BOJ Governor Kazuo Ueda has repeatedly said that there are no changes to monetary policy planned for now, but the data line up is showing a different picture.

The BOJ announced it was conducting a review of monetary policy, which isn’t expected to be concluded until next year. Comments from the central bank have doubled down on the narrative that no changes will happen until that review is concluded. But, it’s not unusual that reality interrupts central bank plans.

The latest reports

This week has brought a trove of data from Japan in the lead-up to the release of inflation figures tomorrow. Many of them have surprised to the upside, taking both analysts and policymakers off guard. The results are so good, as a matter of fact, there is rampant speculation that PM Kishida could call a general election, making the announcement as soon as Sunday, following the G-7 meeting in Japan.

One of the key bits of recent data was the surprisingly good results in GDP in the first quarter. Annualized GDP came in at 1.6%, doubling the 0.8% expected. One of the biggest challenges that the BOJ has been dealing with, and the reason for keeping rates low, is generating “organic inflation”. Although 1.6% annual growth isn’t exactly stellar by most other countries’ standards, it is a radical change from the average previously, and could herald a change in BOJ policy.

The “good” kind of inflation

Japan suffered a bout of inflation recently, but it didn’t shake the BOJ’s easing because it was the “wrong” kind of inflation. What the BOJ was trying to achieve is the natural expansion in the monetary base that occurs when the economy grows. Economic growth implies faster monetary circulation, which raises prices. The problem many other central banks have is that the economy is growing too fast, with high speed monetary circulation. That means they raise rates to “cool” the economy.

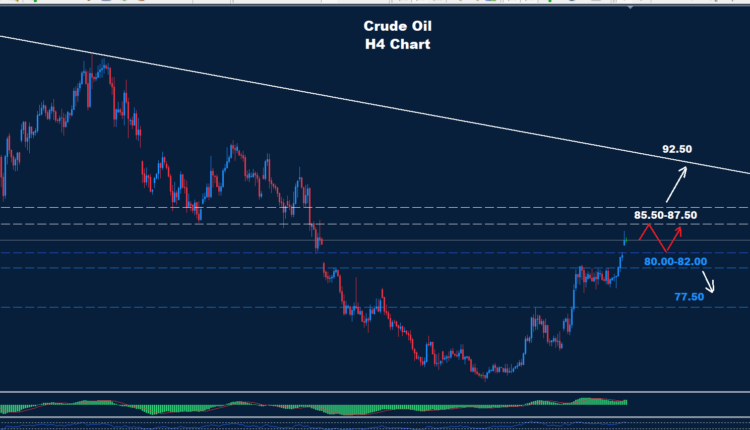

Japan’s persistently low inflation has been because of a lack of growth. The “accident” of high inflation last year was driven primarily by a sudden drop in the value of the yen, which precipitated price increases on domestic products. On top of that, fuel prices skyrocketed. Now that the yen is getting stronger and the price of crude is down, Japanese inflation has been coming down.

What is expected

While inflation is down, it’s still not back to target. Japan’s annual inflation for April is expected to remain unchanged from the prior month at 3.2%. Core inflation is expected to tick up slightly to 3.2% from 3.1%. The BOJ likely sees this still as the “wrong” kind of inflation, which implies its unlikely policy will change in response. The BOJ still expects inflation to keep going down, while holding prices steady.

The hiccup has been the increase in wages recently, strengthening Japanese consumer demand. Businesses have also recorded record profits over the last earnings season, which could be a sign that the economy is starting to grow again. Which means the “wrong” inflation could be replaced by the “right” inflation, and then the BOJ will be compelled to act.

More By This Author:

Intraday Analysis – WTI Tries To Gain Foothold

$70/Bbl Floor For Crude? US To Start Buying Oil

Intraday Analysis – Gold Tests Key Floor

Comments

Log in or sign up to join the conversation.