The bar is set pretty high for the Bank of England to accelerate the pace of rate hikes to 50 basis points this week. But another inflation shocker all but guarantees a 25bp hike tomorrow and another in August.

Headline inflation remained unchanged at 8.7% in May

It’s another month where UK inflation has come in dramatically higher than expected, and that all but guarantees another rate hike from the Bank of England tomorrow. Headline inflation remained unchanged at 8.7% in May, and because the contribution from energy and food reduced, that means core inflation actually rose to 7.1% from 6.8% previously.

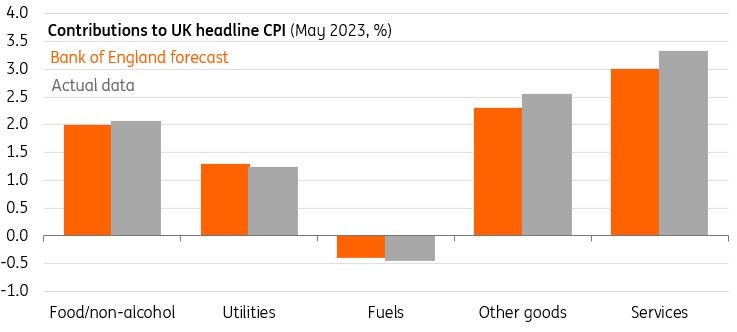

Unfortunately, things look just as concerning when you look into the figures in more detail. The Bank of England is most focused on services inflation because it tends to exhibit more persistent and less volatile trends. And here we saw a further increase in the annual rate of inflation, and that means the contribution from services to overall headline CPI is about 0.3pp higher than the BoE had previously been forecasting. Crucially, this upside surprise doesn’t appear to be concentrated in any single category.

How May's inflation data compare to the BoE's forecast

Macrobond, ING calculations, Bank of England

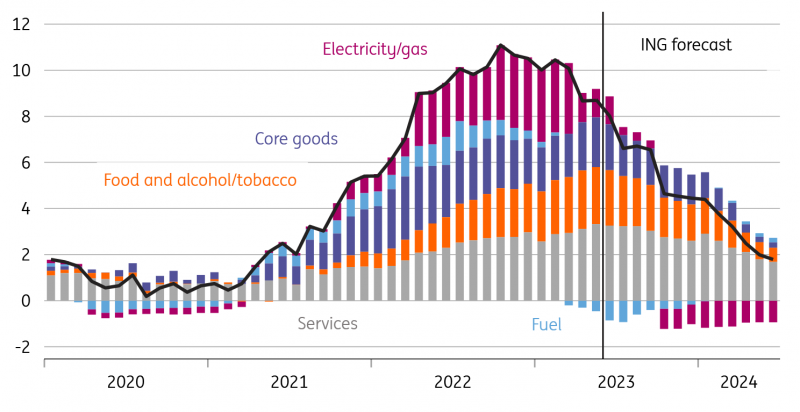

Headline inflation should come down more noticeably over the next couple of months, owing to some pretty hefty base effects. Last June saw a near 10% spike in petrol prices, whereas prices are currently falling, and of course in July we’ll see a material fall in household electricity/gas bills. Core inflation we think should come lower too, though to a much lesser degree and mainly because of further renewed downward pressure from certain goods categories.

Headline CPI, we think, will be just below 7% by July and around 4.5% by year-end. Core inflation will probably end the year above 5%.

All of this makes life even harder for the Bank of England. We think the bar for another 50bp hike is set pretty high, but a 25bp hike is basically guaranteed, as is another in August. But markets are now fully pricing a 6% peak for the Bank rate, which implies six more rate hikes from current levels. That seems excessive, and we suspect the Bank of England would privately agree.

When rates got this high last November, the BoE offered some rare pushback against market expectations and signaled a lower peak for rates. But this time, with inflation consistently coming in hotter than expected, we suspect officials will be more reluctant to offer any firm guidance on what comes next. Policymakers won’t want to steer market rate expectations lower, only to find that further inflation surprises force it to go further than it would like over the coming months.

UK inflation should come in lower in June/July on energy base effects

Macrobond, ING forecasts

Ultimately though, 6% rates would be extremely restrictive. The current structure of the mortgage market – whereby the vast majority of households are fixed for either two or five years – means rate hikes filter through to the economy fairly gradually. That means that the length of time rates stay restrictive is arguably more important these days than the absolute level interest rates reach over the shorter term. As the BoE itself has made clear, the impact of all those past hikes is still largely to hit the economy – and just taking rates to 5% and keeping them there would exert a large drag on the economy.

We also expect the news on inflation to get a little better through the summer. The BoE’s survey measures of inflation have been improving, and forward-looking indicators like producer prices point to more noticeable declines in headline CPI later this year. Crucially, we think the fall in gas prices is good news for service sector inflation and suggests we could get more noticeable disinflation in this sector, even if wage growth takes longer to ease.

More By This Author:

FX Daily: Powell Set To Sail FX Markets Into The Next Data Releases

China: Loan Prime Rates Lowered

FX Daily: Dollar Trapped Between Inverted Curves And Rallying Equities

Comments

Log in or sign up to join the conversation.