VIX extended its Master Cycle low to the close on Friday, challenging the weekly mid-Cycle support at 13.95 and closing beneath it. Primary Cycle [B] appears to be over, or nearly so. While huge gains have been made by shorting Volatility, the Wave structure and Cycles suggest a strong reversal may be imminent.

(ZeroHedge) We discussed the collapse in the VIX earlier, when we pointed out that at least according to the world's largest bond manager, this artificial market calm foreshadows another surge in volatility just around the corner, which is also why Pimco's CIO had one recommendation: start selling now.

However, while Pimco may be accused of merely talking their book, there is another empirical indicator which suggests that a violent market reversal may be imminent.

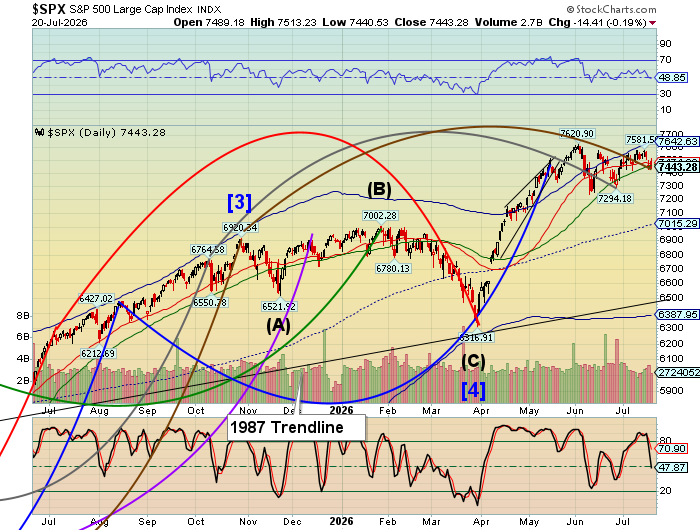

SPX rises above Long-term resistance

SPX rose above Long-term resistance at 2743.91 last week, completing 8 weeks of rally from the Christmas low. While there is a chance of reaching its Diagonal trendline at 2850.00, the Cycle is already stretched. The current period of strength may run out early next week.

(Bloomberg) It was a heck of a week, considering nothing much happened.

U.S. stocks just finished marginally higher for the past four days. The S&P 500 Index rose 0.6 percent, having not closed up or down more than 18 points in any session. In fact, the so-called fear gauge for equities, the Cboe Volatility Index, posted the lowest average reading in the past four months.

That won’t ring many alarm bells for investors. After all, the S&P 500 has gained 16 percent over the past nine weeks, so a pause is understandable. No cause for panic. Unfortunately, there are plenty of other reasons for that.

A menace was lurking in plain sight amid this sea of tranquility: Growth fears have sent so many investors into the safety of Treasuries now with benchmark yields not far from the lowest in a year. The term premium has collapsed. Bond volatility is evaporating. And the bad economic omens have appeared by the day.

NDX holds near Long-term support/resistance

While NDX rose above Long-term resistance at 70547.65, it has not made much progress this week. The Cycles Model suggests that any residual strength may run its course by early next week. There is a potential Head & Shoulders formation that, if triggered, may erase up to 3 years of gains. Stay tuned!

(ZeroHedge) One of the recurring market themes we have observed in recent weeks is that just because hedge funds have been painfully - if only from a P&L perspective - underexposed to the recent rally in the stock market, the "pain trade" is higher and that the higher the market rises, the more investors will be forced to enter the market. This thesis has been most aggressively pitched by JPM's Marko Kolanovic who believes that as VIX drops, resulting in greater leverage among the systematic community, the more buyers will emerge, creating a positive feedback loop that sends the market higher for the next three months.

And at least superficially, this take is accurate because as the following chart from Goldman Sachs Prime Services as of Feb 15 2019 shows, both gross and net hedge fund exposure is near the lowest level of the past 2 years. As noted earlier, in its latest hedge fund monitor publications, Goldman said that hedge fund gross exposures have rebounded modestly alongside the equity market "but remain well below levels registered during most of the prior 18 months", and adds that at roughly 230%, current gross exposures are similar to levels in late November 2018.

High Yield Bond Index tests a prior high

The High Yield Bond Index tested its December 4 high, coming within 12 ticks of matching it. The Cycles Model suggests that strength may be waning. The Broadening Wedge trendline at 196.95, if broken, may clear the way to a potential Head & Shoulders formation that may wipe out up to two years of gains in that period of time.

(Bloomberg) There are 1.2 trillion reasons for U.S. junk bond and leveraged loan issuance to stay relatively strong this year.

That’s how much money private equity firms globally had available to deploy as of the end of last year, a record level that’s 17 percent above 2017 figures, according to Preqin. The buyouts they’ll need to finance should keep U.S. issuance volume from plunging this year.

Treasuries may be done consolidating

The 10-year Treasury Note Index may have finished consolidating beneath mid-Cycle resistance at 122.54, closing beneath it. A breakout above mid-Cycle resistance at 122.54 now gives UST “permission” to rally to the Cycle Top in the next 4-5 weeks.

(Bloomberg) Traders in the world’s biggest bond market likely wished for some peace and quiet after the final weeks of 2018. From early November to the start of January, benchmark 10-year Treasury yields tumbled 70 basis points as investors flocked to havens amid a vicious stock market rout.

Now, almost two months later, they’re left to wonder if the $15.6 trillion market has become too quiet. Bank of America Corp.’s MOVE Index, which dates back to 1988 and tracks price swings on U.S. Treasury options, came within spitting distance of a record low this week. The index value touched 44.5 on Wednesday, close to the all-time low of 44 in November 2017 and another near-record of 44.3 in October 2018.

The Euro continues to drift

The Euro continues to drift beneath Intermediate-term support/resistance at 113.74, on a sell signal, but seemingly not interested in taking the bait. The Cyclical strength was used up attempting to test the Intermediate-term resistance at 113.74 early this week. A decline beneath the neckline may trigger the Head & Shoulders formation.

(Reuters) - France and Germany have agreed a detailed proposal for a euro zone budget to boost growth, strengthen competitiveness and lower the development gap between individual member states, a German government document showed on Friday.

The Franco-German accord is likely to pave the way for an agreement in the wider group of euro zone finance ministers who will discuss the set-up of the new but disputed tool next month.

“The purpose of the euro zone budgetary instrument would be to foster competitiveness and convergence in the euro zone...,” the joint Franco-German proposal read, according to the government document seen by Reuters.

EuroStoxx tests the Head & Shoulders neckline

EuroStoxx rose above the 7-year trendline near 3200.00 and appears to be testing the neckline of its Head & Shoulders formation. The period of strength in Stoxx is already waning. The Cycles Model forecasts 3-4 weeks of decline which may take it to the 2016 lows.

(Reuters) - Europe’s main share benchmarks rose marginally on Friday but company results including Sweden’s Elekta and France’s Sopra Steria drove big swings in stocks as investors awaited news from crucial U.S.-China trade talks..

The STOXX 600 and Germany’s DAX were up 0.2 and 0.3 percent respectively, with the main action at the share level.

Sopra Steria topped the STOXX 600, up 17.8 percent after the French IT services and consulting firm reported full-year results and said it was targeting an improvement in margins this year.

The Yen bounced at multiple supports

The Yen stopped its decline last week at the mid-Cycle support at 90.05 as well as Long-term and Intermediate-term support. Since then it has elevated briefly, then consolidated above support. The Cycles Model suggests a month-long rally that may go beyond the Cycle Top resistance at 93.71

(Bloomberg) The “sharply undervalued” yen is poised for a revival even after Bank of Japan Governor Haruhiko Kuroda surprised markets by warning of further potential policy easing, according to UBS Global Wealth Management.

The fund manager, among the biggest in the world, sees the yen gaining 5 percent to 105 per dollar in the next 12 months. Japan’s accelerating wage growth is bound to spur inflation, the company reckons, even as Kuroda said Tuesday that additional stimulus may be considered if the exchange rate affected the country’s economy.

Floundering world economic momentum could also see the yen benefit from haven demand, UBS GWM strategists, including Thomas Flury, head of currency research, said in a note to clients on Friday.

Nikkei surges above resistance

The Nikkei surged above mid-Cycle resistance this week, potentially making a potential inverted Cycle Top on Thursday. While the Cycles Model does allow for some residual strength early next week, the Wave/Cycle structure appears finished or nearly so.

(JapanTimes) Stocks turned lower on the Tokyo Stock Exchange Friday as profit-taking gained strength following four consecutive winning sessions.

The 225-issue Nikkei average fell 38.72 points, or 0.18 percent, to end at 21,425.51. On Thursday, the key market gauge gained 32.74 points.

The Topix index of all first-section issues edged down 3.98 points, or 0.25 percent, to finish at 1,609.52 after a marginal rise of 0.03 point the previous day.

U.S. Dollar declines, closes above Intermediate-term support

USD peaked last Friday, then drifted lower this week, closing above Intermediate-term support at 96.27. The USD may have set up a bull trap (a Cycle inversion), since the Cycles Model anticipates a month or more of decline, starting imminently.

(NYT) A cursory assessment might find the United States a less than ideal candidate for the job of managing the planet’s ultimate form of money.

Its public debt is enormous — $22 trillion, and growing. Its politics recently delivered the longest government shutdown in American history. Its banking system is only a decade removed from the worst financial crisis since the Great Depression. Its proudly nationalist president provokes complaints from allies and foes alike that he breaches the norms of international relations, setting off talk that the American dollar has lost its aura as the indomitable safe haven.

But money tells a different story. The dollar has in recent years amassed greater stature as the favored repository for global savings, the paramount refuge in times of crisis and the key form of exchange for commodities like oil.

Gold pulls back from the trendline

Gold challenged the Broadening Wedge trendline but closed beneath it for the week. This action offers a potential sell signal provided it remains beneath 1340.00. Both chart formations agree the low may exceed the prior one last seen in 2015.

(Reuters) - Gold rose on Friday en route to a second weekly gain as the dollar was subdued by weak U.S. economic data and hopes of a breakthrough in the U.S.-China trade dispute, with a darkening global economic outlook bolstering bullion.

Spot gold was up 0.3 percent at $1,327.40 per ounce by 2014 GMT, or about 0.5 percent higher so far this week.

U.S. gold futures settled down 0.4 percent at $1,332.80 per ounce.

The metal had fallen about 1 percent on Thursday following the release of minutes from the U.S. Federal Reserve's last policy meeting, which painted a less dovish picture than expected.

Crude rally meets resistance

Crude oil challenged mid-Cycle resistance at 57.63, but closed beneath it. The Cycles Model indicates this is an extension. Because the Cycle has been stretched, the reversal may come quickly and violently.

(OilPrice) Oil prices rose early on Friday, heading for a second weekly increase, driven up by optimism that the U.S. and China will forge a trade deal and that OPEC’s resolve to rebalance the market will outweigh soaring U.S. oil production.

At 08:00 a.m. EST on Friday, WTI Crude was up 0.98 percent at $57.52, while Brent Crude was trading up 0.61 percent at $67.60—with both benchmarks at their highest since November last year.

Although gains are capped by data that U.S. crude oil production hit 12 million bpd and American crude exports hit a new record high last week, market participants are hopeful that the U.S. and China can bridge the gaps in their ongoing trade talks.

Shanghai Index rallies above Long-term resistance

The Shanghai Index came back from vacation with a bang two weeks ago. The Cycles Model suggests the strength may wear off early next week. Once it declines back beneath Long-term support/resistance at 2708.53 it has the potential for a 500-point decline in the next month.

(ZeroHedge) President Trump's at times warm, at times contentious relationship with his Chinese counterpart has been an exercise in cognitive dissonance that's reflective of a broader truth about the relationship between the world's two largest economies. The veneer of economic cooperation belies deeper military tensions as China's expansionist military aims threaten US security in the Pacific.

Just last week, the top US Navy commander in the Pacific warned that China represents the “greatest long-term strategic threat to a free and open Indo-Pacific and to the United States." And the country's insistence on carrying on with its military buildup in the South China Sea, one of the most vital waterways for global trade, has angered the US and nearly all of its neighbors. But while the US public labors under the illusion that a military conflict with the Chinese is only a vague possibility somewhere off in the indeterminate future, for the island of Taiwan, China's increasing muscular military presence in the region is a daily threat that requires 24/7 vigilance, according to CNN.

The Banking Index stalls at mid-Cycle resistance

BKX ran out of strength on Wednesday as it stalled at mid-Cycle resistance at 100.52. The Liquidity Model has turned negative and may remain so for the next 4 weeks. The Cycles Model suggests the decline may resume to the retest of the December low over the next 4 weeks.

(ZeroHedge) As restrictive regulations (MiFid II forced the separation of banks' trading and research businesses) and intensifying competition from American rivals continues to hamstring once-proud European investment banks, SocGen is reportedly the latest continental titan preparing to dramatically reduce the size of its Global Banking and Investor Solutions unit - cuts that could include thousands of jobs - while the bank searches for a partner for its cash equity business (a strategy that has been embraced by other European banks as MiFid has changed the rules surrounding research and other typical i-banking functions).

One of the bank's unions said the bank's traders are bracing for some of these cuts, though the bank is still reportedly weighing which businesses will bear the brunt of the cuts. Shareholders who have punished the company over the past year - the bank's shares have largely missed out on the STOXX 600's 2019 rebound - bid its shares higher on Friday, with SocGen shares rallying more than 2% on the news.

(CNBC) New loans in China surged to a record high in January — and analysts say it could be a sign that government stimulus is “finally kicking in,” which may be good news for the economy.

The world’s second-largest economy expanded 6.6 percent in 2018, the slowest growth in 28 years.

The slowdown was in part due to official efforts to reduce alarmingly high debt levels which started three years ago. Clamping down on credit, in particular non-traditional forms of lending known as “shadow banking,” suppressed economic activity and pushed growth lower.

But the onset of the tariff war with the United States and the pace of the slowdown forced a rethink. Last year, authorities began taking steps to encourage banks to lend more, cut taxes and support small- and medium-sized companies.

(Bloomberg) In 2014, Massimo Balestra received a call from an employee at his bank, offering a risk-free investment “as secure as a wall safe.” The resident of a small northern Italian town ended up spending 6,945 euros ($7,876) on a diamond that he says he hasn’t seen since.

Balestra is one of almost 100,000 Italians who bought so called “investment diamonds” at the urging of their banks in a widespread arrangement that’s now the target of a criminal investigation by the country’s financial police, according to people with knowledge of the matter. Investigators allege that Italy’s biggest banks hooked up their clients with diamond brokers who sold them stones for as much as double their market price.

Police on Tuesday confiscated more than 740 million euros from UniCredit SpA, Intesa Sanpaolo SpA, Banco BPM SpA and one of its units, Banca Monte dei Paschi di Siena SpA as well as two diamond brokerages in connection with the case, according to a court document seen by Bloomberg.

Comments

Log in or sign up to join the conversation.