The Bank Of England’s Jobs Dilemma In Four Charts

The Bank of England is no longer forecasting any real increase in UK unemployment later this year, even as wage support comes to an end. We think this may prove optimistic, and instead, we think we could see an increase in the jobless rate to around 5.5% - though clearly, this is still much lower than predictions made only a few months ago.

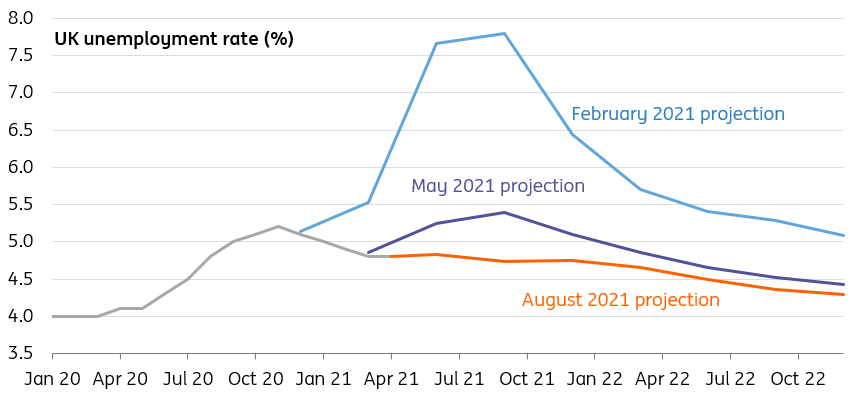

The Bank of England is no longer predicting a big rise in unemployment

There was plenty to digest at last week’s Bank of England meeting. Policymakers formally acknowledged some tightening is likely over the next couple of years – and indeed confirmed that some of that will be delivered by reducing the size of the balance sheet.

And while the BoE didn’t formally put any kind of date on when the first move might come, its latest forecasts effectively endorsed the market’s view that a rate rise could happen later into 2022.

Clearly, there’s a lot of uncertainty beneath that – and one thing that really stands out in the Bank’s latest forecasts is that it no longer expects any material spike in unemployment once the furlough scheme is withdrawn on 30 September. That’s quite a contrast from February when the Bank expected the jobless rate to spike to almost 8% later this year (the current rate sits at 4.8%).

Much of this change in view is underpinned by the fact that wage support has been extended until well after most firms were able to reopen in April or May. This gives most companies space to rebuild, and a better chance of bringing most or all staff back.

Bank of England's unemployment forecasts from recent meetings

Source: Bank of England, Macrobond, ING

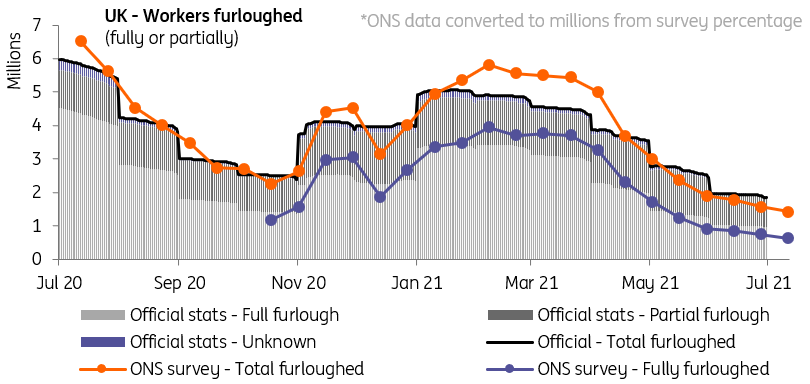

But while that means the spike in joblessness will be much less severe than it might have otherwise been, we think an increase still looks more likely than not. In contrast to the headlines of staff shortages, the number of furloughed employees has stayed surprisingly elevated, despite the vibrant economic recovery through the spring. Some 1.8 million workers – 6.5% of the total - were still receiving government wage support at the end of June, with a little over half still furloughed for all of their hours.

Admittedly, that’s below the previous low set last October, and the bi-weekly ONS survey of businesses suggests that’s fallen a touch further in July. Note too, that this data largely dates back to before 19 July, when the final restrictions were lifted.

The number of people on furlough has fallen more gradually than expected

Source: HMRC, ONS Business Insights and Impact on UK Economy survey, ING

But the presence of Covid-19 rules is not necessarily the only factor at play.

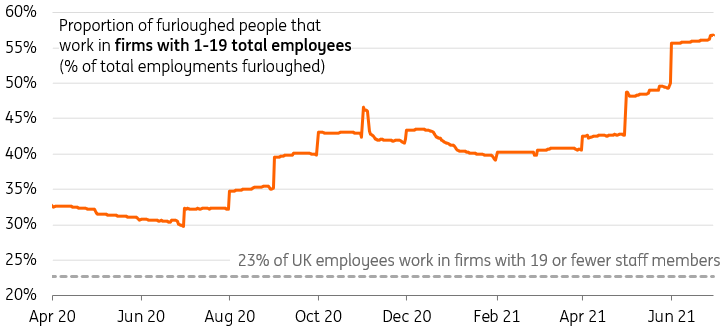

Indeed, one thing that stands out is that small businesses are now overwhelmingly the biggest users of the scheme. Over half of those furloughed work for a business with fewer than 20 employees, easily the highest percentage since the start of the pandemic.

It’s tempting to think that this may be because those sectors most heavily furloughing have higher concentrations of smaller businesses, but a quick comparison with official data on firm sizes across different industries suggests that’s not the case.

Instead, this trend hints that smaller businesses are more reluctant – or more likely perhaps, less able – to bring staff back from furlough than their larger counterparts.

Smaller businesses account for the majority of furloughed positions now

Source: HMRC, BEIS Business Population Estimates, ING calculations

It’s also worth noting that the scheme is now much less dominated by consumer services. And what’s interesting is that a range of sectors still have a non-negligible percentage of workers receiving wage support, and in many cases, the sizable majority are still on ‘full furlough’. For instance, 10% of construction workers were still receiving wage support in June – the vast majority for all of their normal hours - despite economic activity in the sector having recently returned to pre-virus levels.

To us, this suggests that a reasonable number of roles still furloughed may no longer be viable, and are at risk of redundancy as the scheme comes to an end.

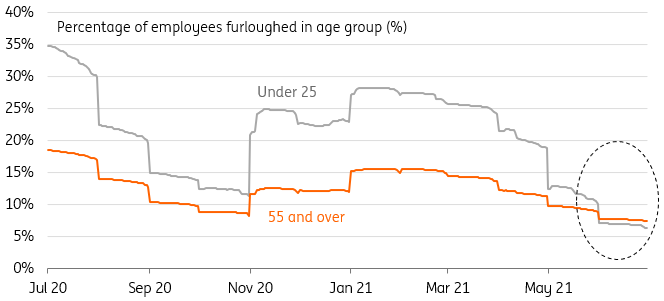

If that's the case, what happens to the unemployment rate will heavily depend on how the workers involved are re-classified in the data. Through 2020, roughly two-fifths of the fall in employment was accounted for by a rise inactivity – that is, individuals not actively looking for a new role. And what’s clear is that the education system helped absorb a number of young workers while hiring fell last year. The percentage of 18-24 year olds in full-time education rose by roughly one percentage point on pre-virus levels through the pandemic.

Older workers now more likely to be furloughed than people at the start of their careers

Source: HMRC, ING calculations

The unemployment rate could increase to 5.5% later this year, though the peak might not last long

This time, things may look slightly different. For the first time in the pandemic, it’s now more likely that those aged 55 or over will be on the furlough scheme than those 24 or younger. That suggests any rise in redundancies in the autumn risks affecting older workers more heavily. But when it comes to the official data, many may classify themselves as retired – even if this wasn’t necessarily out of choice.

So where might the unemployment rate land later this year? If we make a loose assumption that half of those ‘fully furloughed’ in June lose their job when the support ceases, and a similar proportion to last year reclassify as economically inactive (e.g. retired/study, etc), then that would roughly put the jobless rate around 5.5%.

Of course, context matters. Compared to predictions from a few months ago, an increase in unemployment is likely to be much less severe. And the considerable rebound in hiring appetite we've seen recently suggests any peak may not last long. Talk of staff shortages in consumer services (which account for the lion’s share of job losses through the pandemic so far) indicates that employment is likely to be quicker to rebound faster than past recessions.

Incidentally, the fact that staff shortages are coexisting with elevated furlough rates points to a degree of mismatch in the jobs market - something that will gradually, though certainly not fully, reduce in the months to come.

But taken together with the fact that inflation is likely to be much less exciting after a peak of around 3.5-4% later this year, a rise in unemployment would suggest the Bank of England is unlikely to rush into tightening in 2022.

For now, we’re penciling in a rate hike in early 2023.

Disclaimer: This publication has been prepared by the Economic and Financial Analysis Division of ING Bank N.V. (“ING”) solely for information purposes without regard to any ...

more