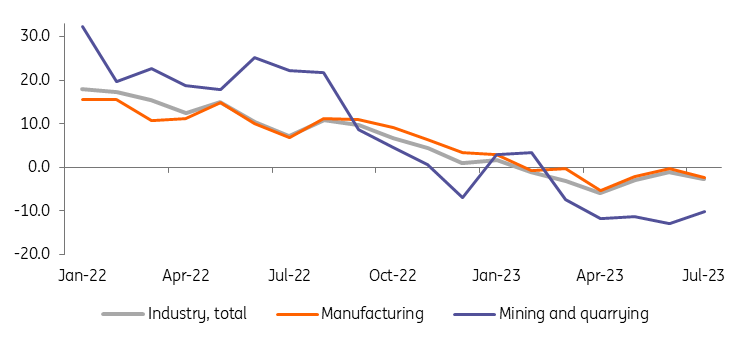

July industrial production fell by 2.7% year-on-year, well below the consensus forecast of 0.6%.

There were yearly declines in all four major commodity groups, double-digit drops in mining and quarrying of 10.2%, and in manufacturing by 2.4%. Producer price deflation was deeper than expected, with July PPI falling 1.7% YoY against a consensus of -1.2%.

Poland's industry saw a surprisingly weak start to the third quarter, although this coincided with dismal industrial PMI readings in Poland (43.5pts in July) and Germany (below 40pts in July).

Year-on-year declines in industrial production in July were recorded in 24 of 34 industrial production divisions, the deepest in coal and lignite mining (by 27.7%), chemical products (9.6%), wood products (15.5%), paper (11.5%), metals (10.4%), and other non-metallic products (8.8%). The 10 divisions that saw an increase in production were led by machinery and equipment repair (up 20.7%), motor vehicles (15.0%), other transport equipment (8.1%) and machinery and equipment (4.9%). Production’s positive growth was driven by pro-export sectors.

The deep fall in PPI producer prices was largely due to the statistical base effect and clearly lower energy prices than a year ago, but also reflected weakness in demand. A similar picture emerged from Germany's July PPI reading. On a monthly basis, Polish manufacturing prices have been falling since November, and we expect PPI deflation to continue at least until the end of the year, which should facilitate further CPI disinflation.

Available leading indicators (PMIs, new orders data) do not suggest a rapid recovery in manufacturing, although the most acute phase of inventory reduction by Polish companies seems to have passed. This week the preliminary August PMIs for the eurozone and Germany will be published; our forecasts do not assume a significant improvement compared to July. The economy of Poland’s largest trading partner is balancing between stagnation and recession.

We expect that industrial production in Poland will remain low in the third quarter and experience a more visible rebound in the fourth quarter.

Poland's industrial production, YoY changes, in %

ING based on CSO data.

More By This Author:

The Commodities Feed: LNG Strike Action LoomsFX Daily: Treasury Slide Keeps Markets Nervous

Asia Week Ahead: Key Central Bank Meetings And Inflation Reports

Comments

Log in or sign up to join the conversation.