The Current Economic Situation In The Euro Area

The euro area, which will hereafter be referred to as the Eurozone, remains in a state of post-recession recovery. Following the financial crisis that began in late-2008 in the United States and the ensuing global fallout, the Eurozone had an economic crisis of its own that is known as the sovereign debt crisis. Precipitated by the vast debt a number of Eurozone constituent countries had accumulated with respect to their GDP, the sovereign debt crisis involved risk of default in several countries and a series of bailouts to some. Economies shrank as GDPs declined, unemployment rose, and deflation occurred. To combat this crisis, in addition to the aforementioned bailouts, the European Central Bank, which will henceforth be called the ECB, drastically lowered interest rates and engaged in the unconventional practice of buying securities as one way to accomplish this. Through its program known as Outright Monetary Transactions (OMT), the ECB offered to purchase government debt (from private banks) of member states that request assistance. Due to the associated conditionality, however, it was never implemented across the entire Eurozone. Also created by the ECB was long-term refinancing operations (LTROs) program in which long-term, low-interest loans were made to Eurozone banks and used government bonds and other securities as collateral. However, the Eurozone is a region of great contrast, which has made universal solutions difficult to develop and implement; while a number of countries, perhaps most notably Greece, remain in terrible economic condition, others such as Germany have bounced back strongly. Today, over two years since ECB President Mario Draghi's famous statement that the bank "is ready to do whatever it takes to preserve the Euro," it remains to be seen what further steps the Eurozone will take towards recovery.

The sovereign debt crisis, as its name implies, started due to high government debts and deficits. This is still a major problem in the Eurozone. The overall public debt/GDP ratio in the Eurozone is above 90%, which is very high. More troubling than that, however, is some of the individual Eurozone countries. Greece, for instance, had reached the point where debt payments were not met and bailouts were required.

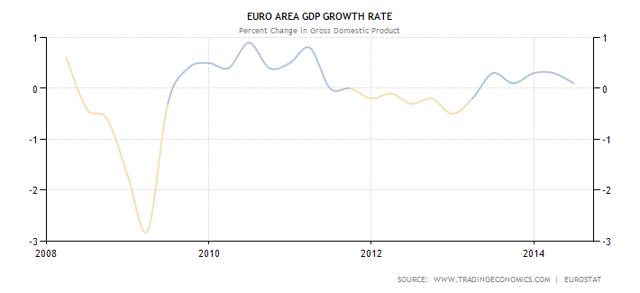

GDP growth, the most complete measure of economic growth and development, in the Eurozone has fluctuated significantly over the past five years. Currently, it is at about 0.1% QOQ in Q2 2014. This is a virtually insignificant amount especially considering the presence of some inflation. Sustained GDP growth at or around 0% causes risk of recession and little room for unemployment to improve. Even more alarming is the long-term trend since the financial crisis, which is visible on the chart below: growth has consistently stayed below 1% and has slipped into the negatives for some stretches, signaling a potential "double-dip" or "triple-dip" recession and general economic stagnation.

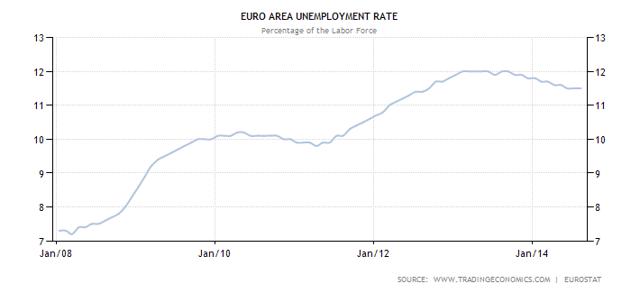

The Eurozone's unemployment rate, indicative of the strength of its industry and workforce (or lack thereof), has generally only increased since 2008. It has stabilized at approximately 11.5%, far above its number five years ago when it was at near 7%. The constant upward tendency of unemployment since the crisis is visible on the graph below.

Additionally, there is a wide disparity between Eurozone countries for this indicator. For example, Austria's unemployment rate is around 5% whereas that of Spain is north of 25%.

Unemployment and GDP are inversely correlated, so the extreme unemployment rate and lackluster GDP growth rate are causes of each other. A low GDP growth rate means there is less capacity for hiring, which increases unemployment. High unemployment, in turn, causes less consumer spending and economic activity in general, which leads to even lower GDP growth. This is a vicious cycle that the Eurozone is currently trapped in.

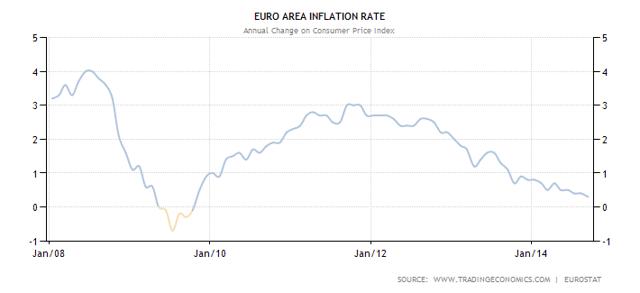

Inflation, which reflects the increase in price of goods and services, in the Eurozone has been below its ideal rate for several years. At the onset of the financial crisis, inflation dropped until it fell below 0%, which is known as deflation. The ECB has stated that its goal is "just under 2%," which has not been met for the past two years. It had earlier rebounded, but it has further fallen to 0.3%, prompting fears of deflation occurring once more and another potential recession. This trend is visible on the graph immediately below.

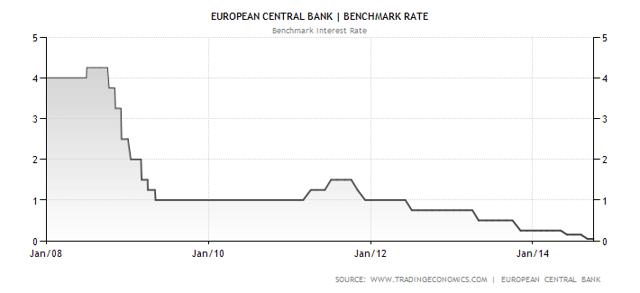

The ECB has attempted to increase inflation through the aforementioned programs that it implemented in the wake of the financial crisis. The lowering of the benchmark interest rate is the primary tool the ECB has employed recently. The result is that the rate, which sets the benchmark for all interest rates in the Eurozone, is currently, as near as makes no difference, 0%. This is shown by the chart below.

Click to enlargeThe low rates, OMT, LTROs, and the other loose forms of monetary policy pursued by Mr. Draghi have all had the goal of injecting liquidity into the banking and financial system of the Eurozone. By buying assets from banks, the ECB is capitalizing and deleveraging banks. This is done in the hopes that the credit market will expand because banks, with their newfound cash reserves, will lend more to consumers. Due to the supply of cash increasing relative to demand, interest rates would be low and borrowing activity from both consumers and businesses would increase. An increase in business activity would help grow the economy and lower unemployment. Also, low interest rates would also mean low bond yields. This encourages investors to withdraw money from bonds and instead put it in stocks and other business-related securities or investments, which gives more capital to business and, again, improves both unemployment and GDP growth. This has already worked, since the stock markets of the Eurozone's constituent countries have all risen dramatically in a bull market over the past few years.

Going forward, the ECB plans to continue its loose monetary policy and also plans to implement a new asset purchase plan. As of last week, the ECB has begun buying covered bonds, a security that uses other bonds and securities as collateral, on the open market. Later this year, it plans to expand this into a variety of asset-backed securities. This is a non-sterilized program and increases both the ECB's balance sheet and the M1 supply, which makes it an inflationary agent. It resembles a form of quantitative easing, which has been implemented in the United States and United Kingdom, among other places. This is a move that stems from Mr. Draghi's previous declaration that he was willing to use unconventional monetary policy to fix the Eurozone's economic situation.

In conclusion, the Eurozone is still in the process of recovering from the global financial crisis and the sovereign debt crisis. It is unclear whether another recession is imminent or not; however, it is clear that stagnation is occurring and growth is not where it should be. The unconventional monetary policy that is being pursued by the ECB aims to solve these problems, and their long-term effects are still not known. Overall, the current economic situation in the Eurozone is mixed and it remains to be seen what the future holds.

Disclosure: None