This morning the Institute for Supply Management published its monthly Manufacturing Report for October. The latest headline Purchasing Managers Index (PMI) was 50.2, down 0.7 from the previous month and in expansion territory. Today's headline number was below the Investing.com forecast of 50.0.

Here is an excerpt from the report:

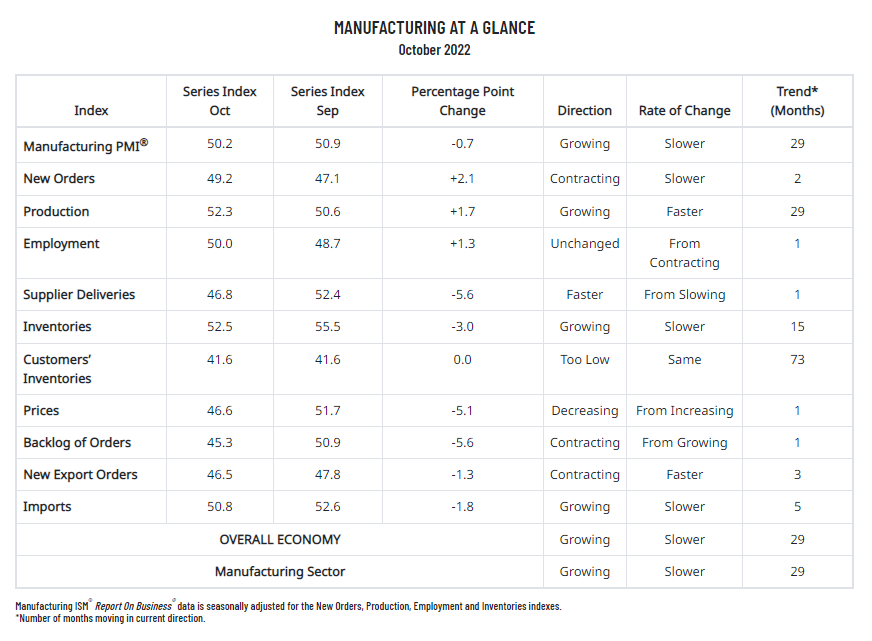

Fiore continues, “The U.S. manufacturing sector continues to expand, but at the lowest rate since the coronavirus pandemic recovery began. With panelists reporting softening new order rates over the previous five months, the October index reading reflects companies’ preparing for potential future lower demand. In the meantime, demand eased, with the (1) New Orders Index remaining in contraction territory, (2) New Export Orders Index below 50 percent for a third consecutive month and at a faster rate of contraction, (3) Customers’ Inventories Index remaining at a low level, with the same reading as in September and (4) Backlog of Orders Index slipping into contraction. Output/Consumption (measured by the Production and Employment indexes) improved month over month, with a combined positive 3-percentage point impact on the Manufacturing PMI® calculation. The Employment Index shifted from contraction to a reading of 50 percent (unchanged), and the Production Index increased by 1.7 percentage points, staying in modest growth territory. Business Survey Committee panelists’ companies are continuing to manage head counts through hiring freezes and attrition to lower levels, with medium- and long-term demand still uncertain. Inputs — defined as supplier deliveries, inventories, prices and imports — mostly accommodated growth. The Supplier Deliveries Index indicated faster deliveries and the Inventories Index dropped 3 percentage points as panelists’ companies continued to manage the total supply chain inventory. The Prices Index decreased for a seventh straight month and fell into contraction territory, which should encourage buyers. See report

Here is the table of PMI components.

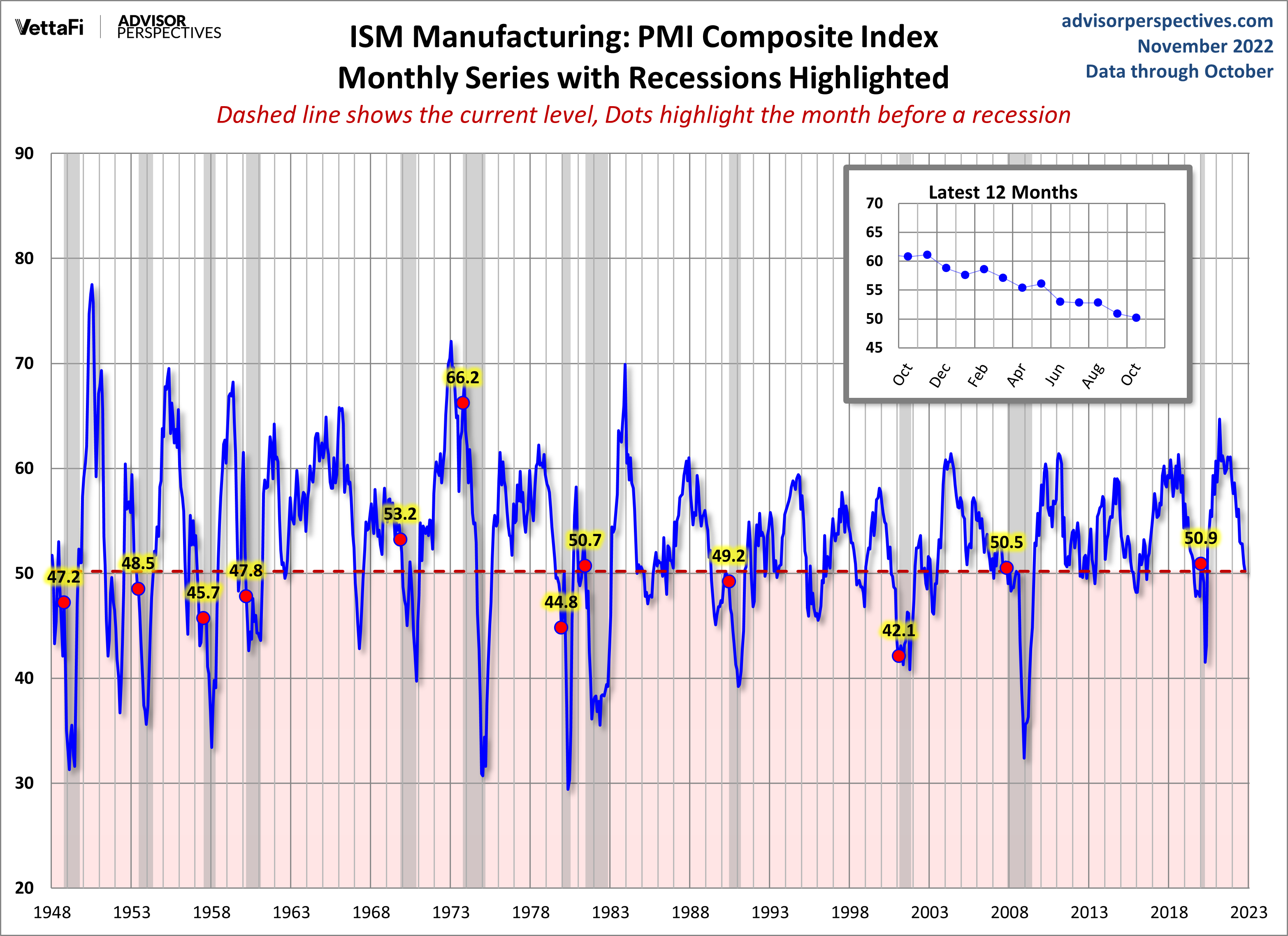

The chart below shows the Manufacturing Composite series, which stretches back to 1948. The eleven recessions during this time frame are indicated along with the index value the month before the recession starts.

For a diffusion index, the latest reading is 50.2 and indicates expansion. What sort of correlation does that have with the months before the start of recessions? Check out the red dots in the chart above.

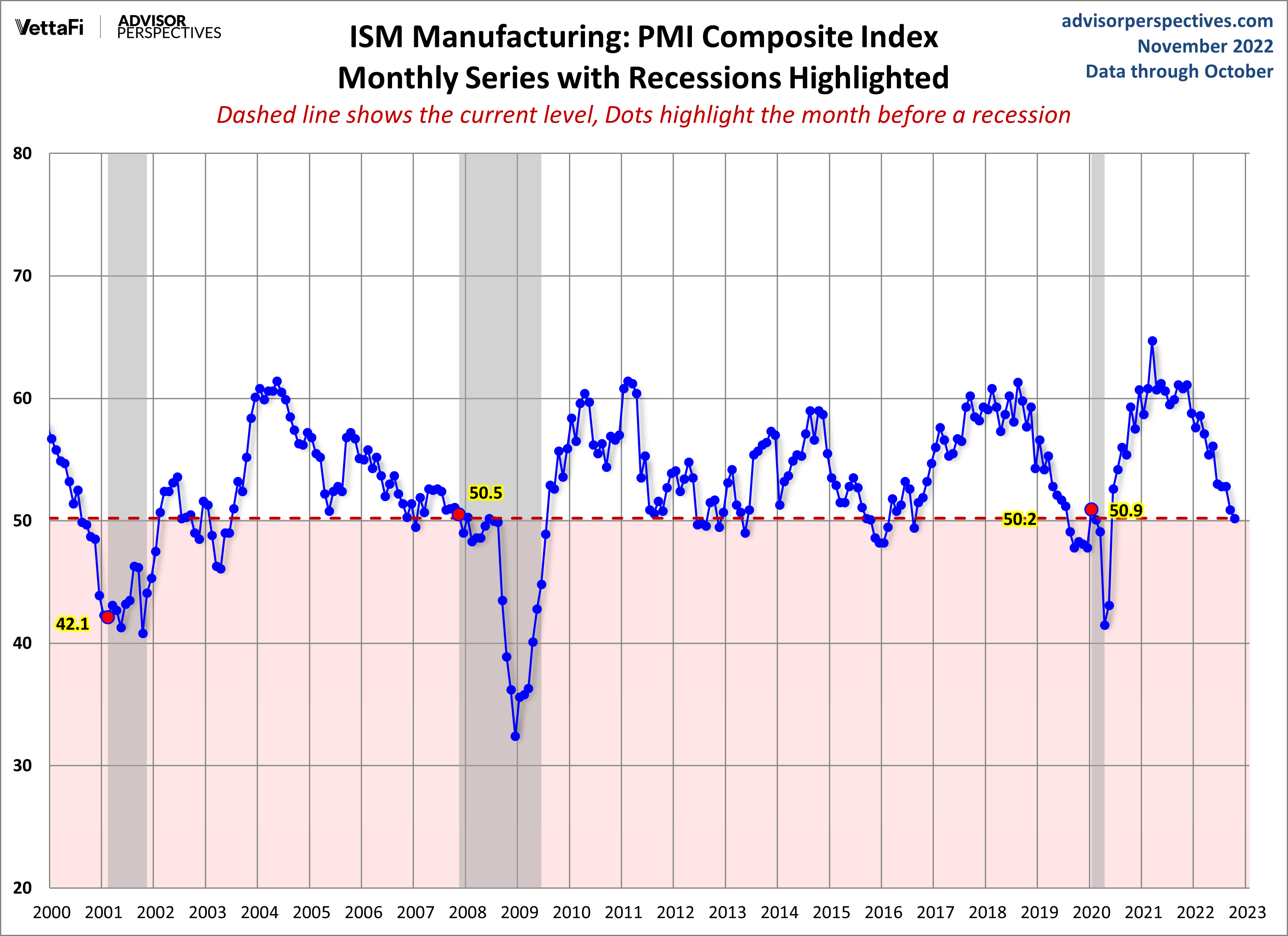

Here is a closer look at the series beginning at the turn of the century.

Note: This commentary used the FRED USRECP series (Peak through the Period preceding the Trough) to highlight the recessions in the charts above. For example, the NBER dates the last cycle peak as December 2007, the trough as June 2009, and the duration as 18 months. The USRECP series thus flags December 2007 as the start of the recession and May 2009 as the last month of the recession, giving us an 18-month duration. The dot for the last recession in the charts above is thus for November 2007. The "Peak through the Period preceding the Trough" series is the one FRED uses in its monthly charts, as illustrated here.

More By This Author:

World Markets Update - Monday, Oct. 31Dallas Fed Manufacturing Growth Outlook Worsens In October

Chicago PMI Dipped In October

Comments

Log in or sign up to join the conversation.