On Friday, we reported that while everyone has been glued to the meltup in heavily-shorted stocks like GME (and the meltdown in the hedge funds who were heavily-short), there have been significant impacts under the covers of the rest of the financial markets that few have (for now) noticed.

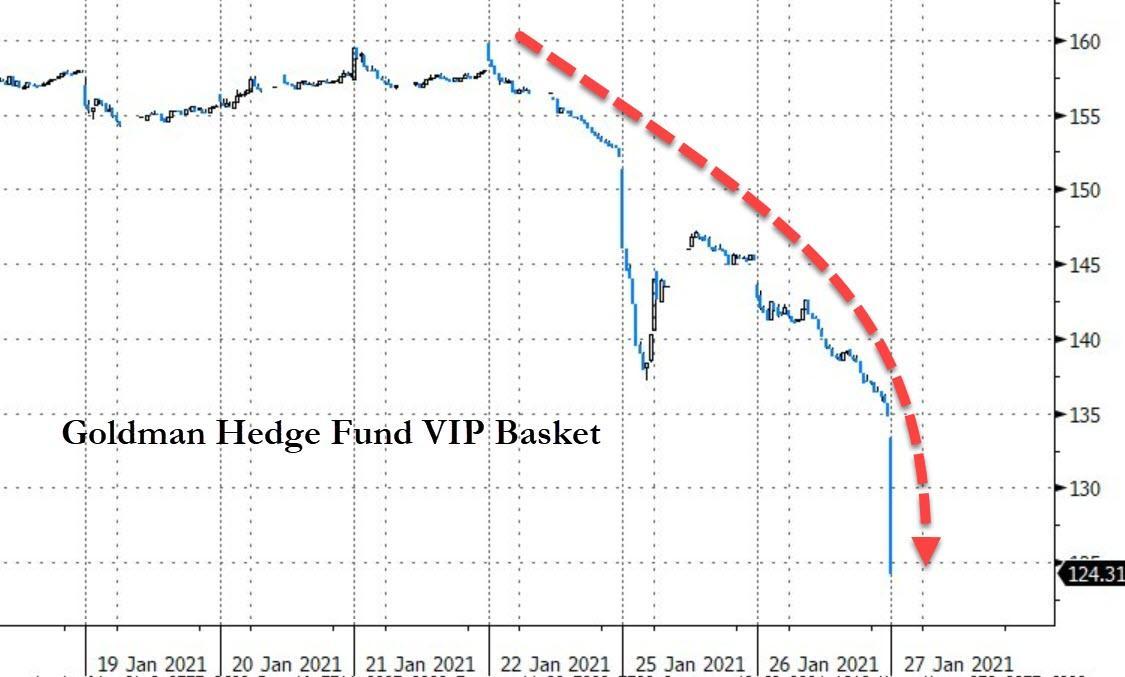

One place where the unintended consequences of the short squeeze hit hard was FANG stocks in particular. Another hit was seen in the most popular and liquid names held by "hedgies" (i.e., the Goldman Hedge Fund VIP basket), which have seen liquidations to meet margin calls, as well as due to VaR shocked-induced gross leverage drawdowns.

In other words, the higher the most shorted names rose, the more selling seen in the "most popular" longs, as illustrated below.

But it's not just pair trades that have gotten hammered - and incidentally, according to several desks, GME was the most popular short pair-trade offset to the ubiquitous AMZN.

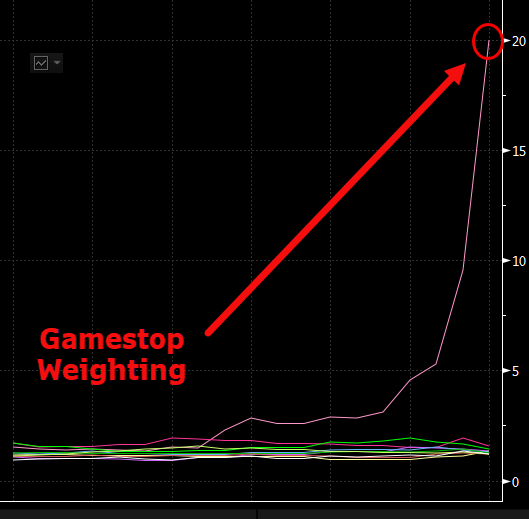

As we noted on Friday, the outsized influence from the booming video-game retailer has altered some ETF compositions, and is forcing what Citi analysts called "ad-hoc rebalances and strategy adjustments." In one of the most stunning developments, roughly $700 million in assets was pulled from the SPDR S&P Retail ETF (XRT) this week.

This is with a record $506 million pulled on Wednesday alone, draining total assets to just $164 million.

The outflows that came after GameStop’s surge swelled its weighting in XRT to an incredible 20%, which is unprecedented given that the fund tracks an equal-weighted index and that the video game retailer’s weighting should be closer to 1%, according to Bloomberg's James Seyffart.

While we didn't know what specifically caused this record plunge in XRT assets, we speculated that "one possibility is that because XRT redemptions are delivered in-kind -- meaning that its shares are exchanged for the underlying stocks in the fund -- investors are ditching the ETF to get their hands on hard-to-borrow GameStop shares."

As it turns out, that's precisely what happened. As Bloomberg's Seyffart and Balchunas explain, "the $506 million outflow on Jan. 27 cut XRT's assets to less than $240 million and offered further evidence of the stability of the ETF structure. Despite the plunge in assets, XRT's price was unaffected, closing at a 6-bp discount... The Jan. 27 outflow amounted to 5.55 million XRT shares, lowering the total to 2.6 million."

A huge move that barely impacted the price; that's good -- it means that the market is still liquid enough for historic asset reallocations in ETFs. But that's not the punchline:

"The in-kind redemption was likely an attempt by investors to get their hands on scarce GameStop shares. Based on XRT's weightings, those who took delivery of the underlying holdings received about 292,000 GameStop shares, alongside 94 other stocks."

Unprecedented? Well, yes. Because as Bloomberg itself concludes, "by allowing investors to redeem GameStop and other shares from its own holdings, XRT effectively acted as a dealer, akin to the role we see many liquid fixed-income ETFs playing in the bond market."

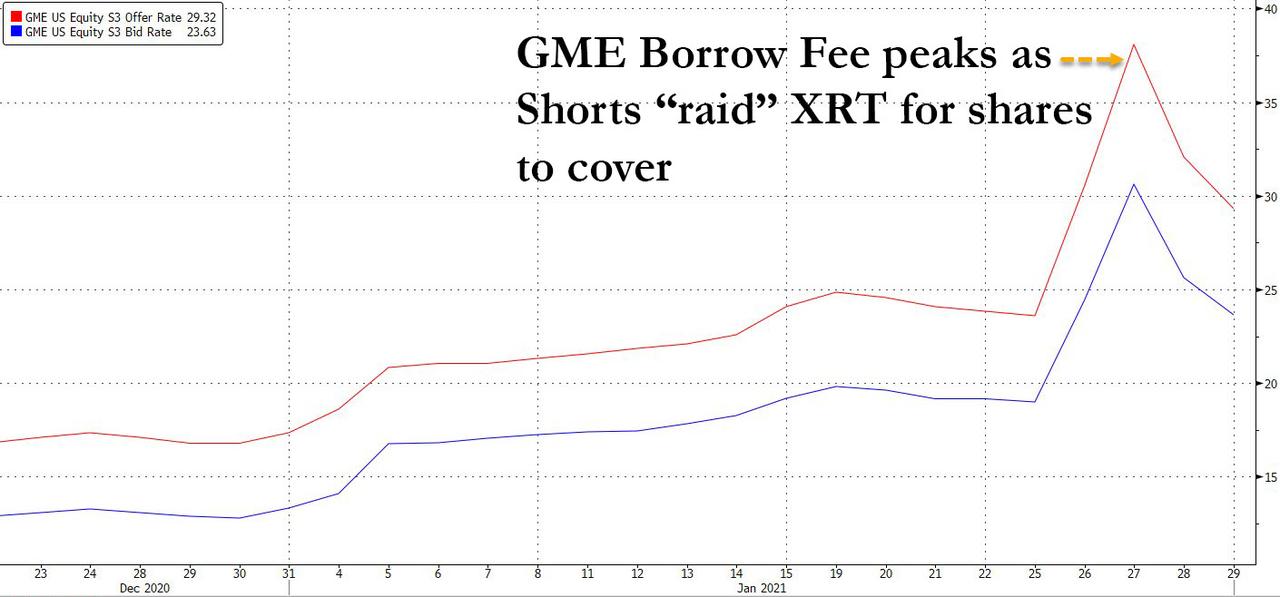

Why is this important? Because as a look at GME borrow rates (courtesy of S3 Blacklight) shows, Jan. 27 is precisely the day when the carry cost to hold GME shorts peaked (and at some dealers it soared as high as a brutal 200%, according to S3 Partners).

In the Thursday overnight session, the price of GME also peaked, and has been drifting lower since.

Here is the bottom line: one (or more funds) facing a terminal margin call were so desperate to close out their GME short in a market where the cost to borrow the stock had exploded as high as 200% (a death sentence for any hedge fund who plans to keep the GME short on for a long period of time), that they stripped XRT (which as Bloomberg notes "acted as a dealer") of 292 thousand shares of GME to quickly plug the shortfall and emerge alive.

As a result of this furious scramble, not only did the cost to borrow GME slide, but so did the stock price.

So what does that mean? Is the panic squeeze over now that the cost to borrow GME has dropped? Well, maybe not, and here's why: with XRT effectively raided out of a paltry 300 thousand shares, there are no more hiding places for GME stock to be raided. In other words, any shorts left are on their own.

Meanwhile, as S3 Partners' Ihor Dusaniwsky wrote on Friday, some 113.3% of the GME float is still short (synthetically, including re-hypothecated shorts). What's worse, while the cost to borrow GME stock has dropped, it still remains around 30%, which means that no hedge fund can remain short the stock indefinitely without suffering massive losses, and yet still more than all of the float is short.

Whether this means the GME squeeze will resume tomorrow, or whether the "help" of Robinhood's effective shutdown and Citadel's friends in high places sees the short raid finally end on Monday, we leave it up to readers to decide.

Comments

Log in or sign up to join the conversation.