UK Growth Cools As Headwinds Begin To Build

The UK's September GDP figures are much less exciting once health spending is stripped out, and overall growth momentum appears to be slowing (albeit not to a total stop). But Bank of England policymakers are more focused on jobs data right now, and a December rate hike still looks more likely than not.

A general view of the skyline and high-rise buildings in London, Britain

At face value, September's UK GDP figures look quite good. Activity grew by 0.6% during the month, though as has often been the case through the pandemic, the majority of this comes from the way health spending is documented in the GDP figures. Once you strip out the effect of people returning to in-person doctor appointments and also other pandemic-related spending, UK growth appears less exciting. Third-quarter GDP came in at 1.3%, a touch lower than expected.

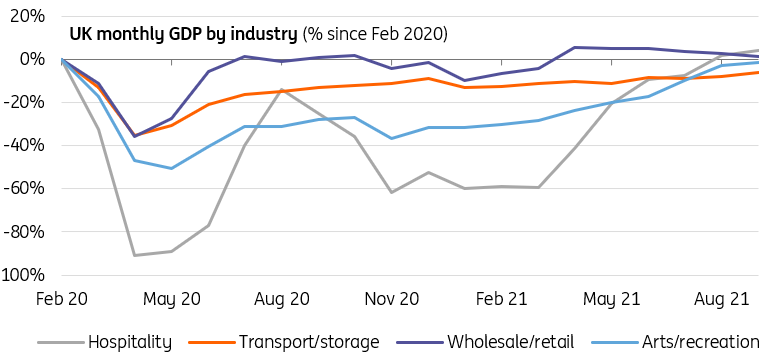

Having said all of that, the economy is still growing - albeit slowly. We have continued to see a further recovery in the hardest-hit sectors of the economy - and remarkably, the hospitality industry is now further above its February 2020 level than wholesale/retail. Partly that's a function of more staycationing over the summer, but it also suggests a fairly rapid rebalancing in spending away from goods and back towards freshly-reopened services.

Source: Macrobond, ING

Nevertheless, we expect growth momentum to remain slow into the fourth quarter. We expect the monthly readings to average around 0.1-0.2% for the next few months, and we think the fourth quarter will record growth in the region of 1% and potentially below.

None of this is likely to have much of a bearing on when the Bank of England hikes first. The real test is what happens to the jobs data now that the furlough scheme has ended, and on that score, the committee will get two more reports before the December meeting. Encouragingly, early signs suggest there has been no discernible increase in redundancy levels since the scheme ended in September, though the effect may show up more visibly in measures of underemployment.

It’s a close call between a December and February rate rise, though we think the former is more likely - especially if the jobs data brings the committee good news. But the pace of tightening thereafter is likely to be cautious, and we expect a maximum of two further rate rises in 2022.

Disclaimer: This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information ...

more