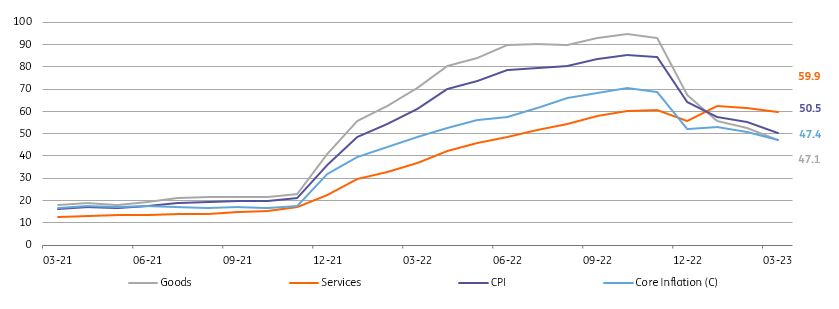

A better-than-expected reading of 2.29% in March left the annual inflation rate at 50.5%, down from 55.2% a month ago. This deceleration was due to the large comparison base effect.

Shoppers at a street market in Antalya, Turkey

Cumulative inflation in the first three months reached 12.5% (vs the Central Bank of Turkey's 22.3% forecast for the whole year in the January inflation report) following the second-highest March reading in the current inflation series, which began in 2003. Therefore, while the latest data still shows strong pricing pressures, the increase in all groups was lower than last year, which helped the drop in the headline. We will likely see a further fall in the near term with the presence of large base effects if stability in the lira continues.

The underlying trend (as measured by the three-month moving average, annualized percentage change, based on seasonally adjusted series) for goods inflation remained broadly unchanged in comparison to the last month. However, the services group has further deteriorated, driven by rent, contributing to the elevated underlying trends of core and headline in March.

PPI inflation recorded another sharp drop to 62.5% year-on-year, the lowest reading since November 2021, implying high but relatively improving cost-push pressures in comparison to previous months. While the monthly reading was at 0.4% with support from price drops in utilities and energy, the base effects have been the main determinant of the decline in annual inflation.

Annual inflation (%)

Core = CPI excluding energy, food & drinks, alcoholic beverages, tobacco, gold

Source: TurkStat, ING

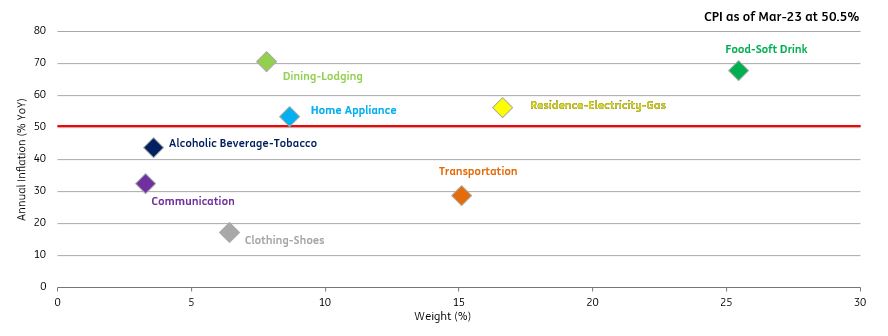

In the breakdown of the main expenditure groups:

- Annual inflation in the food group declined thanks to fresh fruit & vegetables in the unprocessed food group, and bread & cereals in the processed food group. However, the monthly figure more than doubled the long-term March average, pulling the headline up by 1.02ppt. Accordingly, the annual rate of increase in food prices slowed to 67.9%, but it remained significantly above the food price assumption in the Inflation Report, at 22%.

- We see food prices continuing to impact catering prices, making them a strong contributor, with a 0.32ppt impact on the headline rate.

- With a 0.31ppt impact on the monthly headline rate, housing was among the major contributors thanks to continuing upward pressure on rents.

- Home appliances on the other hand impacted the headline by 0.23ppt given the sensitivity of the items in this group to domestic demand and exchange rate developments.

- Transportation, which was the key inflation driver last year, did not lead to a major impact in March given the significant decline in energy prices.

- The only group that reduced the monthly reading was clothing, with a 1.9% decline while annual prices change in this group stood at a mere 17.3%, decoupling from other groups in the CPI basket.

As a result, goods inflation moderated to 47.1% YoY, while annual inflation in services recorded a 59.9% YoY increase, close to the peak of the current inflation series, driven particularly by rent and catering.

Annual inflation in expenditure groups

Source: TurkStat, ING

The downtrend in annual inflation in March is likely to continue in the coming few months mainly due to strong base effects, though currency stability will remain key for the outlook. Given deeply negative real interest rates, further disinflation would be quite challenging, while risks to the outlook this year are on the upside given the deterioration in pricing behavior, higher trend inflation and the still-elevated level of cost-push pressures.

In the March MPC, the CBT hinted that it would maintain a wait-and-see mode, while we can expect further macro-prudential measures to maintain favorable financial conditions to minimize the effects of the earthquakes. In recent weeks, we saw a reduction in the maturity of company deposits under the FX-protected deposit scheme down to one month and the removal of the interest rate cap in the Treasury-supported FX-protected deposits. In this environment, the CBT is likely to maintain its control over locals' FX flows to sustain low rates.

More By This Author:

China’s PMIs Show Growing Risk From Slowing External DemandOPEC+ Shocks Market With Supply Cuts

FX Daily: OPEC+ Output Cut Gives Dollar A Lifeline

Comments

Log in or sign up to join the conversation.