It was good while it lasted, but the party is well and truly ending.

Just three weeks ago, Goldman Sachs - which last year was the first bank to unveil materially above consensus GDP projections - cut its 2021 second half consumption growth forecast, resulting in 1% downgrade to its GDP growth forecasts for Q3 and Q4 to +8.5% and +5.0%, respectively, "as it is becoming apparent that the service sector recovery in the US is unlikely to be as robust" as the bank had expected. Which is odd considering the trillions in monetary and fiscal stimulus that have entered into the economy. One wonder how many more trillions would be needed for Goldman to be happy.

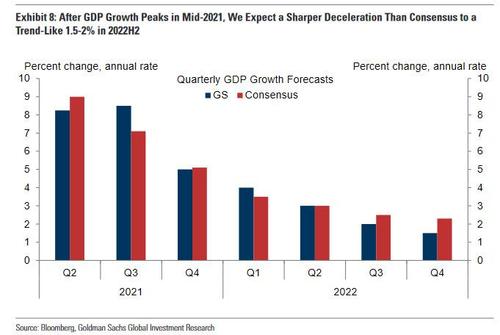

But while Goldman's expected 2021 slowdown was manageable, it got far worse in 2022, when the sluggishness is expected to truly hammer the growth rate, which Goldman now expected to shrink to a trend-like 1.5% - 2% by the second half of 2022, a far "sharper deceleration than consensus expects."

In retrospect, the bad news was just starting.

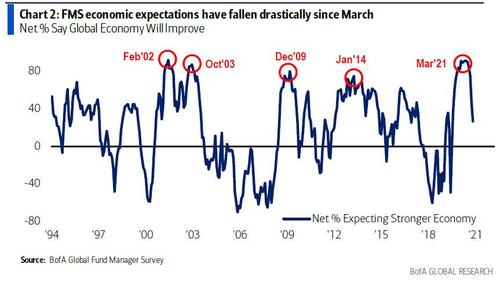

As frequent readers recall, just yesterday we pointed out that US economic growth "suddenly collapsed" as the latest dismal retail sales print showed, validating the latest BofA Fund Manager Survey which saw a collapse in expectations for everything from growth, to profits and inflation.

In response, Bank of America's chief economist Michelle Meyer wrote that "after adjusting for higher prices (PCE deflator of 4.4% qoq saar), the softening in nominal spending leads us to track only 1.5% qoq saar for real consumer spending in 3Q. This follows 2Q real consumption tracking of 12.3%." Plugging that number into the bigger GDP model, and BofA now finds that "the economy is running at a slower pace in 3Q," and currently tracking just 4.5% following the retail sales report, down from the bank's official forecast of 7% qoq saa, which is about to come down significantly.

Just hours later, Goldman strategist Chris Hussey chimed in with a preview of what was coming writing that "the combination of lower-than-expected retail sales and auto production in July, and given an increasingly likely drag on services consumption from the Delta variant, our economists are will likely revise our second-half growth assumptions even as we still do not expect material economic impact from the Delta variant in the US amidst abundant vaccine supply and relatively permissive COVID policies."

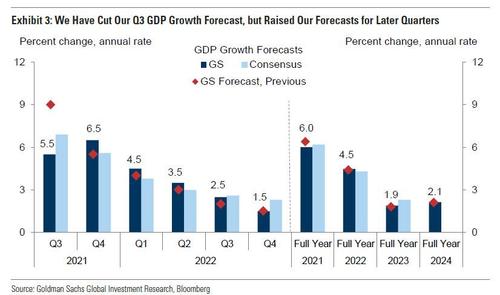

Well, he was right, and moments ago - for the second time in under a month - Goldman has slashed its Q3 GDP forecast to just 5.5% from 8.5% as of late July (and 9.5% previously), as Goldman's chief economist now warns that "the impact of the Delta variant on growth and inflation is proving to be somewhat larger than we expected."

We have lowered our Q3 GDP forecast to +5.5%, reflecting hits to both consumer spending and production. Spending on dining, travel, and some other services is likely to decline in August, though we expect the drop to be modest and brief. Production is still suffering from supply chain disruptions, especially in the auto industry, and this is likely to mean less inventory rebuild in Q3.

The bank's revised forecast also trims its full year 2021 GDP forecast to below consensus 6% (vs. 6.4% previously and 6.2% consensus) and leads to 2022 growth of 4.5%, a number which at this rate will soon be slashed to 0 or negative.

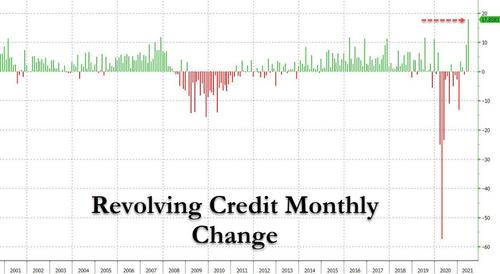

Here are some more details from Goldman behind the sharp cut to GDP, which it blames on - what else - the convenient Delta variant, and not t - say - that US consumers were once again tapped out, and with no more stimmy cash and savings all spent, was instead borrowing literally record amounts on their credit cards.

Anyway, here is how Goldman feeds the "but Delta" fiction:

The Delta variant is weighing on both consumer spending and production in Q3.

Goldman also decided to blame supply-chain bottlenecks - the same bottlenecks that were patently obvious last month yet when countless penguins, like Goldman, expected them to be "transitory." Well, they aren't looking so transitory now, eh?

If that was the extent of it, we would probably not even bother with this note: after all it's just another example of Goldman just being wrong and failing to actually observe what is going on in the economy (something we described in detail in ""A Sudden Negative Change In The Economy": Consumer Spending Slides As Majority Now Expect A New Slowdown").

But sadly it gets worse. So much so that Goldman's note is not so much about the bank's latest me culpa on its GDP forecast (it will be slashed many more times in the coming months, that much we can guarantee) but that it was the first overt admission from Goldman that the US is heading for stagflation, because while Goldman is busy cutting its GDP forecast, it was also hiking its surging inflation forecast... and to those who don't know what stagflation is, now is a good time to look it up. Here again is Kostin:

A Bigger Inflation Surge in 2021: The impact of the Delta variant on supply chains is also likely to push prices even higher in the short run on some of the durable goods categories that have contributed to the inflation surge this year.

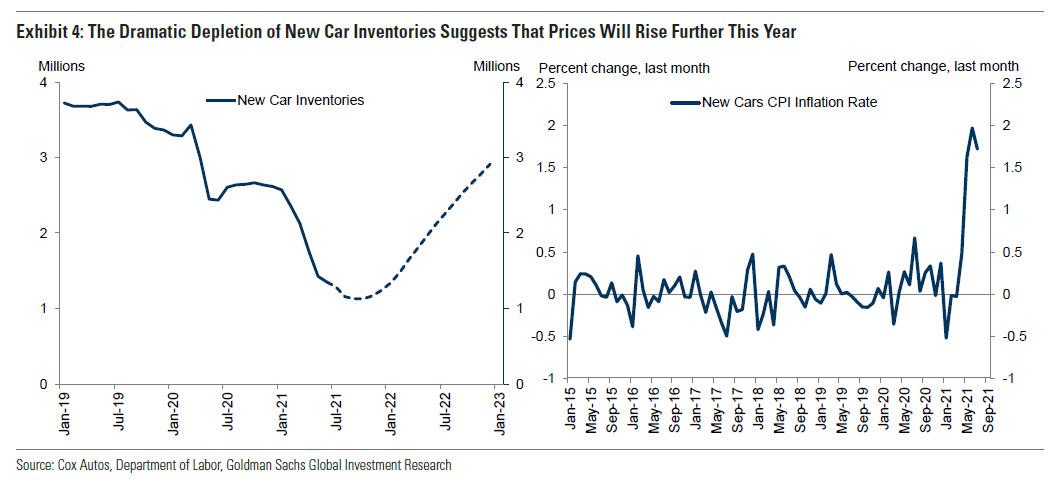

The left side of Exhibit 4 shows that, as a result of ongoing auto production problems, new car inventories are likely to fall to around 1 million, down more than 70% from pre-pandemic levels. This has led to much larger increases in new car prices in recent months than seen in many years. Our auto sector analysts expect further price increases over the next few months and then a partial return of promotional pricing at year-end as production normalizes, and we have revised our forecast accordingly.

Other durable goods that are downstream from the semiconductor shortage—such as consumer electronics and household appliances, shown in Exhibit 5—have also seen much higher than usual inflation this year, reflecting both supply constraints and strong demand. Our sector analysts expect that many consumer electronics companies will announce price increases in the upcoming earnings season and that most major household appliance producers will also raise prices significantly further this year. We have therefore bumped up our forecasts for these categories too.

But while one can, in theory, get away without spending on appliances, cars and video products, one has to eat. And sadly here the inflation is about to surge even higher.

We also raised our short-term expectations for food services inflation. In June we noted that higher wage growth for low-paid workers should flow through to higher consumer prices in sectors such as restaurants that rely heavily on low-paid labor. That has happened to an even greater extent than we anticipated in the last two CPI prints, and there is probably still a couple months of upward pressure left in the pipeline before the end of federal unemployment benefits cools wage and price pressures.

The punchline: "We now expect year-on-year core PCE inflation to reach 3.75% at the end of 2021."

So putting it all together: a drop in GDP + "a bigger surge in inflation" = stagflation. We said as much in May "This Is All About Stagflation... The U.S. Is Walking Into The Early Stages Of The Fourth Turning" and we are surprised it only took Goldman 3 months to catch up.

Comments

Log in or sign up to join the conversation.