How To Effectively Replace Mutual Funds With ETFs In Your Portfolio

According to the latest ICI Fact Book, assets in the US-registered mutual funds totaled $15.8 trillion at the end of 2014, whilst exchange traded funds (ETFs) had just short of $2 trillion AUM. I find this difference odd given that ETFs have been around for over 20 years and their advantages over mutual funds are well documented. Even more surprising is the fact that roughly 70% of assets are invested in actively managed funds, which underperform passive investments by default as Noble Prize winner William F. Sharpe has elegantly proven. It appears that people are willing to pay extra for the mere chance to get a higher return – a bit like a lottery ticket. But do mutual funds present investors with a real opportunity to win?

For simplicity purposes, in this article I focus on the two largest actively managed US mutual funds: American Funds Growth Fund of America (AGTHX) with $149 billion in AUM and an annual expense ratio of 0.66%, and Fidelity Contrafund (FCNTX), which manages $113 billion and charges 0.64%.

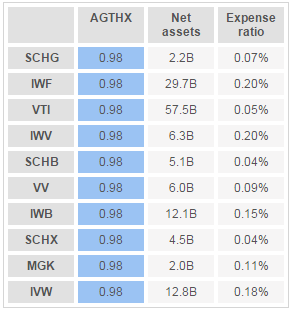

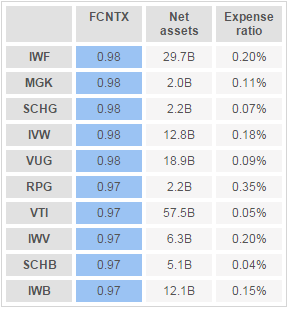

The first part of the test that I run is a check which ETFs mimic each of the funds most closely. For this purpose I tap into the new tool on InvestSpy that ranks largest ETFs by their correlation coefficient to the selected fund. Analyzing data for the last 5 years, I get the following results:

It turns out that there are plenty of ETFs that move hand in hand with each of the two mutual funds. From the portfolio perspective, two securities that have a correlation coefficient in high 90s are virtually identical and to a certain extent can be treated as substitutes to each other.

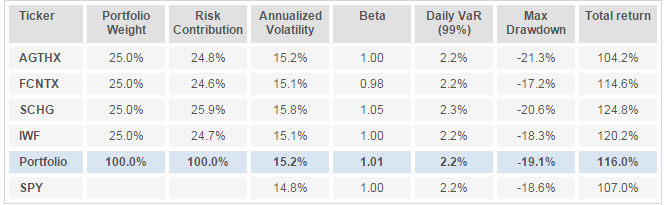

The second part of the test is to check whether the actual performance and risk metrics of these potential substitutes matched those of AGTHX and FCNTX. For this purpose I use the two ETFs that appear in the top 3 of each table: Schwab US Large-Cap Growth ETF (SCHG) and iShares Russell 1000 Growth ETF (IWF). Utilizing the portfolio calculator on InvestSpy for the same 5 year data period yields the following results:

The table above reveals that risk parameters of SCHG and IWF are not much different from AGTHX and FCNTX. IWF looks like an ideal candidate to replace either of these mutual funds in a portfolio straightaway, whilst one may choose to invest a slightly lower amount into SCHG, say 95% of the original investment, to maintain the same risk profile. In terms of returns both ETFs outperformed the mutual funds, although it is important to note that AGTHX was by far a worse performer than FCNTX.

So what would I do if I ended up with a mutual fund like AGTHX or FCNTX in my portfolio? Well, without further ado I would replace them with a low cost ETF that demonstrates similar risk and return characteristics, pocketing in the 0.5% difference in expense ratios. I can then use the savings to buy lottery tickets in a local corner shop.

Makes sense, thanks. And good luck with those lotto tickets!