The Japan Post IPO - Now That’s A Ponzi!

The global financial Ponzi gets crazier by the day, and more often than not the mad men who run Japan Inc. are front and center. But even Japan’s whacko Prime Minister, Shinzo Abe, has outdone himself with the Japan Post Holdings IPO.

We could start with the fact that after trading up roughly 25% from the offer price in an apparent fit of patriotic mania, the holding company and its two subsidiaries were valued at $140 billion. Needless to say, that sporty valuation was not owing to the fact that Japan’s 24,000 unit postal savings system has experienced a sudden spurt of growth.

In fact, revenue has been falling for years, and net profits have been nothing to write home about. Indeed, the group’s offering release indicated an expectation that the net income of Japan Post Holdings would drop 23% to 370 billion yen in the year ending next March 31.

Stated differently, Abe & Co have foisted on Japan’s retail public, which got upwards of 75% of the shares sold this week, the vastly inflated stock of a dying public bureaucracy which by its own admission is now “earning” 33% less than it did in FY 2013.

And this wouldn’t be the first time.Back at the height of the dotcom bubble, the Japanese government sold the retail public 2.1 trillion yen ($18 billion) worth of shares in Japan’s wireless telecom services provider (NTT DoCoMo). In perhaps a foreshadowing of what comes next, the company’s implied total market cap of $220 billion at the time now stands at just $78 billion. That is, about $140 billion of bottled air was peddled to the Japanese citizenry.

Despite its insane overvaluation, at least DoCoMo was in an industry with a future. By contrast, the principle asset of Post Holdings is the Japan Post Bank, which is a relic of the Meiji Restoration created 1875.Needless to say, its millions of Japanese depositors are almost entirely over 65, and its President is an ex-BOJ bureaucrat who is, befittingly, 79 years old.

Nevertheless, the Post Bank alone was valued at $60 billion at the close of the first day of trading, representing 20X its most recent year net income of about $3 billion. But it’s no Goldman Sachs or even Citigroup. In fact, the Post Bank’s financial statement is a testament to the depredations of ZIRP, as it has been practiced in Japan for nearly two decades.

To wit, nearly 70% of the Post Bank’s $1.8 trillion of assets reported for FY 2014 were invested in Japanese government debt——from which it earned the grand sum of 93 basis points. So how could a “bank” which doesn’t even invest in home mortgages—-to say nothing of high yield loans or proprietary trading in debt, currencies and commodities—-possibly earn $3 billion on Japanese government bonds?

Simple. Pay the long-suffering householders of Japan a microscopic 14 basis points of interest on their $1.5 trillion of deposits in the Post Bank and collect the spread. As a mathematical matter, of course, that did produce an enviable net interest margin. In FY 2014, the Post Bank booked $17 billion of interest income compared to only $3 billion of interest expense.

But here’s the giant snag. The Keynesian geniuses who run Japan Inc. are literally driving the yield on the nation’s towering pile of public debt toward absolute zero.As a result of the BOJ’s massive $70 billion per month QE campaign, the central bank is providing a nearly endless bid for Japanese government bonds, and has now driven the 10-year yield to just 31 basis points, the 5-year to 5 basis points and the two year bond yield to zero!

So it was only a matter of time before the Post Bank’s earnings on its $1.1 trillion of government bonds would shrink to the vanishing point. Accordingly, its net interest margin would disappear entirely—even if it reduced its deposit rate to zero. And that’s not the half of it.

Japan’s population is aging so rapidly that its primary customer base is in a liquidation mode. That is, before Japan’s elderly households check-out entirely, the will liquidate most of the $1.5 trillion in deposits now lodged in the Post Bank.

This all amounts to what Wall Street might call a problem with the “business model”. That is, the customer deposit base will be shrinking and the net interest margin on what remains will be heading toward the zero bound as the portfolio of Japanese government debt turns over.

Needless to say, that’s not exactly a 20X valuation opportunity in most parts of the known universe. But Professor Krugman’s disciples in Japan operate on a completely different economic logic.

In truth, Japan is an old age colony heading for bankruptcy. It should be running large budget surpluses before its demographic time bomb totally overwhelms its fiscal capacity. But Abenomics assumes that it can borrow and print it way to economic salvation and is therefore driving the whole system toward a financial armeggedon.

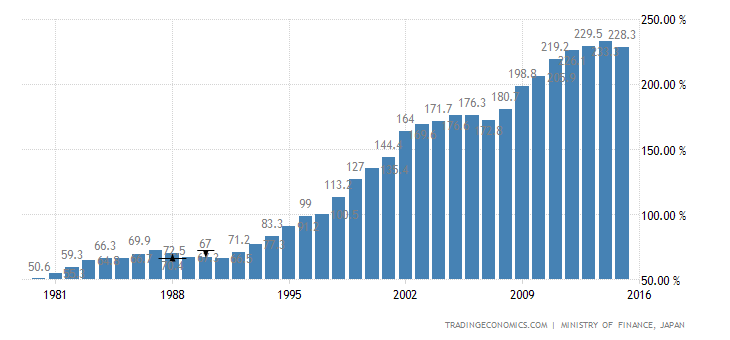

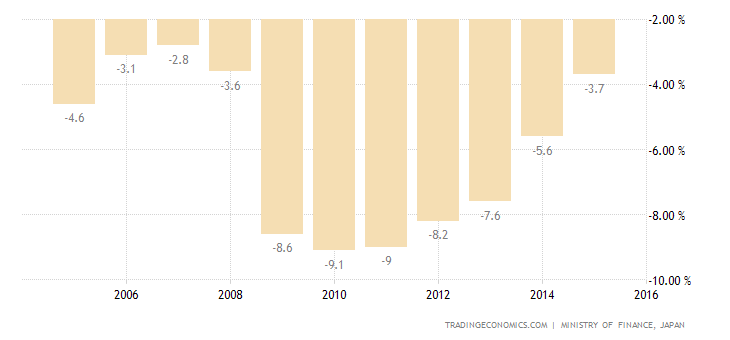

With its public debt at 230% of GDP and the budget deficit still at the highest rates relative to GDP in the developed world, Japan literally can not afford to pay interest on government bonds—-even though paying near-ZIRP is a huge problem for its millions of aging households whose savings are trapped in the Post Bank.

So, as I said at the beginning, Prime Minister Abe has resorted to a scheme of financial prestidigitation that would make Houdini envious.

Does Japan’s retired population need a better return on its $1.5 trillion of savings? No problem.

Does the BOJ need more government debt to buy in order to continue its massive money printing campaign? Same solution.

To wit, encourage Japan’s savers to buy shares in the Post Bank IPO. The latter has advertised that it will pay a 3% dividend yield, which is a pretty snazzy step-up from 14 basis points of yield on postal savings account.

At the same time, mandate the Post Bank to sell its government bonds to the BOJ and replace them with higher yielding alternatives, including foreign debt and equities.

As one research report described it,

If the situation justifies it, the fund would expand its business horizon and consider real estate investment trusts, private equity and project finance deals. Currently the bank’s investment division is staffed by just 100 people.

“We have to refine our investment,” said Mr Nagato, who has stamped the brand “superglobal” on the bank’s new growth strategy and begun a programme of poaching investment professionals from outside. He has nicknamed the first such wave of newly hired investment professionals — who include the former vice-chairman of Goldman Sachs Japan — as his “magnificent seven samurai”. He plans to expand their number to about 30 over coming months.

There you have it. The clueless bureaucrats who run Japan’s post office are going to put on some man pants and plunge straight away into the casinos of Wall Street, London and Tokyo. And just in time for the third central bank created financial bubble of this century to come crashing down all around them.

Needless to say, the odds that the Japan Post Bank will be worth $60 billion after its is introduced to the world of “risk assets” by Goldman Sachs and its like and sundry competitors is somewhere between slim and none. Japan’s savers are heading for another deep fleece.

At the same time, it is virtually certain that the yen will not trade the current rate of 120 to the dollar, but at 220 or even lower, after the BOJ finally buys up the last available JGBs, including the $1.1 trillion currently owned by the Post Bank.

That is to say, the retirement colony on the Japanese archipelago is utterly dependent upon imported energy, industrial raw materials and foodstuffs. So when all is said and done the cost of living there is going to soar, even as Japan’s hoard of retirement savings is depleted by time and deflated by “risk asset” investments gone bad.

Worse still, Shinzo Abe and his merry band of lunatics are dressing all this up as part of the “reform” leg of their economic recovery tripod.

Only in a world gone mad is it possible to contend that turning over the lifetime savings of a nation to the likes of Goldman Sachs is a “reform”; or that having the central bank buy up 100% of the public debt is a route to recovery and growth; and, most especially, that putting Japan’s long-suffering household savers into the massively inflated stock of a dying public bureaucracy is not, in fact, tantamount to a criminal act of state.

Disclosure: None.