Despite an extra bank holiday in May, the UK economy shrank by only 0.1%. Over the next few months, the economy should benefit from the improving real wage story, though rising interest rates will ultimately drag on growth over coming quarters.

The UK economy performed better than expected in May, with GDP falling by just 0.1% across the month. We had been expecting a more tangible hit from the King’s Coronation and the extra bank holiday, given last year’s royal events saw temporary declines in activity worth 0.7% of GDP in June and September. In reality, we shouldn’t be drawing too many conclusions from this better-than-expected data, other than perhaps that the nature of the modern economy means it’s more adaptable to these kinds of events than it might have been 10-20 years ago.

The upshot is that the economy is no longer likely to contract in the second quarter, and we now expect modest 0.1% growth for the three-month period as a whole. But given that most/all of May’s lost output, had it fallen more sharply, would have been regained in June, the knock-on effect on the third quarter and beyond is minimal.

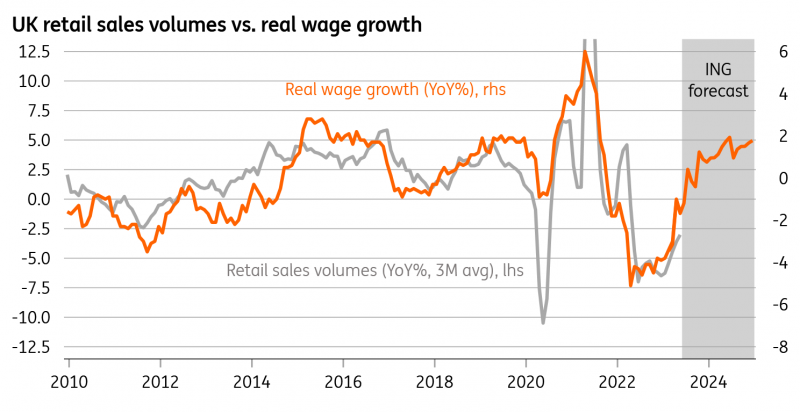

The real wage story means the worst is behind us for retail

(Click on image to enlarge)

Macrobond, ING calculations

Away from the month-to-month volatility in these GDP figures, we think the UK economy should grow modestly over the next quarter or two. It should benefit from the improving real wage story, especially now that electricity/gas bills are down roughly 20%. As time goes on the impact of higher mortgage rates will bite, but the high prevalence of fixed-rate mortgages and the fact that only 28% of households have a loan on the property they live in, means it is going to be a gradual pass-through. The impact of higher rates on corporates – particularly small businesses – may become more noticeable, given these firms are typically on floating-rate debt.

For the Bank of England, the focus is still very much on the CPI and wage numbers, and not a lot else for the time being. Tuesday’s higher-than-expected regular pay figure bolsters the chance of a second 50bp hike, though much hinges on next week’s inflation figures.

More By This Author:

The Commodities Feed: Brent Breaks Above $80

Eurozone Industrial Production Confirms No Strong GDP Bounce Back For 2Q

FX Daily: Dollar Drops On The Disinflation Trade

Comments

Log in or sign up to join the conversation.