UK wage growth is proving sticky, though falling vacancy rates – particularly in hospitality – and lower private-sector employment point to a gradual reduction in pay pressures in 2025.

The first jobs report of the year paints a familiar picture of the UK labour market. Wage growth remains hot, and indeed excluding bonuses, was a tad hotter than expected at 5.6% year-on-year. That said, if you to get really into the details, the month-on-month increase in private-sector pay – a metric the Bank of England occasionally looks at – appeared more muted in the latest period. But generally, these figures have been proving uncomfortably sticky for the Bank.

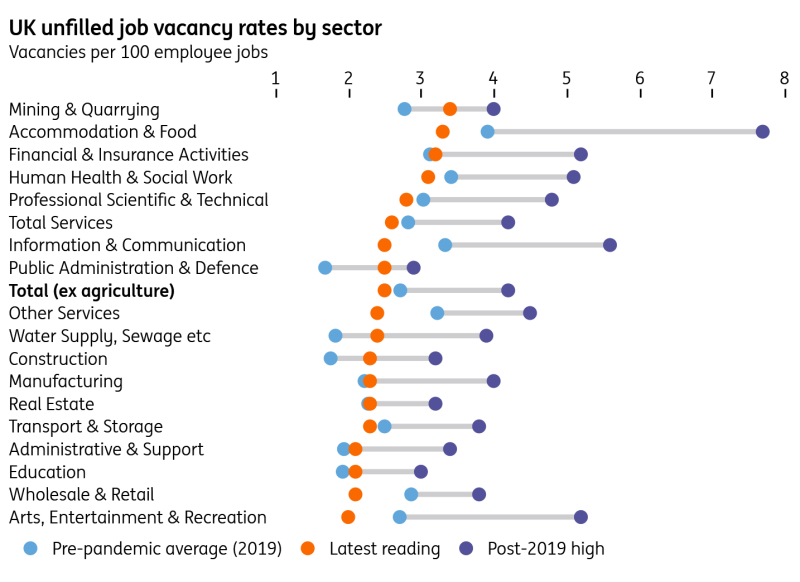

At the same time, plenty of evidence shows that the jobs market is continuing to cool down. Remember, don’t pay any attention to the unemployment rate, plagued by long-running and well-known quality issues. Instead, take a look at vacancies. These were down fractionally in the latest data, and more importantly, most sectors now have vacancy rates below pre-Covid levels – in some areas quite significantly so. Just look at hospitality or retail.

Vacancy rates below pre-Covid levels in most sectors

(Click on image to enlarge)

Source: Macrobond, ING calculations

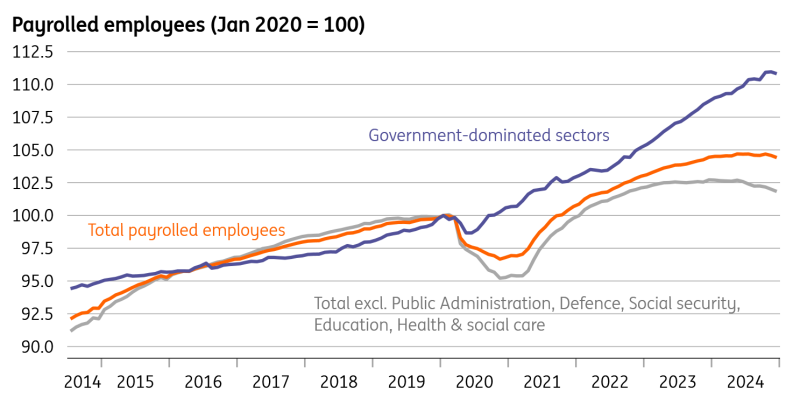

Then there’s payrolled employment, which is perhaps the most reliable jobs indicator we have right now. If we strip out government-dominated sectors like health and education, the number of payrolled employees fell by 0.9% across 2024. That’s not a huge number, but this all points to a backdrop where wage growth can come lower across 2025. Indeed if we look at the latest couple of readings from the Bank of England’s own Decision Maker Panel (a survey of CFOs), it shows that expected wage growth has finally slipped below 4% as of the past couple of readings.

Payrolled employment fell in 2024 outside of government-heavy sectors

(Click on image to enlarge)

Source: Macrobond, ING calculations

Nothing here is likely to change the Bank of England story dramatically, and it looks like policymakers are on course to continue gradually taking rates lower and probably more rapidly than markets now expect. Investors are largely pricing a February rate cut, but only 60 basis points of total easing this year.

More By This Author:

FX Daily: Day One VolatilityRates Spark: Trump’s Government Is Now A Fact

Temporary Relief On U.S. Trade Triggers A Dollar Correction

Comments

Log in or sign up to join the conversation.