The US dollar pulled back, and long-term yields softened last week, but the economic surge has only just begun. The more than 900k rise last month's non-farm payrolls and the jump in auto sales will set the tone for this month's economic data, and investors will get a taste of it next week. The US data will be robust in absolute terms but also relative to other countries.

France and Spain have already revised their growth forecasts this year, and Bundesbank President Weidmann hinted that it may do the same for Germany. The market has written off Q1 and probably Q2 as well.

Singapore is the first to report Q1 GDP. It is expected to have expanded by around 1% after growing 3.8% in Q4 20. It would be the slowest paces since the contraction in the first two quarters of last year. China will be the first of the large countries to report. The world's second-largest economy appears to have slowed by half or more in Q1 after a 2.6% quarter-over-quarter pace in Q4 20. March trade figures are due before the GDP figures, but other March data, including retail sales, industrial production, and fixed-asset investment, are released simultaneously.

The key question is, what happens next? China has taken measures, including discouraging loan growth (which will not be evident in the March lending figures) and other actions that could have a cooling-off effect on entrepreneurship. Can China find its mojo? The IMF apparently thinks so as it revised its projection for Chinese growth this year to 8.4% from 8.1% made three months ago, and said that China's economy will generate 20% of the world's growth in the five-year period beginning this year.

The IMF has caught up to market forecasts, but this year's growth is an aberration, and economists expect China's growth in 2022 and 2023 to fall below 6%. As the shift from rural to the city is well advanced and the productivity catch-up gains largely captured, the growth impulse has slowed. With two exceptions (2010 and 2017), Chinese growth has been slowing every year since 2007. This year is an anomaly in the opposite direction of last year's, but the average over the two years is probably close to the new normal.

The IMF also boosted its projection for US growth this year to 6.4%, up from the 5.1% estimate in January. It optimistically anticipates 4.4% growth in 2022, a third faster than Fed officials' median projection. Private-sector economists seem to be closer to the IMF's assessment for next year than the Fed's. This may help explain why the market has fully priced a rate hike more than a year before the median Fed forecast in March despite the official statements.

The macro story that will dominate next week is the surge in US economic activity in March and a jump in headline CPI above 2%. On the one hand, everyone recognizes that US growth is accelerating. On the other hand, the pace, like we saw with the employment report, may surprise economists. The data will not just appear strong, followed by some weather-induced weakness in February. It will be eye-popping in absolute terms, quantifying the surge driven by the massive fiscal and monetary stimulus, the wealth effect of rising equity and real estate prices (and crypto, judging from what is happening in the art world).

March CPI will be reported on April 13, and the base effect will kick in. Headline CPI is expected to rise by 0.4%-0.5% in the month. That would put the Q1 annualized rate over 4% in its own right, but the year-over-year rate will be flattered by the fact that last March CPI fell by 0.3%. The peak of the base effect is happening this month. In April 2020, CPI fell by 0.7%. March's year-over-year rate will jump toward 2.5% from 1.7% in February and further in April.

The core is going to show a milder base effect. In March 2020, it was flat and fell by 0.4% in April. This year core prices were flat in January and rose by 0.1% in February. A 0.2% increase is expected in next week's report. A 0.1% monthly average is the same as in Q4 20. Still, the core rate on a year-over-year basis is likely to return to the upper end of the H2 20 pace around 1.6%-1.7%.

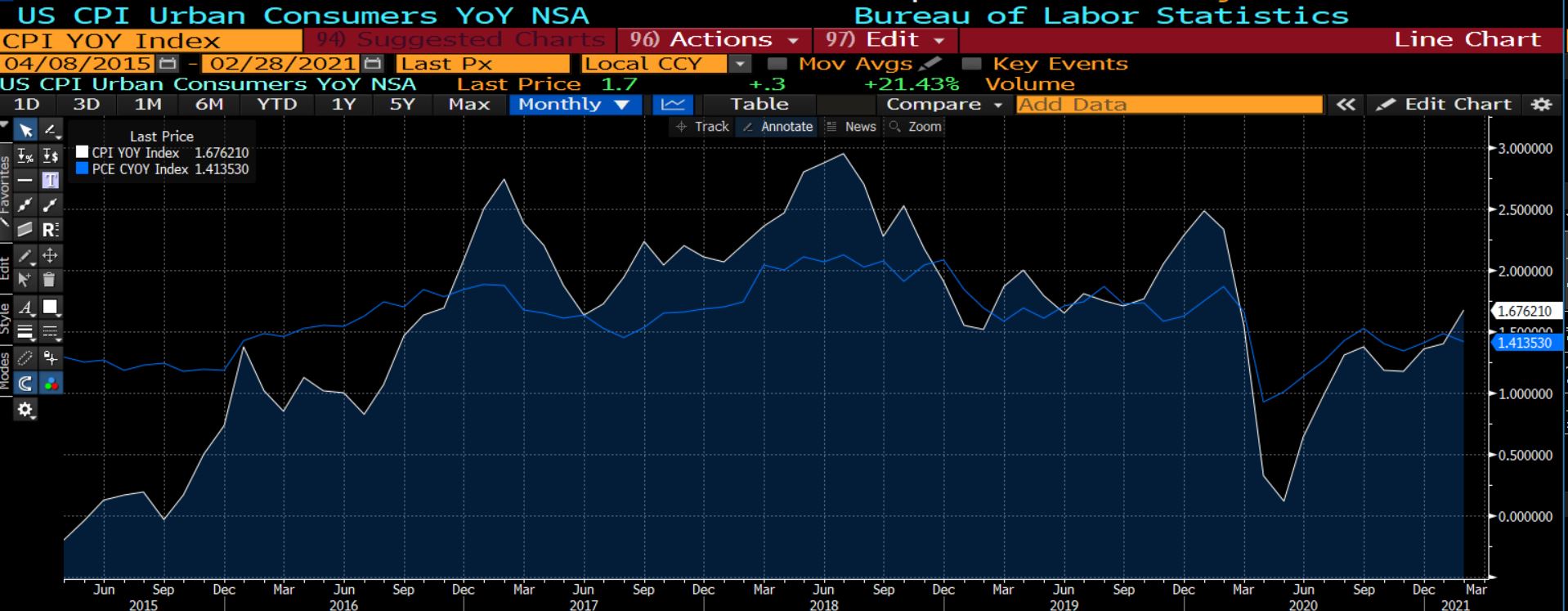

Remember, the Fed targets the headline PCE deflator, though it talks about the core rate. The March readings are not due until the end of April. Here, the Bloomberg chart shows the headline CPI (white line) and headline PCE deflator (blue line). The latter is more stable than the former. The PCE deflator tends to run below CPI, but there are exceptions. Fed officials say they will look through the base effect boost in inflation. The Fed is preserving its strategic ambiguity and has yet to define the look-back period for calculating the average rate of inflation.

Real sector data for March will surge. The much stronger than expected auto sales suggest a jump in retail sales, which account for a bit more than 40% of overall personal consumption expenditures. Core retail sales, which exclude auto, gasoline, building materials, and food services, are expected to soar by 5.5%, says the Bloomberg survey's median forecast, helped by the second check from the federal government in the past four months.

Less than an hour after the retail sales report, March industrial output figures will be released. A rise of almost 3% is expected after a 2.2% decline in March. It may be the strongest since last July. The shortage of semiconductor chips could begin stunting the recovery of auto production. GM, for example, announced last week it was reducing more production at North American plants due to the lack of sufficient chips. It warned that this bottleneck could shave operating profits this year by $1.5-$2.0 bln. Ford also indicated it would be idling more plants but is planning on making it up in the summer.

Meanwhile, and few in the American press are drawing the connection, but US sanctions against Huawei (the largest Chinese consumer of chips) and SMIC (China's leading chip manufacturer) exacerbates the industry strains. Export controls were imposed last week on three other Chinese semiconductor firms (seven entities in all) for helping develop a supercomputer in China that has military as well as civilian applications. The Biden administration hosts a public/private summit on the chip shortage at the start of the new week. As TSMC and Intel have shown, even if for different reasons, staying at the cutting edge of chip fabrication is not a one-time expense but a heavy and continuous significant investment.

Capacity utilization rates are expected to jump after the weather-induced decline in February. The utilization rate, which fell to almost 64% last April and May, has seen a V-shaped recovery. The capacity utilization rate peaked in January at 75.4% and is expected to make a new post-crash high in March. Bloomberg's survey median forecast is for it to rise to 75.7%. The 10- and 20-year average rates converge around 76.5%. It raises questions about the ability to invest the $2.8 trillion of stimulus that has been approved in December 2020 and March 2021. If not, rising prices will allocate the scarcity.

The week's real sector data reports will conclude on April 16 with a jump in housing starts. Of course, starts were initially paralyzed in the early days of the pandemic and collapsed to five-year lows last April but surged in the remainder of the year and finished 2020 at a seasonally adjusted annual rate of 1.67 mln, the strongest since 2006. Starts fell by more than 15% in the first two months of the year, mostly due to abysmal weather. That pushed February starts to a 1.42 mln unit pace, the slowest since last August. The median forecast (Bloomberg survey) calls for a nearly 14% increase. Such an increase would lift March starts to a 1.61 mln unit pace, which would be the second-best since last year's trough behind December.

The market reaction to the news will be an important reflection of psychology and position. The dollar edged only a little higher after the stronger than expected employment data. While the 10-year yield rose, it gave it all back and more in the sessions that followed. There has been a pullback in the dollar and yields that suggest positioning was also adjusted, at least on the margins. Also, after a couple weeks' hiatus, the US Treasury is selling $110 bln of coupons next week. If the dollar cannot rally or yields do not rise, more participants may conclude that the divergence theme has been fully discounted.

Comments

Log in or sign up to join the conversation.