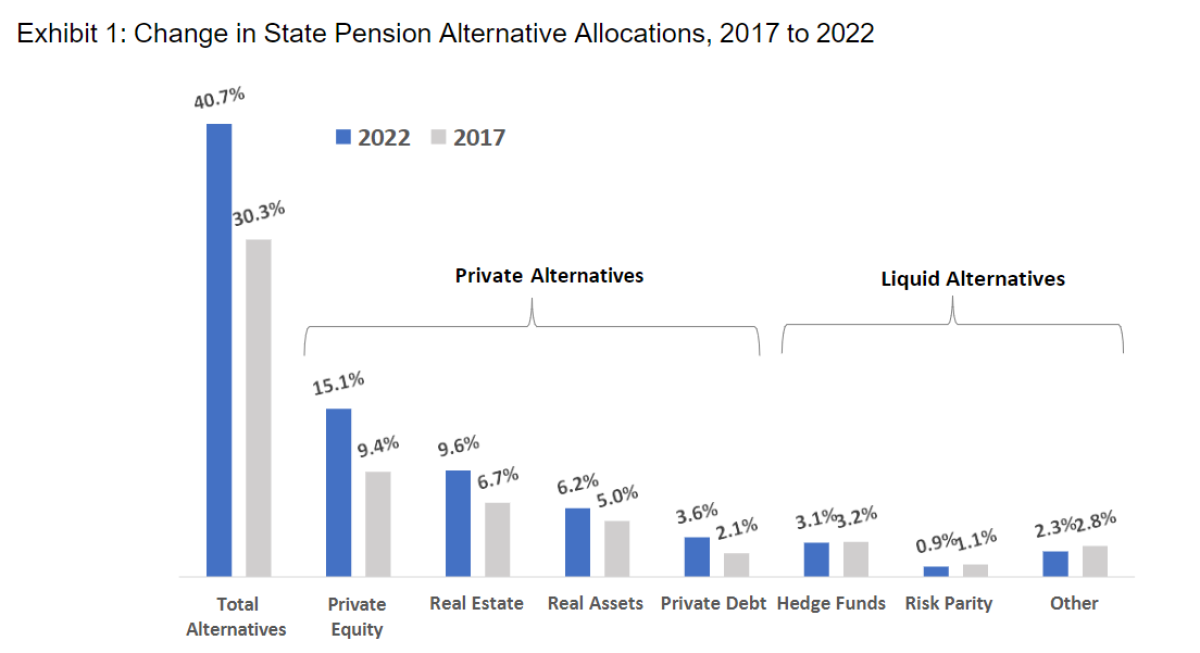

Allocations to alternatives have increased among all investor groups, but perhaps nowhere more than the $3 trillion state pension market, where alternatives increased a remarkable 10% in just the last five years, reaching 41% of total state pension assets as of June 30, 2022.

However, not all alternative asset classes benefited. Those alternative asset classes relying upon the private markets (private equity, real estate, real assets, and private debt) rose 11% over the most recent five-year period, while liquid alternatives (hedge funds, commodities, managed futures, risk parity, and other risk-mitigating strategies) fell -1%.

(Click on image to enlarge)

Liquid Alternatives Have Struggled to Meet Early Expectations

Institutional allocations to alternatives first jumped after the 2008 Financial Crisis as investors sought to de-risk their portfolios from large allocations to public equities. Liquid alternatives promising low equity correlations became fashionable, including hedge funds, commodities, risk parity, and other risk-mitigating strategies.

More than a few institutions created separate allocations to loosely defined Opportunity, Innovation, or Strategic investments with an emphasis on low equity correlation. Subsequent overall results from these liquid strategies have been mixed. Returns have been lower than expected while correlations have been higher than expected.

(Click on image to enlarge)

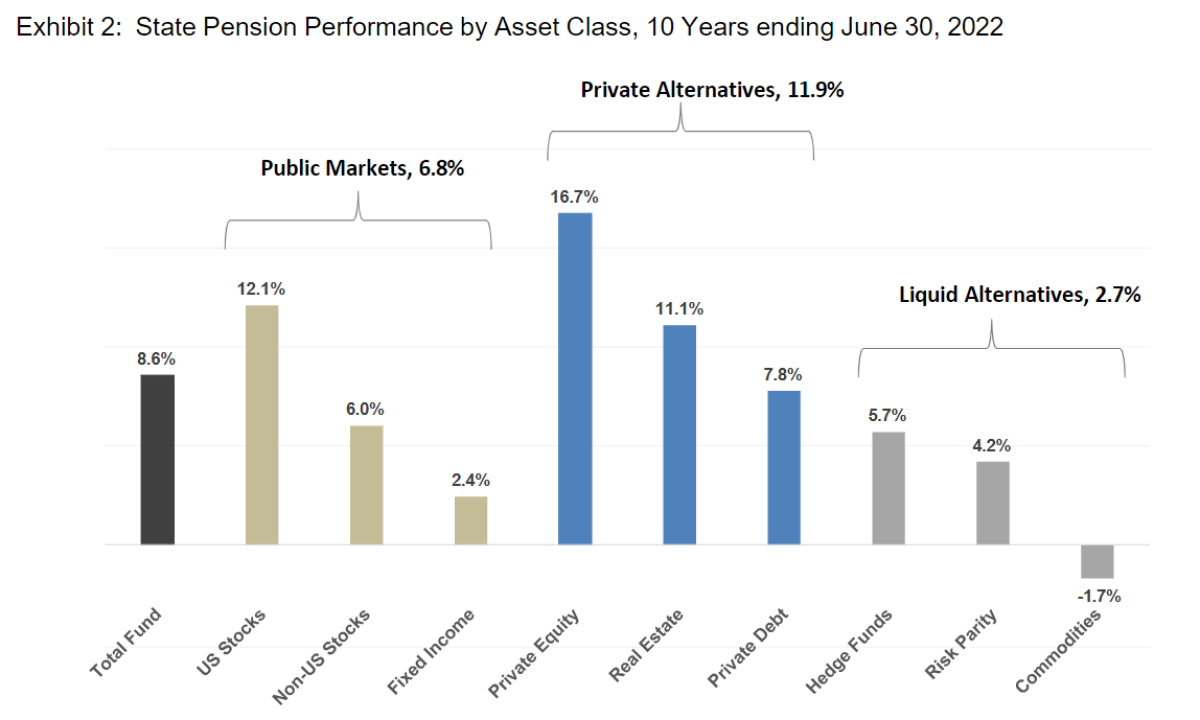

From a return perspective, the five-year institutional shift to alternative investments and private alternatives specifically may be largely explained by performance, as shown in Exhibit 2 for the 10-year period ending June 30, 2022. The 8.6% total state pension total return is broken down into public asset classes (averaging 6.8%), private alternatives (averaging 11.9%), and liquid alternatives (averaging 2.7%).

Even if liquid alternatives reduce short-term risk, the give up in long-term return may be too high a price for institutions. From a risk perspective, liquid alternatives had mixed results over the last 10 years. Risk parity fell almost 20% in 2022, commodities fell almost 30% in 2015, and hedge funds provided only modest protection when stocks fell in 2016 and 2022.

Private Alternatives Deliver an Illiquidity Premium

The reallocation to private alternatives is a likely reflection of the higher returns from private asset classes over public asset classes, as shown in Exhibit 2 where private alternatives returned an annualized 5.1% above public asset classes (11.9% minus 6.8%) over the 10-year period.

The emergence of private debt within institutional portfolios, while still at modest 3.6% allocation levels, has perhaps the greatest potential for growth because of its high and persistent yields and lack of interest rate risk.

About the Author

Steve Nesbitt is the Chief Executive Officer and Chief Investment Officer of Cliffwater, and is primarily responsible for the day-to-day management of Cliffwater Corporate Lending Fund (CCLFX) and the Cliffwater Enhanced Lending Fund (CELFX), an SEC registered credit interval fund focused on the US corporate middle market.

Steve is recognized for a broad range of investment research. His papers have appeared in the Financial Analysts Journal, The Journal of Portfolio Management, The Journal of Applied Corporate Finance, and The Journal of Alternative Investments. His private debt research led to the creation of the Cliffwater BDC Index, measuring historical BDC performance, and the Cliffwater Direct Lending Index, measuring historical performance for direct middle market loans.

Steve authored the book, Private Debt: Opportunities in Corporate Direct Lending, Wiley Finance (2019) which provides the analytical and empirical underpinnings of the private debt market.

More By This Author:

Structured Credit: Creditworthy Income Solutions For Investors Facing Rising Rates

Entering Leveraged Loans? Three Implementation Questions To Answer

Navigating A Higher-For-Longer Interest Rate Environment

Comments

Log in or sign up to join the conversation.