The Lacklustre Take-Up, So Far, Of Europe’s Multi-Billion Rescue Fund

The EU's Recovery and Resilience facility is meant to help European economies recover from the Covid-19 crisis. The fund will serve more as a medium-term boost to growth than a crisis-fighting tool. That said, digitalisation and the greening of mobility, energy and real estate stand to gain significant investment so boosting overall GDP growth.

European Commission President, Ursula von der Leyen

Not all countries too eager to pick up a free lunch

It's the facility that's meant to help European countries recover from the Covid-19 crisis. €672.5bn of grants and loans are available and countries have been submitting their plans. But that take-up, at least so far is modest at best. Only 14 out of a possible 27 proposals have come in. Like you would do when hosting an unsuccessful party, you extend the deadline for applications a bit to make sure you fill the room. That’s what the Commission has done as it has made the deadline flexible.

Some countries have already announced they will not participate for now, while others struggle to make proposals up to the Commission’s standards. For now, let’s take a look at what has already come in. And we're limiting ourselves to the investments and will leave the reform proposals for another time.

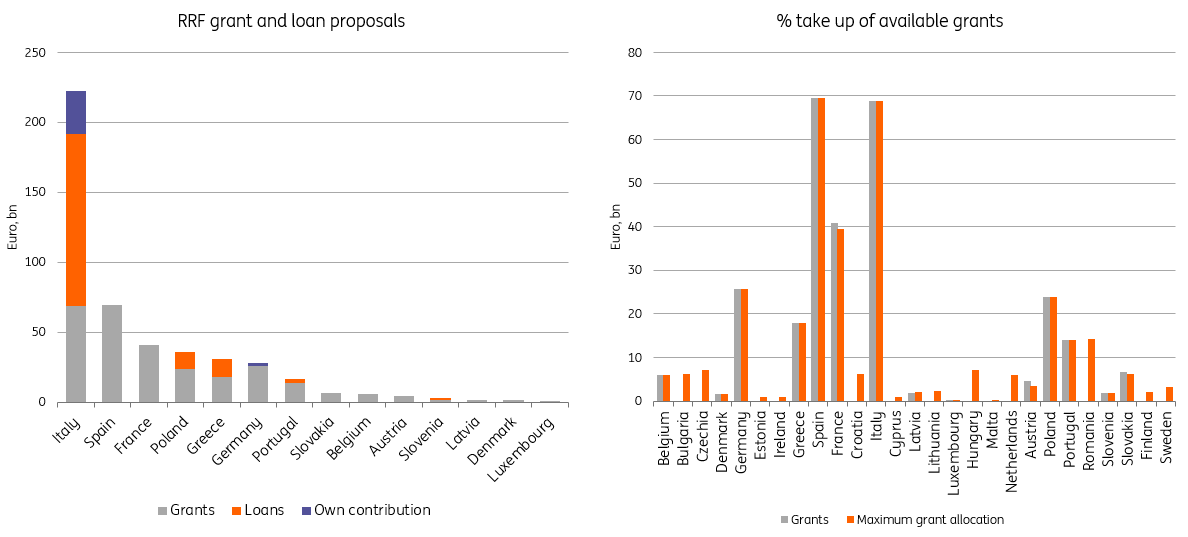

It's important to say that the countries which haven't put proposals in so far have smaller maximum grants to receive from the fund. About 84% of the available grants have been applied for because the countries that stand to gain the most from the fund have already applied. The only country that is set to receive more than €10bn that hasn’t submitted a proposal so far is Romania. For the eurozone economy, the biggest one not tapping funds for the moment is the Netherlands at €6bn. Still, with very few countries opting for loans, the total amount of proposals comes in at ‘just’ €433bn, well shy of the total of €672.5bn in the facility.

As you can see from the chart below, it's obvious that Italy has gone big and bold with its proposal. Not only have they applied for the maximum amount of grants available to them, but they have also gone for an even larger amount in loans and add their own contribution to the plans on top (mind you, the proposal also includes a small amount coming from the recovery funds smaller cousin REACT-EU). That makes the amount for Italy - if approved – about 44% of the total money demanded so far.

But don’t count out Spain’s fiscal efforts either. While Italy’s plans spread out over the total period of 2021-2026, Spain’s plans are set to take effect in the first three years only, making the impact on GDP in the first recovery phase large.

Italy has applied for the largest sum from the facility; most grants have now been applied for

(Click on image to enlarge)

Source: European Commission, National Recovery and Resilience Proposals, ING Research Note: some country data – like Italy - also includes the funds requested from the REACT-EU part of the NextGeneration EU

The plan still leaves eurozone Covid-19 fiscal efforts at less than half of the US

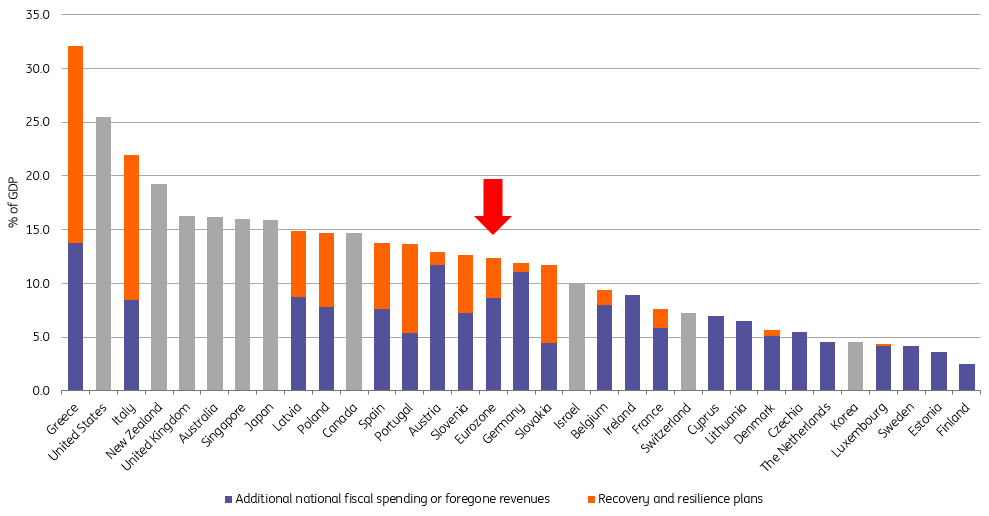

The impact of the plan is definitely sizeable, although the amount applied for is well shy of the total available in the facility. At €433bn, it has to be said that the impact will spread out over the full period 2021-2026 for almost all countries. That makes the fiscal impact of the programme for the initial recovery phase somewhat underwhelming.

Looking at the additional fiscal spending that countries have done or promised to do in response to Covid-19, the US stands out with a whopping 25.5% of GDP. This includes the approved proposal for the American Rescue Plan, but not the new proposals put forward by President Biden which have yet to find approval in Congress. The eurozone comes in at just 12.4% of GDP when adding the Recovery and Resilience Proposal to national fiscal spending to fight the pandemic. This might even overstate the total amount as there may be some double-counting in projects originally planned to be nationally financed that are now included in the national RRP.

Additional fiscal spending in response to the Covid-19 crisis gets a sizeable boost from the RRF in some countries

(Click on image to enlarge)

Source: IMF database of fiscal policy responses to Covid-19, National Recovery and Resilience Proposals, ING Research

Note: possible double-counting due to projects initially nationally-funded now included in RRPs. France has been corrected for double-counting as total spending funded from RRF is part of previous proposals.

Of course, it is more relevant to look at the fiscal impulse for individual countries as the facility was designed to help the states most in need. Given the sizeable loans that countries like Greece and Italy have taken out, these countries do move to the global frontrunners in terms of fiscal spending in response to Covid-19. Greece even surpasses the US at 32.1% of GDP, but the impact could be significantly smaller as the lending part of the Greek proposal is reserved for the partial funding of private investment so the takeup is non guaranteed.

Italy stands at 21.9% of GDP, also very high on the list. Overall it is important to keep the possible double counting caveat in mind (RRF funding for originally nationally-funded proposals) for the exact number though, view this as an upper estimate. It is also important to keep in mind the time span, as US support agreed on so far has a far larger immediate impact than the Italian and Greek Recovery and Resilience Proposals. Spain and Portugal also rank high thanks to the recovery fund proposals but do remain well below countries such as the UK, Australia and Japan.

As Spain and Portugal have weak automatic stabilisers, this is of concern from a crisis response perspective. That shows that while the project helps significantly in terms of fiscal support, it is still unlikely to cause the harder hit eurozone economies to recover quicker than their northern eurozone partners as we have extensively written about here. The big wins are for the medium term as investment and reforms have the potential to improve trend growth, which has been a clear eurozone problem since the global financial crisis.

How to spend it, the eurozone version

The Commission has put a strong directive on how to invest the funds in the rules around the Recovery and Resilience Facility:

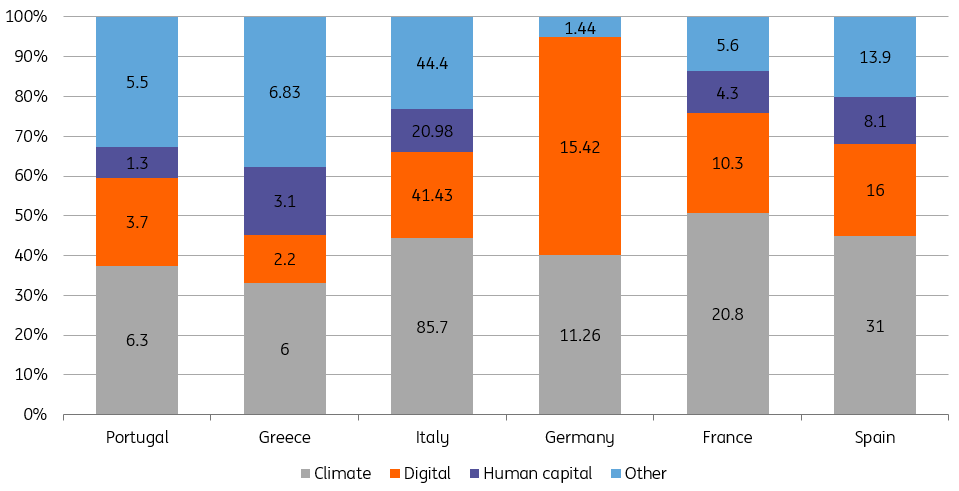

- At least 37% has to be directed to climate investments and reforms and 20% to foster the digital transition.

- All large economies meet these targets set with most going well above it - according to their own assessment, whether the Commission agrees is another matter.

- The German plan even indicates that more than 50% of the plans count towards digital transition.

Most countries have indicated spending more than 40% of their funds on climate investments and reforms with Belgium and France spending over half.

To get a sense of the focus of the larger countries we look at the six largest eurozone RRPs, which come from Italy, Spain, France, Greece, Germany and Portugal. Those are the only ones over 15bn euro and represent 95% of the total eurozone proposals. Comparisons are tough given different classifications and reporting of projects between countries, but we have drafted some rough categories to see where most spending will be done.

The main focus of RRF spending differs between the big spenders

(Click on image to enlarge)

Source: National Recovery and Resilience Proposals, ING Research

As we've just mentioned, climate spending takes the crown in the project with €16bn earmarked for investment under green transition-related projects. Even though Italy has a rather balanced proposal, its total size still makes it contribute to more than half of the specific climate-related proposals. Digital is most important in Germany, with a majority of investments going to digitalisation.

Greece and Portugal have very balanced programmes with a lot of spending on other types of projects. Greece also heavily banks on human capital related investment, about 17% of the total as skills and employment have been key factors in which Greece has lagged since the Global Financial Crisis.

Green energy, real estate and mobility take the cake

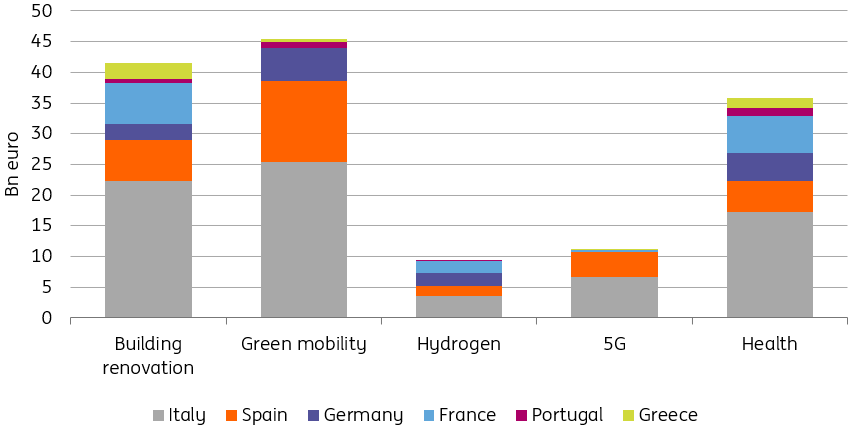

When looking at specific factors, a few things stand out. The climate projects are mainly driven around the themes of green energy, real estate and mobility. The greening of real estate has been a focal point of the green transition for quite some time and this marks a large investment effort of no less than €41.5bn for the six countries examined. Greener transportation also ranks very high with about €45bn in investments planned.

Think of investments in cleaner public transportation but also in electric car charge points. Within the clean energy theme, investments in hydrogen as a clean energy source are interesting to note, with investments amounting to around €10bn set to be done.

Selected investment themes and earmarked spending show potential for green investments

(Click on image to enlarge)

Source: National Recovery and Resilience Proposals, ING Research

Other projects that stand out are investments in digital modernisation, which leads to sizeable 5G rollout investments that add up to over €10bn. Spain and Italy, in particular, tend to invest significantly in 5G projects, which makes sense given the generally weaker digital infrastructure compared to some of the larger northern eurozone economies. Finally, health care is also important to mention and directly related to the Covid-19 crisis. All countries have devoted RRF investments to the sector, amounting to €36bn in total.

Where does the project go from here?

A few key things are on the agenda at the moment. First of all, the Commission still eagerly awaits other countries to still join the party. When other proposals can be expected to come in remains unclear, but we do expect some to trickle in over the coming weeks. The EC will then review the proposals within two months of receipt. One month after the Commission agreement, the Council will have to approve the plans as well. When agreed, the countries will receive 13% as an early payout to get projects going, which should be the case in July. That means that money can start flowing in the third quarter of this year.

Before that can happen though, countries will still need to ratify the Own Resources Decision. This establishes how the EU budget and RRF is funded, so without those approvals, the recovery fund is in jeopardy. This has not been done by all countries as of yet; mainly northern and eastern European countries still have to ratify. While this is a hotly contested decision in some countries like Germany and Finland, it does look like all countries are moving towards ratification before the end of June. That means that we don’t expect major hiccups in the process for the RRF at this point and that the historical project can kick off later in the summer.

Disclaimer: This publication has been prepared by the Economic and Financial Analysis Division of ING Bank N.V. (“ING”) solely for information purposes without regard to any ...

more