Image source: Pixabay

Sentiment showed some signs of positivity, with OAT spreads narrowing on the back of moderating comments from Le Pen’s party. Having said that, the fiscal challenges France is facing are structural and it’s difficult to see an election outcome that will help improve the fiscal picture.

Comforting words don't solve France's fiscal challenge

European markets showed some positive sentiment on Monday, and that in a week set for political restlessness and Friday’s pivotal US PCE reading. Sentiment was helped by the leader of the National Rally, who underlined the party’s aim to return France to budgetary reason – which was of course well received by OAT investors. He also stated that he would not challenge the EU’s interconnected power grid, a moderation of the more hostile tone versus the EU in the past.

In our view, such statements may help calm markets in the short term but they will not solve the structural fiscal challenge France is facing. The weakening fiscal picture has taken shape under President Emmanuel Macron’s rule, and we do not see an election outcome that could offer an easy fix to the deteriorating government finances. From a tactical perspective, we therefore remain cautious about buying into the French bond spread widening since the catalysts of a substantial retightening are hard to envisage.

So far, the spillovers to European Central Bank rate cut pricing have been small, suggesting that the market’s perception of the immediate risk of escalation of political risk is limited. In our view the tail risk from the French elections is actually coming from the left coalition (the New Popular Front), which is a lot less market friendly than Le Pen. Polls suggest little chance of a win, but given the second round may be a stand-off between the left and right, no outcome should be fully discounted. If the left manages to establish a significant share in Parliament, OAT investors could get more nervous and then any further market jitters could see more spillovers to ECB rate cut expectations.

EU plans moderated issuance over the second half of the year

The EU announced its plans to issue €65bn in bonds over the second half of the year compared to the €75bn it had pencilled in for the first half. A slowing of issuance activities had been anticipated following last year's pattern, and going by that, an even more pronounced decline would have looked possible. The amount for the second is now spread across four set windows for syndicated deals, one optional syndication window in December, and six auction dates.

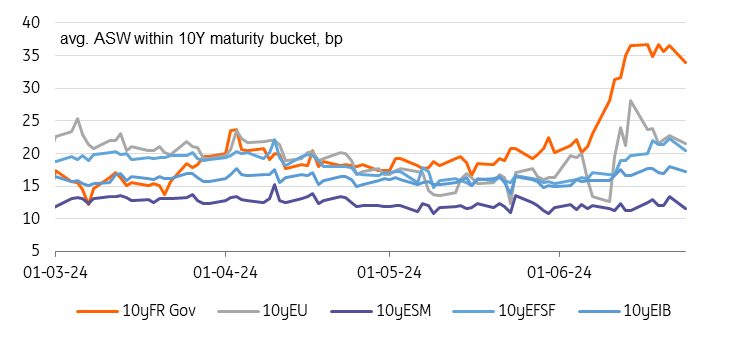

The spread levels of EU bonds had also come under widening pressure on the back of the French political turmoil, initially hit worse than its other European Supra peers which had seen a more gradual rewidening. Prospects of EU bonds being included into sovereign bond indices had sparked hopes of an expanded buyer base in the weeks ahead of the French elections, but these hopes were later dashed by one index provider (MSCI) shelving the idea for now. In the end, the outperformance versus France was down to the EU still trading more closely aligned to the SSA space.

ASW spreads of European Supras and French government bonds

Source: Markit, ING

Significant UST issuance in the same week as the PCE readings

US rates markets seem in a holding pattern until Friday’s core PCE reading, but should not forget about the significant UST issuance planned for this week. Just last week the CBO raised its deficit forecast for this year and beyond, drawing more attention to the longer-term supply outlook. The Treasury will kick-off with US$69bn in new 2Y notes today, followed by an additional US$142bn later in the week, so plenty of supply to absorb.

Today's events and market views

Data-wise, eyes should be on the US with the release of the Conference Board’s consumer confidence measure being the main focus. Since we think that next to cooling inflation a softening consumer story in the US should help nudge the Federal Reserve towards cutting rates in September, a dip below 100 would provide a bullish signal.

In primary markets, Germany and Italy will be active. Germany sells €4.5bn in 2Y bonds, while Italy will be selling up to €4.75bn also in shorter dated 2Y bonds as well as 6y and 15y inflation linked bonds. Over in the US, the Treasury will sell US$69bn in new 2Y notes.

More By This Author:

CNB Preview: Past And Future Inflation Perceptions Set The Pace Of Easing

FX Daily: Investors Struggle To Stay Bearish

Polish Construction Sees Another Lackluster Month In May

Comments

Log in or sign up to join the conversation.