UK PMIs Signal Omicron Rebound And Stubborn Inflation

Signs of a growth rebound and ongoing inflationary pressures from the latest purchasing manager indices will act as another green light for Bank of England policymakers, who look poised to hike interest rates again in March and May.

The latest UK purchasing manager indices will tick a lot of boxes for Bank of England policymakers.

Firstly – and perhaps unsurprisingly – the services index jumped by almost seven points to 60.8, the highest reading since the reopenings last spring. Admittedly we should probably avoid reading too much into the size of that increase, given it's consistent with what we’ve seen just after other bouts of Covid turbulence. Ultimately, these indices are simply telling us that a greater proportion of firms are seeing increases in output as government restrictions and Covid caution eases, and the read-across to GDP hasn't always been great.

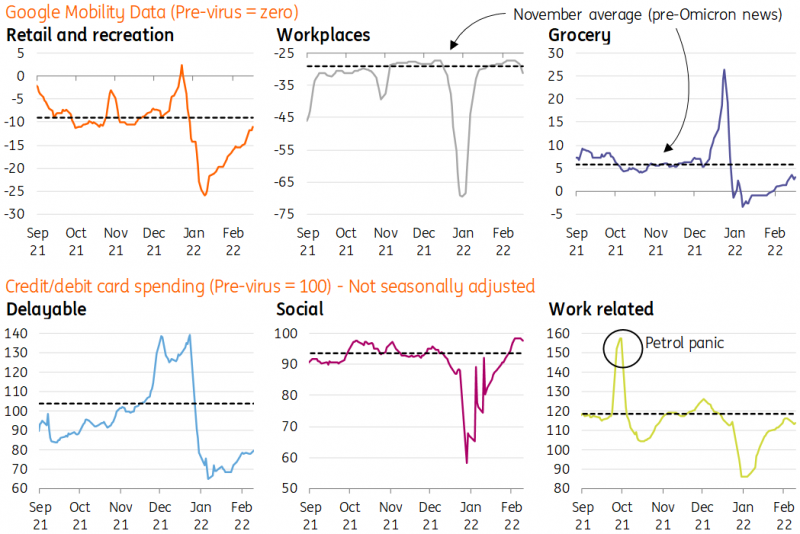

Nevertheless, it’s yet another hint that Omicron has done very little lasting damage to the UK economy, and the data is consistent with what we’ve seen with just about every other high-frequency indicator. The chart below shows that mobility and card spending (at least related to socializing and workplaces) is virtually back to pre-Omicron levels. The most recent edition of the ONS business survey also pointed to reduced staff illness now Covid-19 case rates have subsided.

After only a fairly mild hit to December’s monthly GDP, we think we could see successive rebounds in January and February. Overall first-quarter GDP growth could be in the region of 0.5%.

Mobility and spending data points to post-Omicron rebound

Image Source: Macrobond, ING

But it’s the survey’s findings on inflation that will really catch the attention of the Bank of England. The IHS Markit/CIPS press release cites “severe inflationary pressures” and the second-highest rate of cost pressure since the survey began in 1998. Much of the BoE’s recent hawkishness appears to be premised on its own survey evidence from its agents, which has pointed to circa 5% wage growth this year.

All of this is effectively another green light for a rate hike in March, though we have our doubts that policymakers will go for a sharper, 50 basis-point increase at that meeting. The committee narrowly opted against doing so in February on the basis that it would risk adding yet more fuel to 2022 rate hike expectations.

In practice, markets have ramped up expectations regardless, and investors are now pricing close to six rate rises for the remainder of 2022. We wouldn’t be surprised to see policymakers offer some modest pushback against this in the various speeches and testimonies this week.

Ultimately, we think markets are overestimating the pace of tightening this year. We expect hikes in March and May, and perhaps another later in the year, but that might be it. We expect some of the recent sources of wage pressure to ease later in the year, while the sharp increase in living costs will keep a lid on economic growth in coming quarters.

Disclaimer: This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information ...

more