Services inflation has once again come in higher than expected. But some of this is down to noise and we doubt it will completely knock the Bank of England’s new-found confidence in its future inflation predictions. We’re still looking for the first rate cut in August.

For the first time since the spring of 2021, UK headline inflation is finally back to the 2% Bank of England target. It’s also a fall on April’s numbers, and we can point to areas like food, household goods and clothing which are all now contributing considerably less to inflation than just a few months ago.

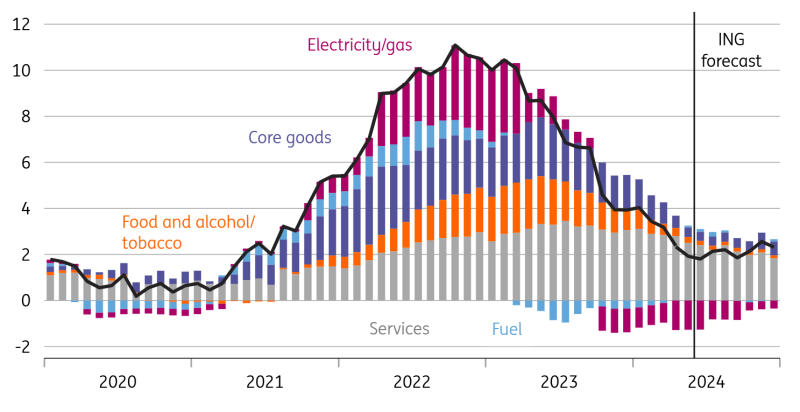

All of that is of course great news, but we think we’re probably towards the end of the disinflationary process for now. While headline CPI could conceivably drop another tenth of a percentage point or two into the summer – helped perhaps by some further disinflation in food and services – other areas will be less helpful. Household energy bills, though set to drop by a further 7% in July, are currently having their peak negative impact on the annual rate of inflation and the negative contribution will diminish as the year goes on. We expect inflation to bounce around the 2% target for much of this year and potentially could creep back up to the 2.5% area into year-end.

Contributions to UK inflation and ING forecasts (YoY%)

Macrobond, ING calculations

For the Bank of England though, it’s services inflation that matters and for the second month in a row, this has come in higher than expected. Investors would be forgiven for feeling a sense of déjà vu after a very similar pattern emerged this time last year, and at the time markets became concerned that the UK had a considerably worse inflation problem than elsewhere.

Indeed at 5.7%, it’s now 0.4 percentage points above the Bank’s forecast from the May Monetary Policy Report. That all but confirms the BoE will keep rates on hold tomorrow. But it doesn’t necessarily change the game for August’s meeting. The things that kept services inflation elevated aren’t all necessarily telling us much about the underlying trend. Air fares rose more aggressively both in April and May than they did in the same months last year. Package holiday price rises did something similar, and these are areas that the Bank would typically say are driven more by noise than signal.

We’re therefore sticking to our call for the first rate cut to come in August, with a total of three cuts this year. We’ll still get another inflation report next month ahead of the August meeting. Any big surprises here could conceivably cause a further delay. But listening to Governor Andrew Bailey back in May, it sounded like he was keen to get on with the job of cutting interest rates. And a bit like the European Central Bank, the BoE seems more confident in its inflation predictions than it had been over the past couple of years. We’ll be watching tomorrow’s statement for signs that this confidence has been shaken by the latest data, or whether policymakers decide to play it down.

Either way, markets are pricing a 40% chance of an August cut and that seems much too low.

More By This Author:

FX Daily: UK Inflation Helps Sterling Ahead Of Bank Of EnglandThe Commodities Feed: Further European Gas Disruptions

Asia Morning Bites For Wednesday, June 19

Comments

Log in or sign up to join the conversation.