Image Source: Pexels

What central banks can learn from a wild week in markets?

Life comes at you fast if you're a central banker; think Noah Lyles in the Olympics' 100-metre final. Talk of emergency rate cuts, 50 basis point moves, and an imminent US recession? None of that was presumably on the Fed’s bingo card at its July policy meeting just nine days ago.

Has Jerome Powell been caught in the blocks? The Fed Chair has, of course, seen his fair share of market turmoil. And I suspect the mood in Fed Towers is not one of panic. A rogue US jobs market may have been the catalyst for what’s unfolded in financial markets, but what’s followed says as much about crowded positioning and low summer liquidity as it does about genuine macro fears.

Higher volatility isn’t necessarily a concern for the central bankers unless it exposes pockets of leverage that prompt a doom loop of issues in the financial system. So far that doesn’t seem to be happening. And even if it did, policymakers are adept at creating bespoke schemes to contain fires as and when they emerge.

That’s all well and good, but it doesn’t mean there aren’t lessons for the central banks from this week’s shenanigans. And here are four reasons why officials should avoid becoming complacent:

Firstly, it’s not obvious that the current bout of instability is fully behind us. Our Rates Strategy team describes the Treasury market as “rudderless”.

Investors are hungrier than ever for clarity on the US macro story, but the reality is they’ve been trading in a void of information. Data like jobless claims, a number that frankly is nothing more than noise in the short term, has attracted far more attention than it deserves.

That means Powell’s appearance at the Fed’s Jackson Hole conference in a couple of weeks will be pivotal. And it also means that next week’s US inflation data is going to attract even more eyeballs than usual. The story has been much better recently, and with the jobs market on the turn, the Fed is telling us that it is inclined to put less focus on its inflation mandate than it was just a few months ago.

But here’s the thing: the data has a habit of ignoring “the narrative”. An upside upset on inflation isn’t our base case, but our US expert James Knightley warns that it is possible.

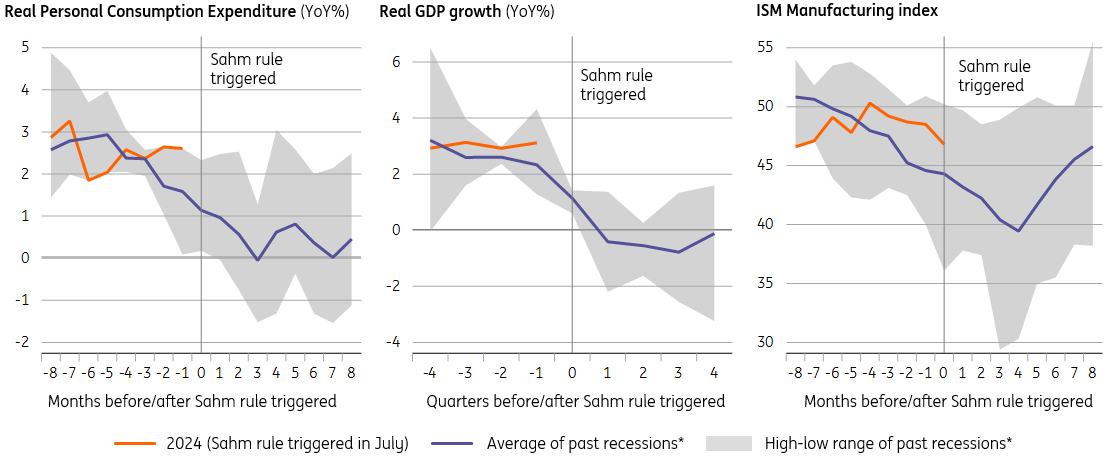

Second, there’s the jobs market itself. At least some of the bonkers market moves can be traced back to the triggering of the “Sahm rule”, which shows that recession has always ensued when the three-month moving average of the unemployment rate goes half a percent above its low in the prior 12 months. And as of last Friday’s data, that’s now the case.

Powell argues that much of this is explained by a rise in worker supply as opposed to increased layoffs. James K agrees, but more importantly, he warns that the situation can change quickly. The Fed’s Christopher Waller has said in the past that a rise in joblessness could become more apparent once the vacancy rate falls back below pre-Covid levels. And we’re very close to that point right now. Slow rises in the unemployment rate have a habit of turning more rapid as the economy flirts with recession.

Third, officials should be wary of drawing too many conclusions from other macro data that, for now at least, looks perfectly OK. The healthy rebound in the services ISM index this week is a good example. But take a look at previous recessions, and you'll find that the more serious slowdown in GDP growth and consumer spending tends to come after and not before the Sahm rule has been triggered – see the charts below. James K has, for some time now, been highlighting the mounting stress among US consumers, particularly at the lower end of the income scale.

Remember, too, that the recent strength in US activity is in no small part because interest rate hikes have hit the economy much more slowly than they did in the past. That’s down to long-dated mortgage fixes and more prevalent interest rate hedging at American corporations.

So here’s my fourth point: if the economy is more insulated from rate hikes, then exactly the same is true of rate cuts. If the jobs market really does start to weaken, then there’s not a huge amount the Fed can do about it in the short term.

That’s a lot to think about over in Washington, so let me leave you with our latest ING forecasts, which are out today.

James Knightley now forecasts a 50 basis point rate cut from the Fed in September, and he thinks that could easily happen again later in the year. For now, he’s projecting 100 basis points of cuts in total for the remainder of this year and another 100 next year.

After months of just sitting in the stands, the race is now on for Mr Powell.

Chart of the week: Weaker growth and spending tends to come after, not before, the Sahm rule is triggered

*Based on Sahm rule triggers points in 1980, 1981, 1990, 2001 and 2008. 2020 excluded given it wasn't a typical recession.

Source: Macrobond, ING calculations

THINK Ahead for Developed Markets

United States (James Knightley)

- Inflation (Wed): Volatility in financial markets is likely to remain elevated given the all-important inflation data that is out this week. The past two months have seen both the core CPI and the core PCE deflator come in at the MoM% run rate required, over time, to bring annual inflation back to the 2% target, but the Fed needs to see more of this to be confident it can cut rates. We believe we will see that again this week with another 0.2% core CPI print likely, especially given evidence that housing costs within CPI are finally catching up with what private rent surveys have been saying for the past year.

United Kingdom (James Smith)

- Jobs report (Tue): Much like the US, the UK jobs market is cooling more noticeably now, though issues with the data mean its hard to know how seriously to treat the recent rise in unemployment. But for what it's worth we think the jobless rate will rise again next week.

- Inflation (Wed): Services inflation has been stickier than expected recently, though as the Bank of England has acknowledged, a lot of this is down to noise and backward-looking price hikes at the start of the financial year. We expect more progress here next week, and that should keep the door open for one, more likely two rate cuts later this year.

- GDP growth (Thu): The UK economy has surprised pretty much everyone so far this year, and data already available for April and May suggest second quarter GDP will be almost as good as it was in the first quarter. We suspect growth will slow to more 'normal' rates as the year goes on, but the question is to what degree that rise in unemployment filters through to slower activity as we enter 2025.

Norway (James Smith)

- Norges Bank (Thu): Norway stands out as a relative hawk in the G10 space, having signalled that it plans to keep rates on hold for the remainder of this year. Recent NOK weakness is only likely to have reinforced that view. But inflation is trending a bit below forecasts and assuming the Fed does cut rates aggressively from September, then we think Norges Bank will ultimately deliver at least one rate cut before the year is out.

THINK Ahead for Central and Eastern Europe

Poland (Adam Antoniak)

- Current account (Tue): We forecast a current account surplus of €793m in June, aided by small surplus in trade in goods and a narrower deficit in primary income amid weaker profitability of foreign enterprises. Still, the cumulative 12-month current account surplus probably eased to about 1.4% of GDP from 1.8% of GDP after May as the trade surplus this year was lower than in June last year. According to our estimates, imports were stagnant as upward pressure from imported energy abated and demand from domestic investment was poor. Exports likely contracted (-4.4% year-on-year in €) amid weakness in external demand.

- GDP (Wed): This should confirm that a continued economic recovery is underway, with industrial output posting positive annual growth following five quarters of declines, a more moderate drop in construction output and only a slight drop in retail sales versus the first quarter. GDP growth of 2.8% YoY is slightly below earlier projections given somewhat weaker consumer demand. We still expect 3.0% economic growth for 2024 as a whole, but downside risks are mounting.

- CPI (Wed): The flash estimate of 4.2% YoY is likely to be confirmed. Even though the removal of the energy shield had less of an impact than feared, the details are likely to show this was not the only factor driving inflation. The lowest annual increases in food prices are already behind us and core prices remain sticky, especially in the service sector that accounts for roughly 50% of core inflation.

- Core inflation (Fri): Our initial estimates suggest that core inflation increased to 3.7% YoY in July from 3.6% YoY in June, confirming that a tight labour market and robust wage growth make it difficult to reduce upward pressure stemming from services prices.

Czech Republic (David Havrlant)

- Consumer inflation (Mon): Headline inflation likely remained unchanged at the 2% target in July. Meanwhile, the monthly move in headline and core inflation was rather pronounced due to seasonal factors, namely the upward price effect of packaged holidays. We also expect a monthly increase in fuel prices, which aligns with higher Brent crude prices and weaker CZK/USD in June and July. Food prices likely dropped further from a month earlier, yet seasonality in this item can change patterns rather easily. There is some downward risk for regulated prices in July, as the large energy distributors have been reducing end prices for customers. However, the magnitude of this effect is challenging to estimate due to the lack of accuracy regarding the shares of customers with floating contracts. Monetary policy remains restrictive after the modest 25bp cut in early August, and the deteriorating prospects for a solid recovery present a downward risk to the future trajectory of consumer prices.

- Producer inflation (Fri): Continued industrial weakness was likely seen in producer prices, which are expected to hover just above 1% YoY in July. The subdued pricing in industry points to low supply-side inflation pressures for the months and quarters ahead. The current account also likely deteriorated in June, as foreign demand remained sluggish and did not provide robust support to exports.

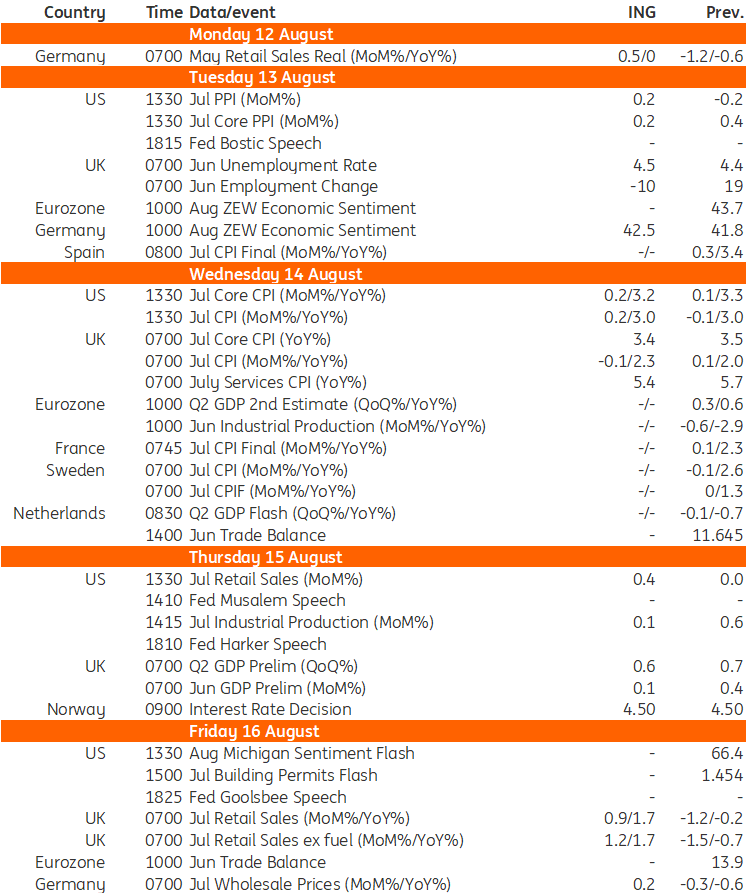

Key events in developed markets next week

Source: Refinitiv, ING

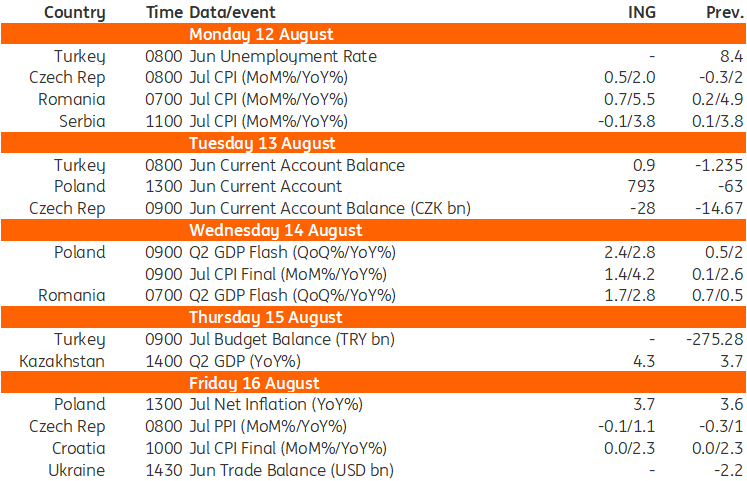

Key events in EMEA next week

Source: Refinitiv, ING

More By This Author:

Asia Week Ahead: China’s Economic Data, Japan’s GDP And India’s CPI And Trade FiguresGold Monthly: Rally Might Not Be Over Just Yet

China’s CPI Inflation Rebounded Due To A Smaller Drag From Food Prices

Comments

Log in or sign up to join the conversation.