Wednesday’s Spring Statement from the UK Chancellor will be the third fiscal event since last September but hopefully the least dramatic. Lower gas prices are good news for the public finances, but potential revisions to the medium-term outlook offer little-to-no room for the Chancellor to shelve plans for tighter public spending this decade.

The near-term fiscal outlook looks brighter

The collapse of Silicon Valley Bank last week forced the Chancellor and Bank of England to spend the weekend looking at ways to prevent contagion. But the private purchase of SVB UK announced at the start of the week means much of the focus of this week’s Budget can now switch back to domestic policy issues.

Cast your mind back to November when Chancellor Jeremy Hunt was under a lot of pressure to present a fiscal plan which stabilized the public finances across the medium term. In truth, markets had already begun to stabilize by the time of the Autumn Statement, and Hunt was able to strike a balance between offering some modest support to the economy in the near term while promising some fairly aggressive restraint on public spending further down the line.

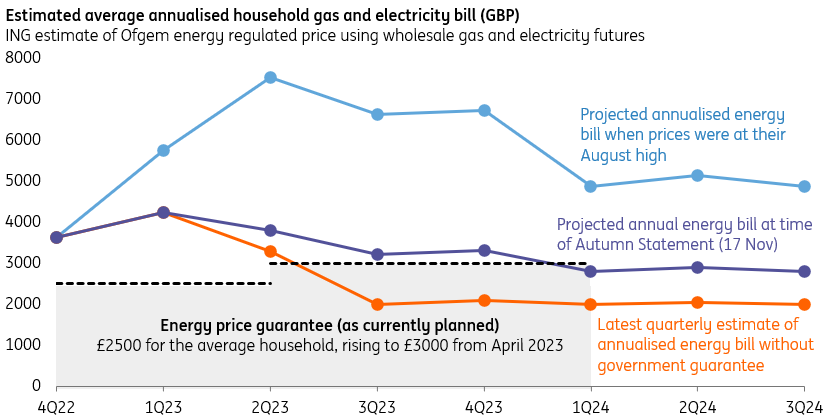

The good news for the Chancellor is that the fall in wholesale gas prices has drastically reduced the cost of supporting household energy bills. By our calculations, the estimated cost of the Energy Price Guarantee in FY2023 has fallen from £13bn in November to less than £2bn now. That should allow the Chancellor to scrap the planned increase in unit electricity/gas prices in April.

Projections for household energy bills have fallen with wholesale gas prices.

Image Source: Ofgem, Refinitiv, ING

That would keep bills at £2500 on an annual basis for the average household, instead of rising to £3000 as planned. In practice, households will still pay more, as a fixed £400/household discount expires this month, though this will be partly offset by planned one-off payments to low-income/vulnerable households. We assume these payments will continue, even if the average energy bill will no longer rises.

More importantly, by July the government probably won’t be supporting energy bills at all, with wholesale prices pointing to a fall in the average annualised bill to roughly £2000-2100. To be clear that’s still roughly double the pre-2022 level, but the fact that it isn’t several multiples of that should help the UK avoid a deeper recession – and may mean it avoids one altogether in the first half of the year.

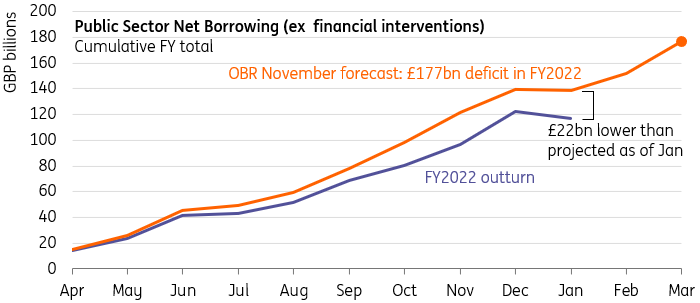

The near-term fiscal situation is also helped by lower headline inflation projections (thereby lowering debt interest). Borrowing over recent months has also undershot the Office for Budget Responsibility’s forecast by roughly £22bn.

Borrowing has come in lower than expected throughout this fiscal year

Image Source: Macrobond, ING, OBR

Lower growth and higher inflation in the medium-term offer no wiggle room for giveaways

Unfortunately, that’s probably where the good news will stop for the Chancellor this week.

The medium-term fiscal picture, which will help determine how much “headroom” (if any) the government has against its target for debt to eventually fall as a percentage of GDP, won’t change much. That target is heavily influenced by forecasts from the Office for Budget Responsibility. Here, we could begin to see downgrades to medium-term growth forecasts, which previously have looked much too optimistic. We’d also expect upgrades to inflation forecasts beyond this year, with the OBR having previously forecast negative CPI in 2024/2025.

In short, there’s little – if any – room for the Chancellor to water down some of his plans for fiscal restraint later this decade. And the reality is that these plans still look like they'll be difficult to implement. With day-to-day spending already under heavy pressure due to inflation, reducing capital investment is likely to be the path of least resistance (at least politically) when it comes to curbing government expenditure. The decision to scale back the High-Speed Two rail project is a timely reminder of that, and November’s budget already projected Public Sector Net Investment to fall from 3% of GDP this year to 2.2% later this decade.

Market rates and 2023-24 issuance: higher borrowing and skew to shorter bonds

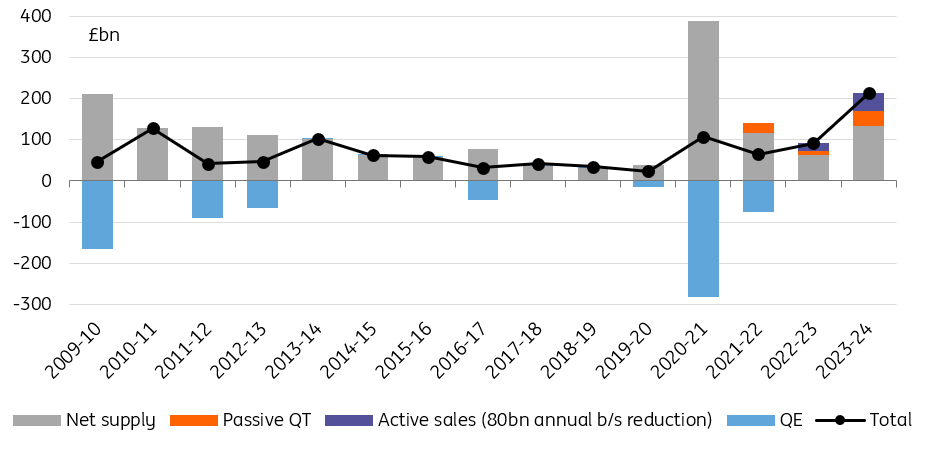

When it comes to borrowing, the Debt Management Office (DMO) will be busy over the next fiscal year. We’re expecting a jump in gross gilt issuance to £250bn in FY2023-24, which will translate to £133bn of net supply after redemptions are taken into account. Regular readers know that this is not our preferred measure of the draw on private investors, however. Instead, we like to look at this net supply corrected for BoE buying/selling, and here the picture is slightly more alarming. Private investors will be required to increase their holdings of gilts by £210bn next fiscal year. For reference, we estimate this is only £92bn in this fiscal year.

There's a lot of gilt supply for private investors to absorb next fiscal year

Image Source: Bank of England, DMO, ING

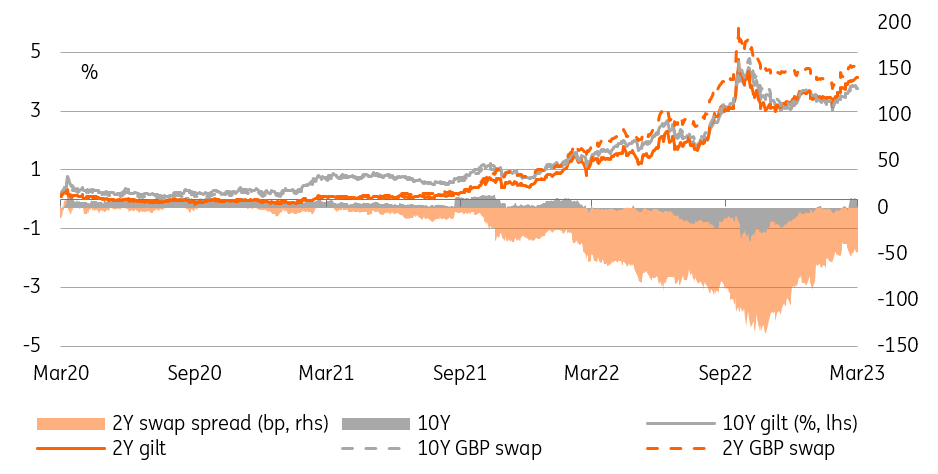

This begs the question of where will all this extra demand come from. Clearly, a greater draw on private investors should make the DMO more cautious when it comes to its borrowing strategy. A lot of the extra weight, we expect, will be coming from yield-sensitive investors. In other words, investors who after years of being side-lined by low-interest rates should aim for a greater allocation into gilts. For the same reason, we think investors who were forced to buy longer-dated bonds when rates were low on shorter ones, will now return to the short end of the curve.

The differential between gilt and swap rates has been narrowing

Image Source: Refinitiv, ING

This is partly why we expect short and medium-maturity bonds to make up a greater proportion of the DMO’s issuance next year, while the amount of long-dated and index-linked gilts are less likely to scale up in proportion to overall gilt issuance. We’ve been flagging this sharp increase in issuance for some time now, and indeed, it was a key factor behind the September 2022 mini-Budget ‘doom loop’ that saw gilt yields soar.

Since then, the rate differential between gilts and swaps has increasingly been reflecting the wall of gilts about the hit the market over the next fiscal year. These so-called swap spreads are now back above 0bp at the 10Y point, and we think greater short and medium issuance in the coming year will also help bring that spread closer to 0% at shorter maturities.

More By This Author:

Turkey: External Financing Remains A ConcernAssessing The Silicon Valley Bank Fallout

Surprise UK Growth Rebound Means Technical Recession Could Be Avoided

Comments

Log in or sign up to join the conversation.