February balance of payments data in Turkey confirms a challenging flow outlook, while a reversal in portfolio inflows following recent domestic events are likely to further weigh on the financial account. In our view, risks are skewed towards a narrowing external deficit with challenging external financing conditions.

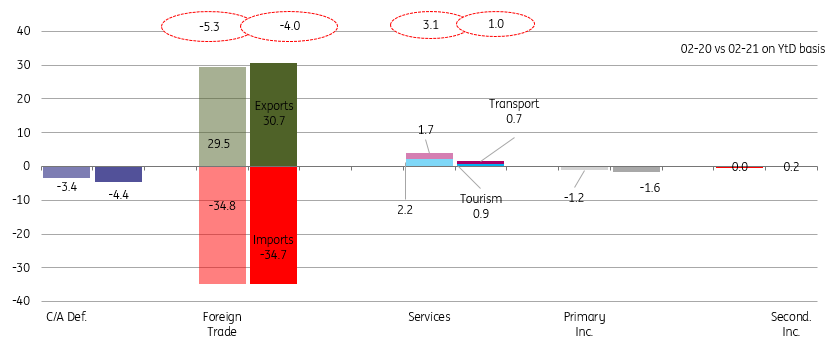

Turkish current account deficit in February at US$2.6 bn showed a relative deterioration over the same month of 2020 mainly on the back of continuing narrowing of services surplus, while goods balance remained practically unchanged. The 12-month rolling deficit, on the other hand, recorded a further increase to US$37.8 bn, roughly translating into 5.3% of GDP.

Source: Shutterstock

The details of foreign trade show that the net gold deficit that signals direction change in January moderated further in February. We also saw the continuation of the decline in the energy bill. However, expansion in core deficit (excluding gold and energy) limited the improvement.

Breakdown of current account (US$ bn, on YtD basis)

(Click on image to enlarge)

CBT, ING

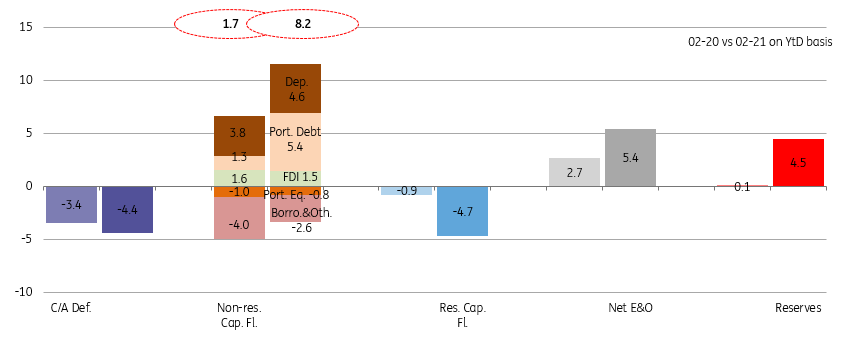

Capital account has remained positive with US$1.7 bn in February, though the level of inflows portrays a fragile outlook.

With another significant net error & omissions at US$1.9 bn (US$5.4 bn in the first two months) more than offsetting the current account deficit, reserves have recorded a further increase with a US$0.9 bn.

In the breakdown, residents posted US$1.5 bn inflows, determining the capital account outlook in February driven mainly by local banks’ contracting deposit holdings abroad.

Non-resident flows were hardly positive at US$0.2 bn thanks to the impact of non-debt creating items attributable to gross FDI at US$0.9 bn despite the continuing sale of foreign investors in the equity market amounting to US$0.5 bn in February. On the flip side, key debt creating items witnessed a small US$0.3 bn outflows on the back of long term debt repayments of banks a US$0.5 bn. Accordingly, in February alone, the long-term rollover ratio for the banking sector was at 67% comparing with 124% for the real sector.

Breakdown of capital account (US$ bn, on YTD basis)

(Click on image to enlarge)

CBT, ING

Overall, February data confirms the challenging flow outlook for Turkey, while reversal in portfolio inflows following recent domestic events should further weigh on financial account.

Going forward, real estate related inflows, government borrowing and level of corporate rollovers should help ease pressures. On the current account, core imports which are closely associated with domestic demand can show some correction this year depending on the continuation of tight credit policy and demand control while the evolution of gold imports will also be key for the external balances.

In our view, risks are skewed towards a narrowing external deficit with challenging external financing conditions.

Comments

Log in or sign up to join the conversation.