Image Source: Pexels

As consequential as yesterday’s FOMC meeting was, particularly for equity markets, one can assert that Chairman Powell was upstaged by his predecessor, Treasury Secretary Yellen earlier in the day. But regardless of whether the present or prior Fed Chair was delivering the message, markets were enthusiastic about what they heard.

Secretary Yellen didn’t actually speak publicly, but the Treasury’s refunding announcement did the talking for her. Bond markets were already encouraged after Monday’s announcement that the Treasury’s borrowing needs would not be appreciably worse than feared, and then became enthusiastic when they learned that this quarter’s borrowing would be more front-end loaded than last quarter’s. As we noted yesterday, after the first leg down in yields:

Bond traders were thrilled that the quarterly refunding announcement was biased more heavily toward shorter-term notes than long-term bonds.That bias is helpful for two reasons: first, because the concerns about excess supply had been weighing more on the long end; and second, because the long end is more volatile than the short end, good news has a bigger impact.

Then it was the current Chair’s turn.The FOMC delivered the expected pause in rate hikes, but not a

“hawkish pause” – no change in rates and a largely unchanged policy statement.Yet there was one key addition to the second sentence in the second paragraph that got traders excited:

Tighter financial and credit conditions for households and businesses are likely to weigh on economic activity, hiring, and inflation. [emphasis mine]

You may be thinking, “yay, financial conditions are tighter?”But you need to think like a liquidity addict. An acknowledgment that financial conditions have tightened could mean that the Fed is more likely to ease to ameliorate them. Then he uttered this meeting’s magic word: “done.”Implying that the FOMC might be “done” kicked stocks and bonds into another gear. That enthusiasm is unabated today. Yesterday we reminded that:

Traders react while investors consider.

Investors considered yesterday’s developments overnight and clearly agreed with the traders.

We have noted traders’ propensity to fixate on keywords that can be interpreted in a friendly manner:

think about trader’s enthusiastic reactions to terms like “disinflation” in February, and “neutral” in August 2022

Much about today’s reaction reminds me of the events of February 2nd of this year. Here are two charts that illustrate the comparison:

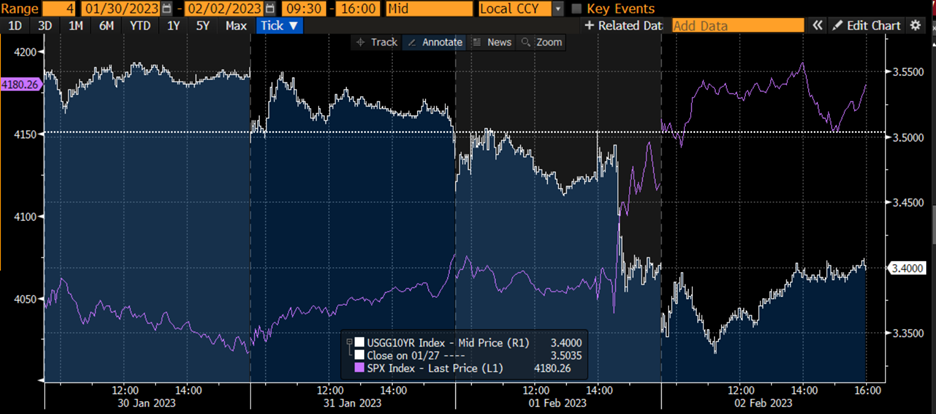

4-Day Chart, January 30th – February 2nd, 10-Year Bond Yields (white) vs. SPX (purple)

(Click on image to enlarge)

Source: Bloomberg

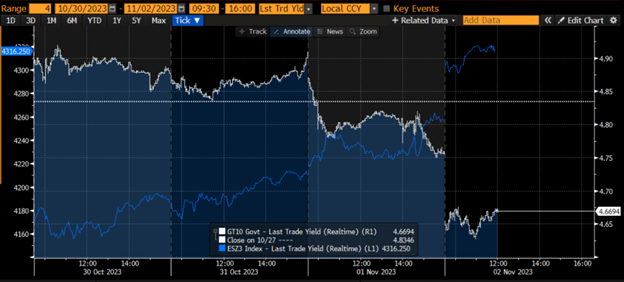

4-Day Chart, October 30th – November 2nd, 10-Year Bond Yields (white) vs. SPX (blue)

Source: Bloomberg

During the FOMC press conference that occurred on the afternoon of the 1st, we saw both bonds and stocks rally with each successive mention of “disinflation.”The S&P 500 (SPX) closed over 1% higher on February 1st and nearly 1.5% higher on the 2nd. As of now, this is awfully similar to what we have seen over the past day and a half.

That said, the bond market reaction now is even more powerful. On February 1st, the 10-year yield dropped 9 basis points, much less than yesterday, and only another 2.5bp on the 2nd. But it is important to keep in mind that the bond market was not yet focused on Treasury supply concerns (yields were around 3.5%, more than 1% below today’s levels), so in February yields were not supercharged by their own specific events. And today, yields also benefitted from a higher-than-expected 3Q Nonfarm Productivity Report of +4.7% (vs. 4.3% consensus), and an unexpected drop in 3Q Unit Labor Costs of -0.8% (vs +0.3% consensus). Higher productivity is always welcome news while shrinking wages benefit the overall inflationary picture (if not those whose wages fell).

Bullish traders should hope that the parallels between now and February end tomorrow. Then, as now, we had a monthly jobs report on the 3rd. That day Nonfarm Payrolls came in well above expectations. Equities gave back their Thursday gains and bonds gave back their entire post-FOMC move. Expectations for tomorrow morning’s report are for a gain of 180,000 payrolls and an Unemployment Rate unchanged at 3.8%. We’ll know tomorrow if history repeats.

5-Day Chart, January 30th – February 3rd, 10-Year Bond Yields (white) vs. SPX (purple)

(Click on image to enlarge)

Source: Bloomberg

Another key catalyst of course will be Apple’s (AAPL) earnings due after today’s close. Expectations are for $1.39/share on revenues of $89.3 billion. That revenue expectation is slightly above last year’s $90.1bn and last quarter’s $81.8bn.It would break a three-quarter streak of lower revenues, something one does not expect to see from the premier growth stock – one sporting a 29 P/E and a PEG ratio of 3.22. As we have seen with other mega-cap tech stocks ahead of their recent earnings, the options market is placing a maximum probability on slightly above-market options, as shown by the IBKR Probability Lab:

IBKR Probability Lab for Options Expiring Friday

(Click on image to enlarge)

Source: Interactive Brokers

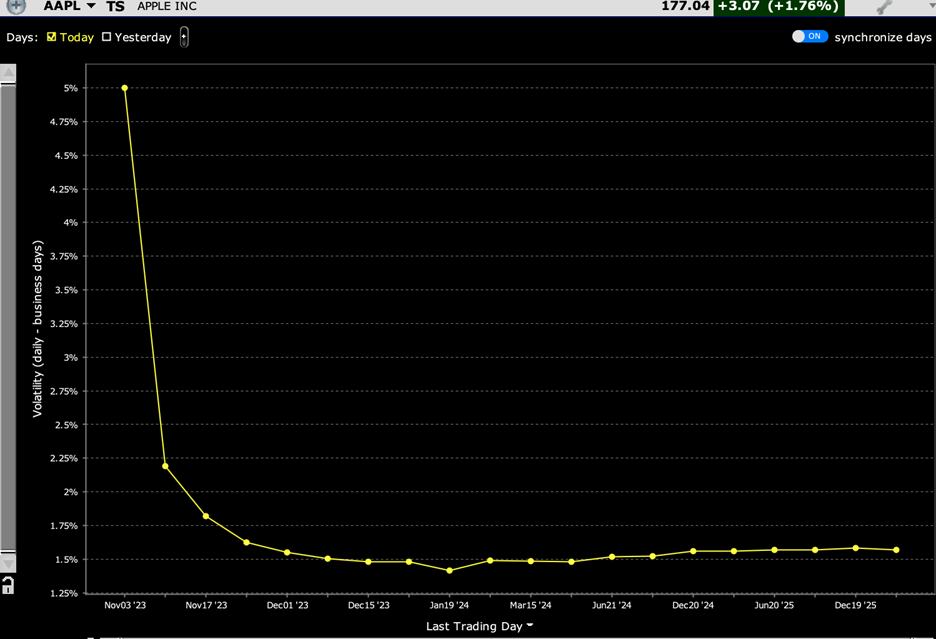

At-money options expiring tomorrow have a daily implied volatility of 5%, which is right in line with AAPL’s average 4.87% post-earnings move over the past four quarters (-4.8%, + 4.69%, +2.44%, +7.56%):

AAPL Implied Volatility Term Structure

(Click on image to enlarge)

Source: Interactive Brokers

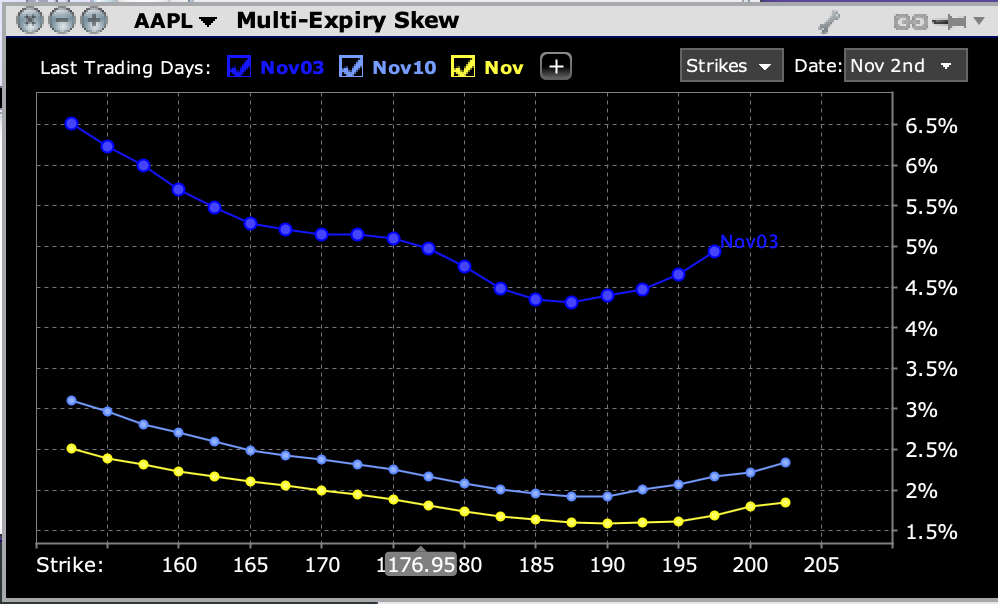

Skews are also relatively normal, with even this week’s options showing something resembling the classic “Elvis smile”:

AAPL Multi-Expiry Skew for Options Expiring Tomorrow (dark blue), Next Friday (light blue) and November 17th (yellow)

(Click on image to enlarge)

Source: Interactive Brokers

We have seen very powerful rallies over the past two days in stocks and especially bonds. We’ll have a much better idea tomorrow at this time whether these moves might represent key turning points or simply relief rallies.

More By This Author:

A Reminder: Other Stocks MatterHappy Monday So Far, With A Busy Week To Follow

Fed’s Inflation Gauge Rises At The Fastest Pace In Five Months

Comments

Log in or sign up to join the conversation.