The Bank of England’s reaction to the UK’s fiscal U-turn will be key to determining if Gilts can rally further. They are especially nervous about quantitative tightening and the outlook for rate hikes. The European Central Bank has yet to revise its growth outlook, and as long as that remains the case, Bund yields will struggle to fall.

What’s needed for Gilts to rally further

The announcements made by the new Chancellor Jeremy Hunt on Monday are significant both in terms of the revenue that will flow back into the Treasury’s coffers and in terms of the signal sent to investors. Not all of the fiscal hole identified by external auditors, said to be around £70bn per year by 2026-27, has been plugged, but investors are rightly cheering the change of direction, and of tone. We believe that most of the important news has now been delivered and that markets have had enough time to build a pretty good picture of the new fiscal state of play.

All this is to say that the focus should turn back to other actors, namely monetary policy. The announcements made by the chancellor yesterday will result in much higher taxes and lower government spending than the ill-fated "mini" Budget planned. At the time, the BoE warned that the, now mostly reversed, measures would mean higher interest rates for the economy. The main question now is whether the recent changes will prompt a dovish change of tone at the BoE. Without this, and if it persists with its plan to start outright Gilt sales as soon as 31 October, we think the period of extreme volatility in rates markets could well continue. If confirmed, the Financial Times report that the BoE will delay active Gilt sales would compound the good news from the fiscal U-turn.

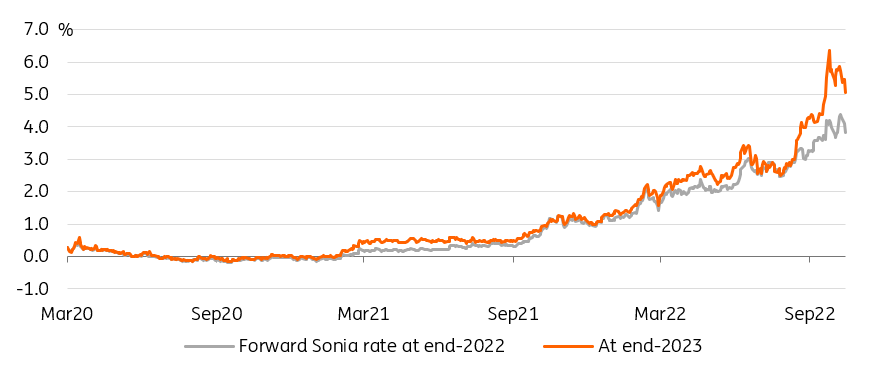

Gilts could rally a further 40-50bp, but this feels like a tall order without BoE help

At just around 4%, 10Y Gilts are a far cry from their early August levels of 2%. To put it bluntly, they won’t go back there any time soon. A rally below 4% is possible but will have to come alongside a sharp repricing of BoE hike expectations. As things stand, markets are still pricing a terminal rate of over 5%. In that context, Gilts will have a hard time rallying further. Much, then, depends on what the BoE says in the coming days and weeks. Our back-of-the-envelope calculation based on 10Y Bund and Treasuries suggests that Gilts could rally a further 40-50bp, but this feels like a tall order without BoE help.

Markets are still pricing a terminal rate above 5%, difficult for Gilts to rally in these conditions

Image Source: Refinitiv, ING

One last hurrah before the ECB goes quiet

The ECB’s pre-meeting quiet period starts this Thursday. A number of ECB speakers have come out in favor of a 75bp hike at next week’s meeting. This also remains the market’s favorite outcome, priced with over 90% probability. If this view is correct, as our economics team thinks it is, then this should leave the attention firmly on the economic outlook. There will be no update to economic forecasts next week but the ECB’s growth projections of +0.9% in 2023 are in stark contrast with our own forecast of a 0.8% contraction.

This matters because it is all well and good to hike rates into a recession, it is another matter entirely to hike while the recession is underway. All this is to say that the ECB’s tone on economic growth will play an important role in setting hike expectations for subsequent meetings, especially in 2023, and thus in setting longer-dated interest rates.

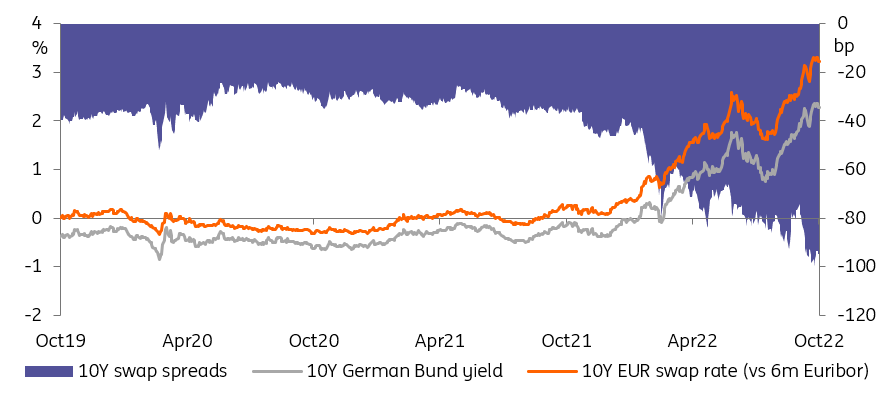

10Y Bund yields (just above 2.25%) are below where markets price the terminal rate

Currently, 10Y Bund yields (just above 2.25%) are below where markets price the terminal rate. Even without expecting much swap spread tightening next year, something that could happen on a combination of reducing excess liquidity, greater bond issuance, and quantitative tightening, this doesn’t seem like an excessively high level. A further drop in yields may well occur when the ECB eventually takes the knife to its growth forecasts but, in the meantime, we expect appetite to buy Bunds to remain limited.

Wide swap spreads are one factor keeping Bund yields well below the market's expected ECB terminal rate

Image Source: Refinitiv, ING

Today’s events and market view

The ZEW survey is the main item on the European economic calendar. The expectations component is due to fall judging by the Bloomberg consensus but it is the current situation that is expected to fall the most sharply, indicating that the widely-anticipated downturn is becoming a reality.

Supply includes 7Y bonds from Germany and 10Y/30Y from Finland, nothing too challenging to absorb.

The US releases feature industrial production and the NAHB housing market index.

Central bank speakers today include Isabel Schnabel of the ECB, Neel Kashkari, and Raphael Bostic of the Federal Reserve. Schnabel is widely seen as the most influential ECB member so any comment on recession risk (see section above) would carry a lot of weight for rates markets. This feels like too tenuous a hope in our view until the ECB has reached a deposit rate of around 2%.

More By This Author:

FX Daily: Corrective Forces Build

The Commodities Feed: Supply Tightness Vs. Demand Concerns

Key Events In Developed Markets For The Week Of Oct. 17

Comments

Log in or sign up to join the conversation.