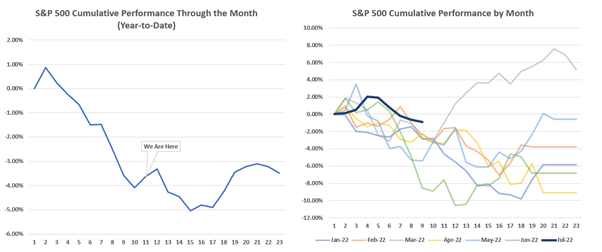

S&P 500 Bear Market Bounce To Close The Week

Despite the volatile FX action with the USD breaking out to fresh record highs and US inflation rising to a whopping 9.1%, prompting markets to shift towards a 100bps hike. Equity markets are closing out the week on a firmer note, halving their weekly losses. This is quite noteworthy that equities are taking this in their stride. However, as I have stated previously, the bias remains to fade bear market rallies. What’s more, based on the cumulative monthly performance of the S&P 500 this year, equities may continue to struggle next week. There is also plenty of catalysts that present a big risk for markets, most notably the ECB decision and whether Russia resumes gas flows through Nord Stream 1.

Source: Refinitiv, DailyFX

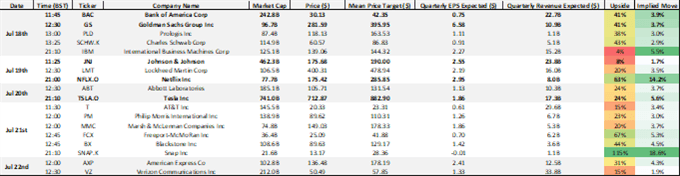

Elsewhere, US earnings will garner attention with Netflix and Tesla among the high-profile names to report, as shown in the table below.

US Earnings Calendar

Source: Refinitiv, Bloomberg, DailyFX

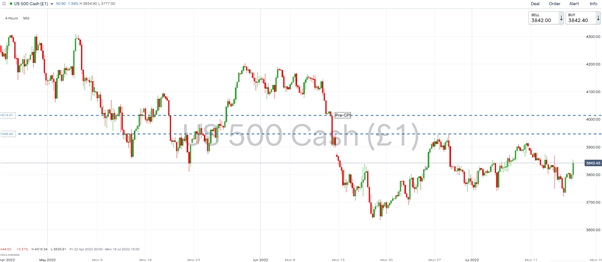

From a technical perspective, resistance is situated at 3900, with 3945-50 above. While the S&P 500 has eked minor gains so far for the month, the index is still some distance from being out of the woods. This will likely remain the case until we see a day of capitulation such as the VIX soaring to 40-45, or the Fed begins to pivot away from its extremely aggressive hawkish stance. On the downside, support resides at 3740.

S&P 500 Chart: 4-Hour Timeframe

Source: IG Charts

DAX 40 Russia Gas Flows, ECB Anti-Fragmentation Tool and Italian Politics Take Focus

European risk events will take centre stage next week. Firstly, the ECB is expected to deliver the first-rate rise since 2011. However, with the ECB essentially pre-committing to a 25bps rate rise, the focus will be firmly around their anti-fragmentation tool. As reports have signalled that discussions around a new instrument are ongoing, it has been hard to gauge whether the ECB will provide sufficient details on the size and how it will be deployed. Failure to do so, however, risks disappointing market expectations, weighing on risk sentiment and pushing the Euro lower. That being said, the ECB’s plan to contain peripheral spreads while raising rates has been made much more difficult after Italian Prime Minister Mario Draghi announced he would resign, raising the risk of snap-elections.

If that was not bad enough for the Euro Area, concerns remain over whether Russia will extend the disruptions of gas supplies to Europe via the Nord Stream 1 pipeline. As it currently stands, the annual maintenance of the pipeline is scheduled to end on July 21st. If Russia decides to extend the disruption of gas supplies, European equities alongside the Euro can be expected to come under significant pressure. On the technical side, downside momentum is likely to persist and while the YTD low has held, for now. Risk remains lower with a break through the YTD low opening up 12000.

DAX 40 Chart: Weekly Timeframe

Source: IG Charts

More By This Author:

Canadian Dollar Weekly Forecast: CAD At The Behest Of Crude Oil And Rampant U.S. DollarJapanese Yen Forecast: Will a Dovish BoJ Keep USD/JPY Rising? CPI in Focus Too

US Dollar Fundamental Forecast: DXY Set For More Gains On Ailing Euro, Yen

Comments

Log in or sign up to join the conversation.