Image Source: Pexels

Short Term Trading is one of the elusive trading strategies within Managed Futures. Often managers have been able to deliver uncorrelated historical returns. Once the manager grows above a certain limit or becomes known to the investment community, the future results tend to be underwhelming as capacity constraints and alpha decay start to bite.

Our friends at TwoQuants recently showcased a creative way to use Hedge Fund Return data. Here, we show a different way to use it, a potential way to indicate capacity constraints (or alpha decay).

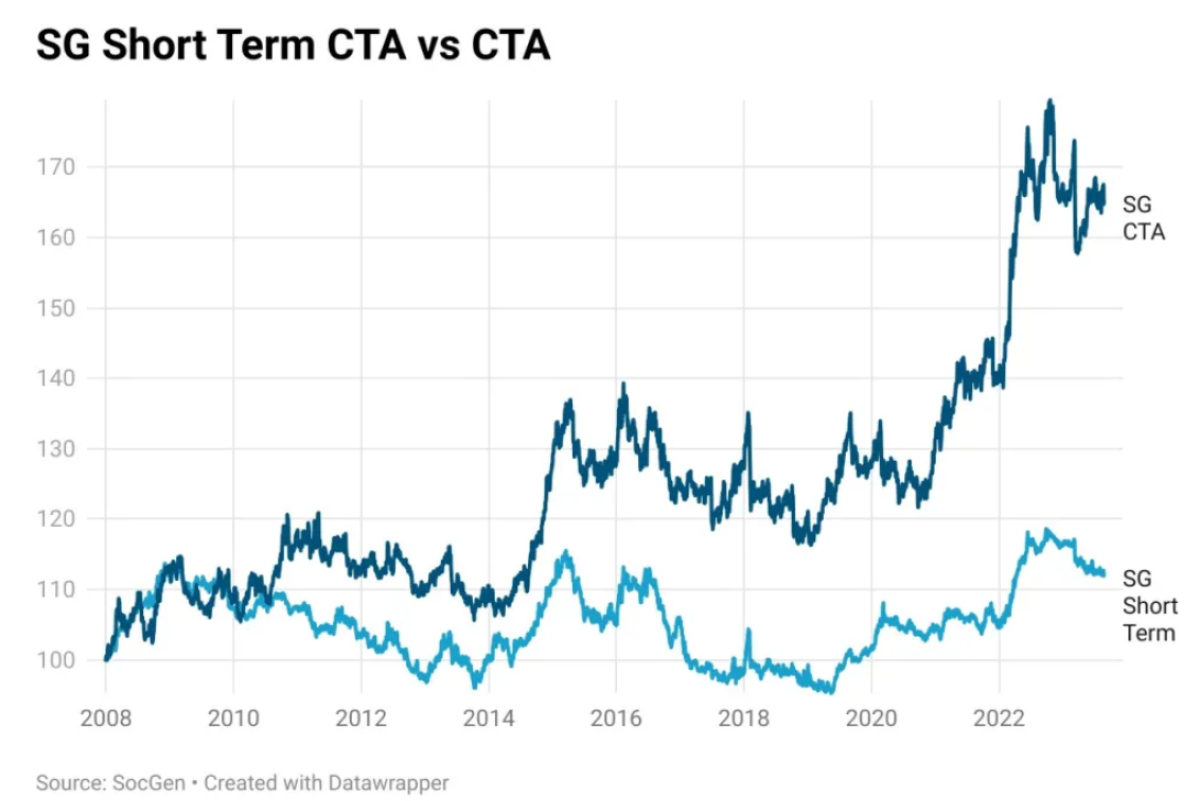

One of the longest-running short-term indices is the SocGen Short Term Traders index which consists of the largest short-term Managed Futures managers. This index has lagged behind the broader SG CTA Index (there are some overlapping names) and is highly correlated (0.6) to the CTA Index. To some extent, it looks like a strategy group that has half the upside of the CTA but similar drawdowns. Overall, investing in a group of large short-term traders has been a disappointing exercise and the return has lagged trend following strategies.

The NilssonHedge Short Term Index has similar performance characteristics compared to the SG index. We started the index in 2019, so the optics of our index are a bit better, but the returns are largely the same when adjusting for the period. Time will tell if the smaller managers in our index can contribute to stronger long-term performance.

Managing capacity is one of the most difficult issues for short-term traders. Some of the issues are not always in the control of the managers themselves. To name a few:

-

Assets under management - the more aum, the harder it is to extract the same alpha per trade. Slippage will increase and some trades have an inherent counterparty that has a specific budget to spend on trades or may change behavior if it is too costly to execute.

-

In general, a short-term trader needs to size positions larger than a longer-term trader. To state the obvious, short-term strategies also trade more often. This will reduce capacity faster than for longer-term strategies.

-

Volatility - higher volatility allows for smaller position sizing, all else equal, which will result in more opportunities for traders. Higher volatility usually results in more forced trading which creates opportunities for both trend and mean reversion.

-

Crowding - several investment banks have commoditized common short-term strategies, for instance, intraday momentum can be bought in swap format. That will reduce the available returns for short-term managers who are engaged in intraday momentum strategies.

-

And of course, alpha decay. A difficult-to-assess metric that usually coincides with declining returns for a particular investment thesis.

So, what can you as an investor do? This short post will show a quick way to estimate capacity. There are more complicated ways, and for more serious treatment, you should adjust for the overall market opportunity and only look at the excess returns for a particular strategy compared to their peers.

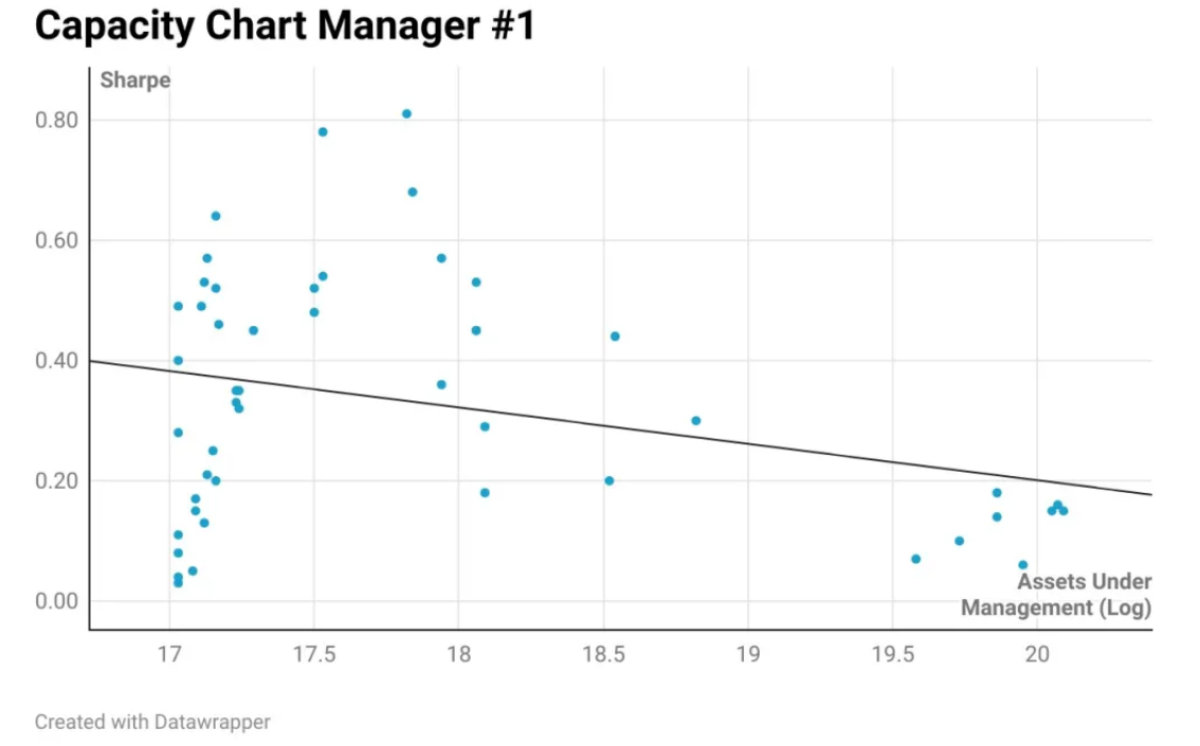

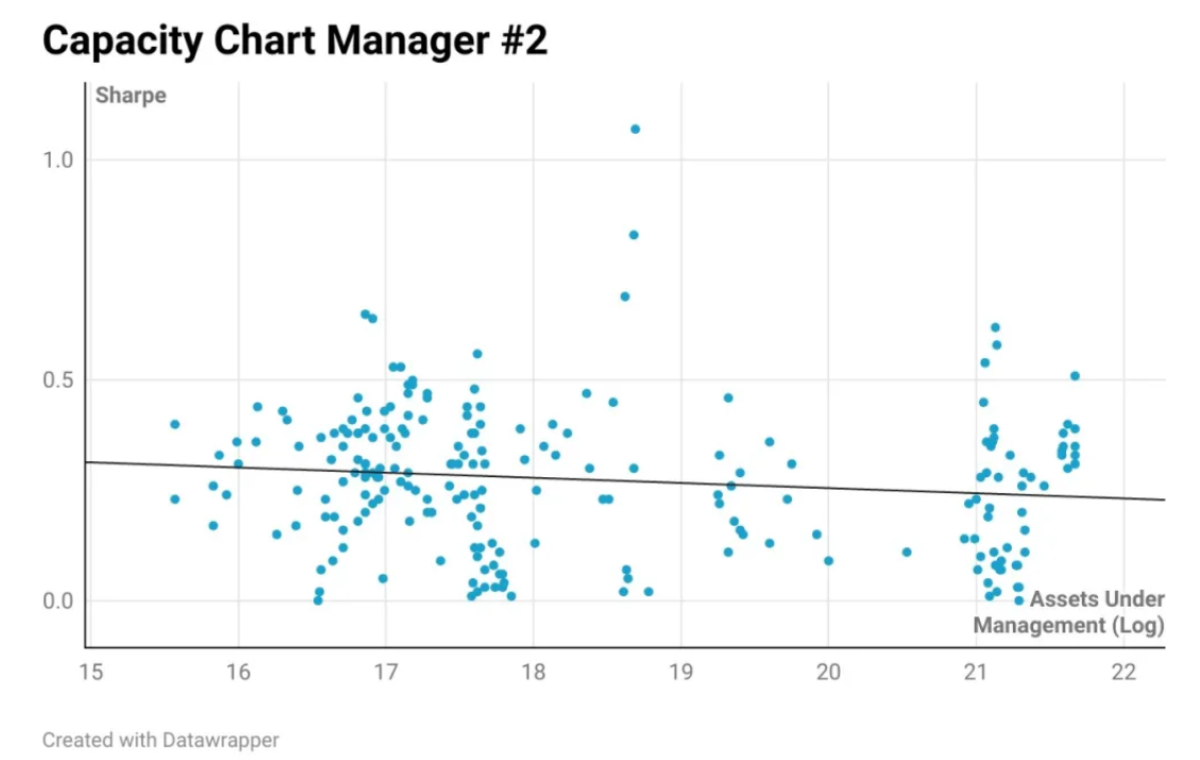

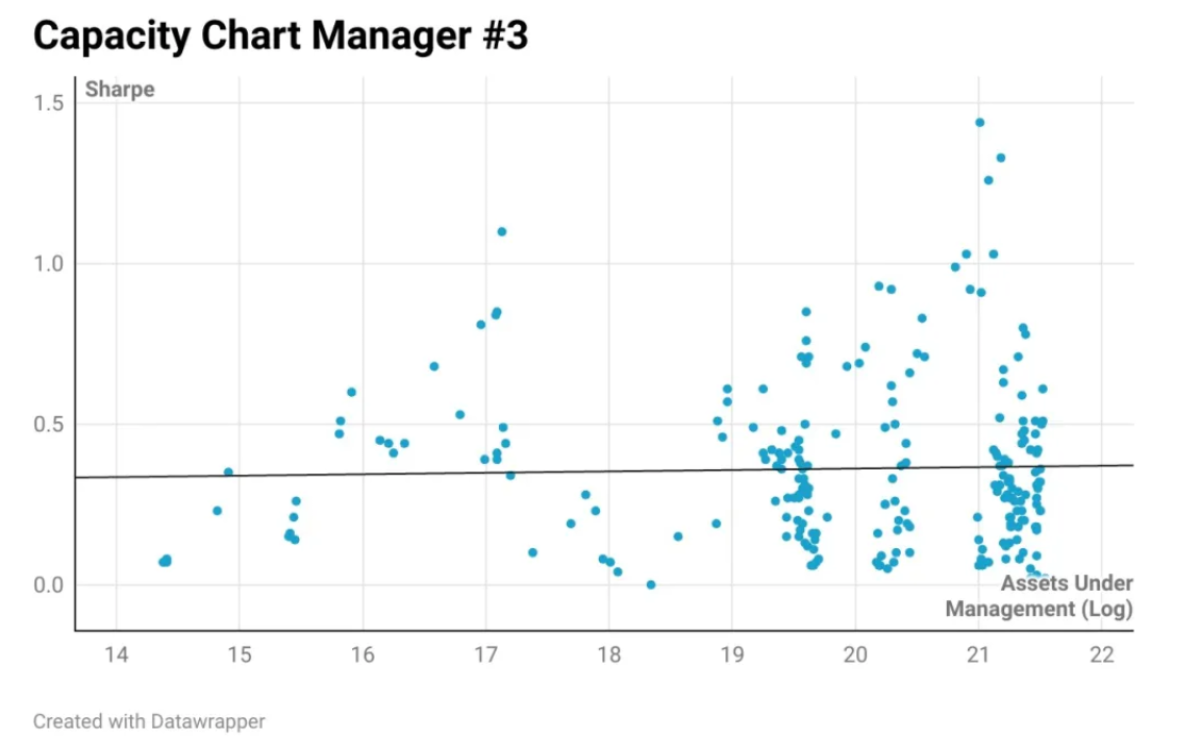

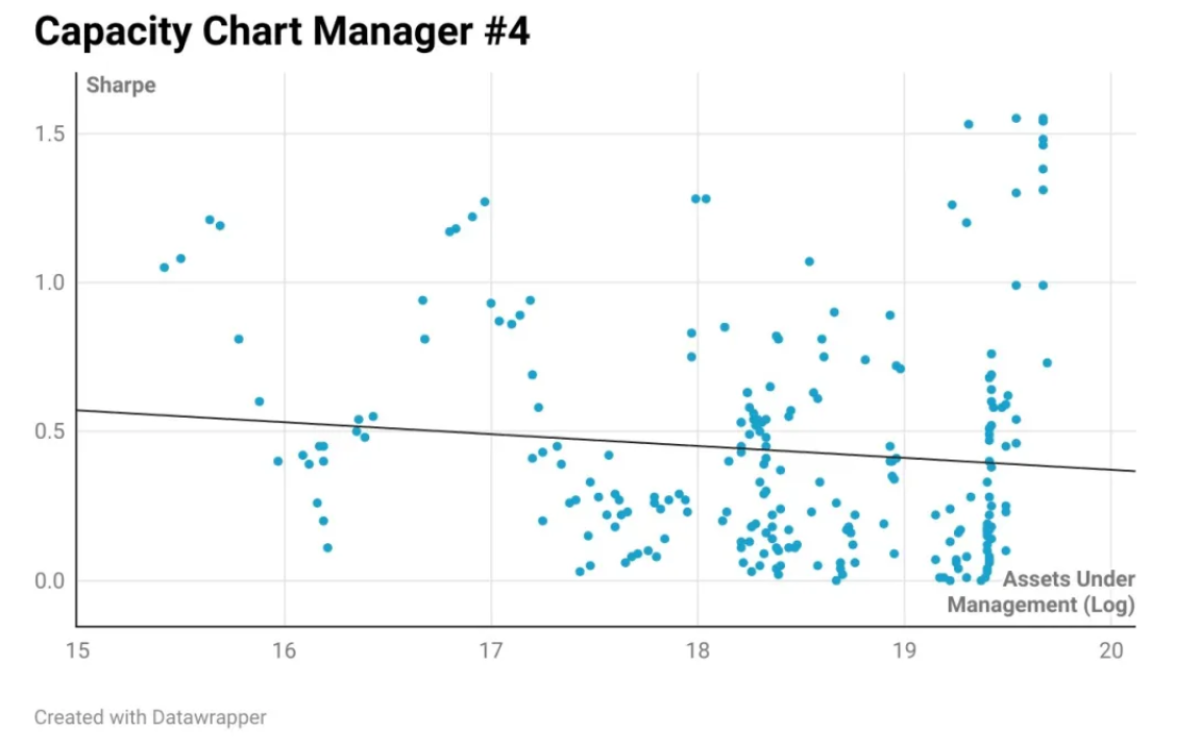

One naive way to quickly estimate capacity is to regress assets under management against the realized Sharpe ratio. We do so for a few short-term managers and some of them show a strong sensitivity to increased assets. We use (natural) logged assets under management and one unit change is roughly a doubling of aum.

Each of the four managers has unique and different trading styles and different sensitivities to market conditions and assets.

-

Manager #1 A manager depending on a few select strategies, using AI and Fundamental data, seems to have a capacity constraint. Here an investor would require more due diligence to figure out the trading strategy and how it develops.

-

Manager #2 A short-term manager with a high trend correlation, this manager only seems to have a modest capacity dependency. The decline is largely explained by lower efficiency for Trend Following over this period, a sub-strategy for the manager.

-

Manager #3 is a diversified short-term trader, with multiple portfolio managers. Here capacity seems to be well managed and there is no clear dependency.

-

Manager #4 is a short-term equity-focused manager. The strategy is probably capacity-constrained but is also more environmentally dependent as it only trades one market sector.

More By This Author:

On The Unintended Consequences Of AI And AutomationAlternative Investments During 2023: Money Growing On Trees

Reflections From The Middle Seat: An Allocators Journey To Private Capital Advisory

Comments

Log in or sign up to join the conversation.