Industrial production rose but missed the market consensus while retail sales unexpectedly declined. Weaker-than-expected monthly data suggests any rebound in 4Q GDP should be modest. But the upturn in the semiconductor cycle and solid demand in vehicles should support growth.

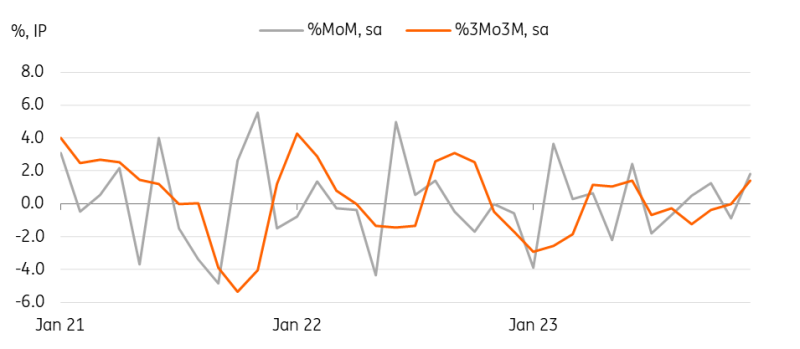

Industrial production rebounded in December, more than offsetting the November decline

December IP rose 1.8% month-on-month (seasonally adjusted), a bit weaker than expected (market consensus 2.5%) but the monthly gains were broadly based. Notably, chip-making equipment grew 5.4% for a second month and transportation equipment – vehicles (1.2%) and aircraft parts (11.3%) – rebounded. Also, as shipments grew faster (2.5%) than production, inventories were down -1.2%.

Along with today’s robust Korean IP outcome, we firmly believe that global demand for IT and vehicles is solid. We believe the negative impact of the recent earthquake should begin to appear from January's monthly data, but it should be limited and temporary, thus the underlying trend of a solid recovery in IT and vehicles will likely continue in the current quarter.

Japan IP improved compared to 3Q23

CEIC

Unexpectedly weak retail sales are a concern for near-term growth

Retail sales declined -2.9% MoM sa in December (vs 0.2% market consensus), more than offsetting the previous month's gain of 1.1%. The declines were widespread across all sectors but were most notably down in apparel (-10.7%), vehicles (-5.0%), and household machines (-8.8%). It seems like higher inflation is biting into household consumption.

GDP and BoJ outlook

The gains in manufacturing output suggest 4Q23 GDP rebounded (0.3% QoQ sa) from a mild contraction in 3Q23 (-0.7%), with the risk skewed to the upside. We think that weak retail sales should be the main drag on overall growth and that households’ cautious consumption behavior could further discourage the Bank of Japan from raising its policy rates. The economic outlook is still positive as solid corporate earnings will likely boost investment and offer solid wage gains. But, if the negative output continues, then demand-driven inflation is hardly achieved. So, it should preclude the Bank of Japan from making major policy changes in March.

More By This Author:

FX Daily: US Data Does The TalkingFrench Inflation Eases More Than Expected

China: January PMI Edged Up But Remained In Contraction

Comments

Log in or sign up to join the conversation.