Jerome Powell’s upcoming speech at the Federal Reserve’s annual shindig is a chance to put things right. Last year in Jackson Hole, Wyoming, the central bank chair wrongly said that inflation was transitory to justify not responding to already-rising prices with higher interest rates. That mistake, though, turns out to be a happy one.

After Powell downplayed the risk of rising prices in August 2021, the pace of inflation quickened, and its scope spread. The consumer price index surged 9.1% year-over-year in June. Prominent financial folks now accuse Powell of being behind the curve, including former Treasury Secretary Larry Summers and JPMorgan boss Jamie Dimon. The Fed chair’s address on Friday is likely to compensate with a more hawkish tilt.

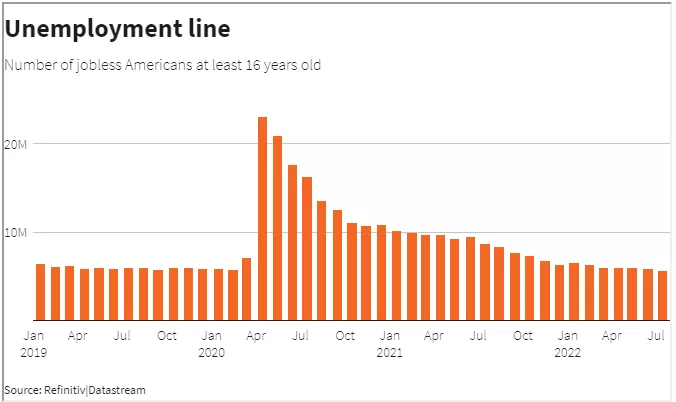

But even if the Fed could have acted a year ago, that doesn’t mean it should have. The economy wasn’t obviously sturdy enough to handle higher interest rates. The unemployment rate was 5.2% last August, with 8.4 million people still out of work. The jobless level for Black workers was a dismal 8.8%.

Rising borrowing costs would also have collided with a resurgence of Covid-19. The United States hit a peak of nearly 1.3 million new cases a day in January. California limited indoor gatherings while New York City required vaccines for indoor dining. Interest rate hikes then would have put even more strain on companies.

Besides, some of the fastest-rising costs wouldn’t have responded to higher rates anyway – such as the oil price, driven up by the war in Ukraine. The Bank of England began raising rates last December, three months before the Fed. Still, UK inflation in July was 10.1%, a 40-year high outpacing other G7 countries.

Now the U.S. economy is in a better spot. The Fed started raising rates in March when the jobless rate was near a 50-year low of 3.6%. Consumer spending has held up through two 75-basis point increases in a row. Employers are adding jobs at pace, and while GDP contracted in the first two quarters of 2022, that was largely due to supply chain issues. The consumer price index, still high, grew at a slower 8.5% in July.

Powell’s speech may reflect his hope, and belief for now, that higher rates won’t push the economy into a recession. But workers can meet that risk in a stronger state than they were a year ago – thanks to Powell’s earlier doozy of a mistake.

More By This Author:

TSX Earnings ScorecardQ2 2022 U.S. Retail Scorecard – Update

Recession Could Be U.S. Banks’ Guilty Pleasure

Comments

Log in or sign up to join the conversation.