9, June

When investors choose to buy gold bullion or invest in silver bars they are doing so because they wish to reduce their portfolio risk. One of those risks is counterparty risk.

If you own shares, then you are exposed to the risk of company management making poor decisions, if you invest in property you are exposed to the risk of a property market crash. If you invest in art then you are exposed to the risk of the artist tarnishing their name with bad behaviour and if you invest in NFTs well…just pick any risk.

Today’s blog is all about counterparty risk. And not just the potential for counterparty risk, it’s about the counterparty screwing up big time and costing investors millions and millions of dollars.

We need to say it again. Exchanges, especially futures exchanges are no friend to metals investors.

Gold: The Only Safe Haven Asset You Need

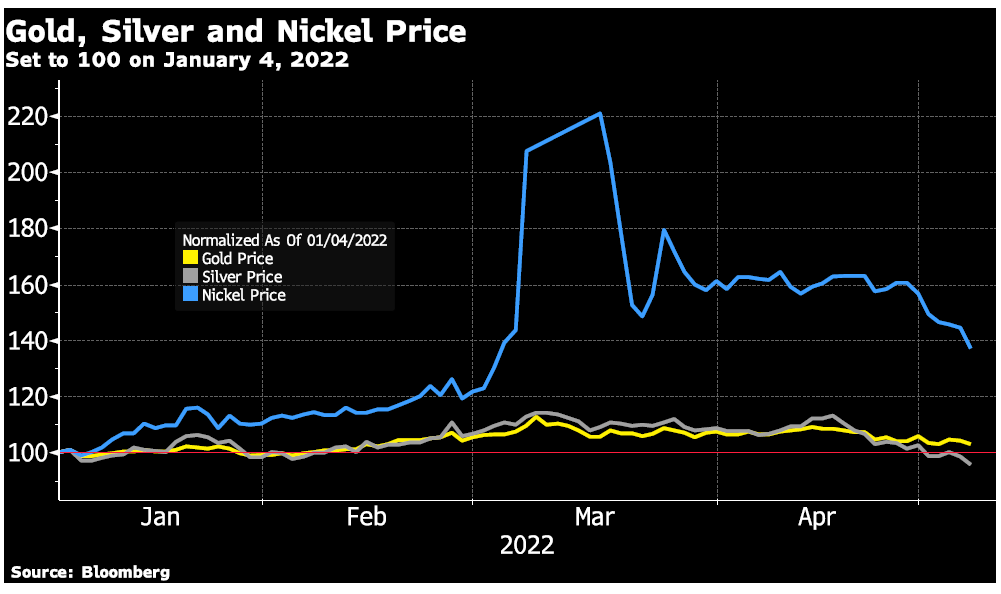

In our March post titled “If You Don’t Hold It, Then You Don’t Own It” , we wrote about how the LME had cancelled trades to the benefit of a Chinese national who was short nickel contracts.

As it happens the LME is owned by Hong Kong and Chinese interests.

It is timely this week to discuss the latest fallout from those cancelled trades. Throughout this discussion the main takeaway will remain worth repeating; physical metals investors have much less counterparty risk than other metals investors.

Said another way – if you [or a custodian] don’t hold it, then strictly speaking you don’t own it.

You don’t own it if someone else has the ability to choose to not honour a contract. It is at moments of crisis when honouring contracts matters most because prices are swinging wildly.

Gold, Silver and Nickel Price Chart

Another important point to remember: what happens in the nickel market this year could happen in the silver market or the gold market next year.

These busted trades that hurt hedge funds in 2022 could have implications for ETFs in the future.

So, what happened this week? The lawsuits have started. Giant pools of capital run by hedge funds were on the opposite side of the nickel contracts LME cancelled that served to benefit the Chinese national.

Gold To New All-time-high When Fed QT Fails Watch Don Durrett Only on GoldCore TV

The hedge funds lost millions of dollars when their paper trading profits in nickel futures were eliminated by retroactive decisions taken by LME staff while Chinese nickel billionaire Xiang Guangda was short, and his losses were retroactively cleared.

Elliott Management is a giant American hedge fund headed by a multi-billionaire named Paul Singer.

Elliott Management is so big it actually owns the AC Milan football club. And Elliott has a track record of being able to protect its interests via courts and foreclosing on loans it makes.

One notable case was that Elliott Management fought a decade long court battle with the government of Argentina over the default of Argentina’s sovereign bonds, forcing the government to the negotiation table.

LME in Crisis

Elliott is now suing the LME futures exchange for US$456,000,000!

According to Reuters Elliott claims that the LME acted

“unreasonably and irrationally in particular by taking into account irrelevant factors, including its own financial position”.

A market-making firm called Jane Street has also sued the LME for US$15,300,000. A Financial Times article remarking on Jane’s lawsuit contained something which exchange traded metals fund investors, including those for gold and silver, should read very carefully.

“If your job . . . is to essentially ensure an orderly smooth functioning of the global financial markets, they can’t do that if the counterparties, aka an exchange, don’t align with the contracts that they enter into,” the person said.

They added that uncertainty created by actions such as the LME’s increased the risks of providing liquidity for exchange traded fund markets, one of the group’s biggest businesses” (bolding added).

This quote shows the direct implications for ETFs. Jane Street is saying that metals ETFs need the LME to be impartial, but since the LME is not impartial, Jane Street is suing the LME to recover losses.

This means that any gold or silver ETF might be prevented from buying more gold or silver by the LME during a panic to own the metal – exactly the moment when demand for gold and silver ownership will increase.

Clearly, a better strategy would be to own physical metals rather than investing in ETFs.

Everyone expects stock exchanges and futures exchanges to operate like a public utility, but they don’t operate like that at all.

Certainly not in times of crisis. Perhaps LME, similar to the WHO, [World Health Organization] has lost its way by centering too much on the needs of a specific constituency instead of the comprehensive global community.

Giant investors like Jane Street and Elliott Management have deep enough pockets to chase justice from the LME via courts for many years to come.

Gold is Not an Investment Asset – Here’s Why Watch Ned Naylor-Leyland Only on GoldCore TV

A capacity that very few individual investors or families have as an option. We will be watching the court case as it winds through the legal system for recognition [hopefully] from a Judge that exchanges should be unable to escalate counterparty risk whenever it chooses.

Perhaps the LME’s legal teams plan to suggest that Elliott Management knew and accepted the implicit risks of trade cancellation and counterparty risk inherent to trading on a futures exchange.

If LME takes that stance, then their argument would prove ours: if you don’t have the physical then you don’t own it!

Comments

Log in or sign up to join the conversation.