We think UK inflation is now only fractionally away from the peak, which is likely to come in October.

But depending on how the government's energy price guarantee is structured beyond April next year, inflation could be 2-3pp higher for much of 2023 if most consumers switch back to the Ofgem regulated price for electricity and gas.

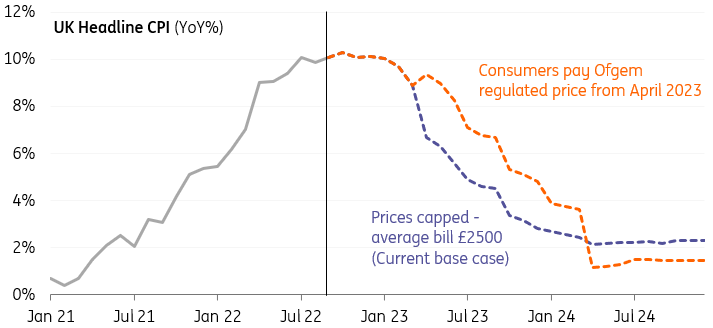

UK inflation is back into double-digits once more and at 10.1% is the highest rate in 40 years. But we think we’re only fractionally away from the peak now, which is likely to come in October – though in practice we’re likely to see inflation hover in the 10-10.5% range through to January. Food prices are still a key source of pressure, though there are very early signs in the producer price data that month-to-month gains are slowing. Food inflation is close to 15% now, but again that’s probably close to peaking out.

Elsewhere, there are good reasons to think inflation should begin to ease through 2023. Inventory levels among retailers are spiking now supply chains are gradually improving, and more importantly, consumer demand is flagging. That potentially points to aggressive discounting in coming months, or at the very least slower price rises in durable goods categories.

But the key question for the 2023 inflation outlook now relates to the energy price guarantee. We explained in more detail yesterday that the Chancellor’s decision to make the government’s energy price support more targeted could see most consumers switch back to the Ofgem-regulated price from April. We still need to see how this is going to work in practice, but such a scenario could add between 2-3pp to headline inflation from April onwards.

Making energy price guarantee more targeted could add 2-3pp to inflation from April

Source: Macrobond, ING

While on paper you could make a hawkish case out of that for the Bank of England, in practice it’s more likely to be the opposite. The dramatic scaling back of fiscal support by the new Chancellor will be seen as lowering medium-term inflation, and that’s what BoE policymakers will be more interested in. We’ve scaled back our forecast for November’s meeting to a 75bp rate hike, from 100bp previously.

The hawks at the BoE will still be acutely worried about the value of the pound and the potential for any further weakness to add to medium-term inflation. But the alternative is hiking aggressively and baking in the extremely high mortgage/corporate borrowing rates now on offer - something which is only likely to amplify a winter recession. We, therefore, think it's more likely that Bank Rate peaks between 3.5-4% by early next year, below market expectations.

More By This Author:

The Commodities Feed: Further US SPR ReleasesRates Spark: The Ball Is In The BoE’s Court

FX Daily: Corrective Forces Build

Comments

Log in or sign up to join the conversation.