Unabated central bank hawkishness is stoking recession fears and markets are pulling forward prospective tipping points. But it is the ECB that has yet to even lift off, suggesting it is EUR rates that hold the most upside near term. Bond spreads could become a casualty as outlines of the anti-fragmentation tool still underwhelm.

Hawkish posturing comes with increasing costs

Central bankers brandished their hawkish inflation fighting credentials in Sintra. The current economy should be able to stomach further tightening as the Fed's Powell stated. Sure, there is a danger of tipping over the economy, but the greater risk would be falling behind in the fight to curb inflation.

On the face of it such remarks should be outright bearish, but recession fears are starting to outweigh and curves flatten. And markets are bringing forward the prospective (economic) turning points. More specifically, in the US the hawkish posturing by Powell has raised implied rates of 2022 and early 2023 Eurodollar contracts, but beyond that the curve has actually bent lower. From a peak in early 2023 money markets are now showing a decline by around 50bp over the remainder of that year. The result yesterday was the entire US Treasury curve seeing a shift lower with the 5Y to 10Y area in the lead and the 2Y10Y curve briefly dipping to 2 basis points as it continues to flirt with inversion. It is a pattern that should become more entrenched if data delivers more indications of slowing growth dynamics amid persistently elevated inflation.

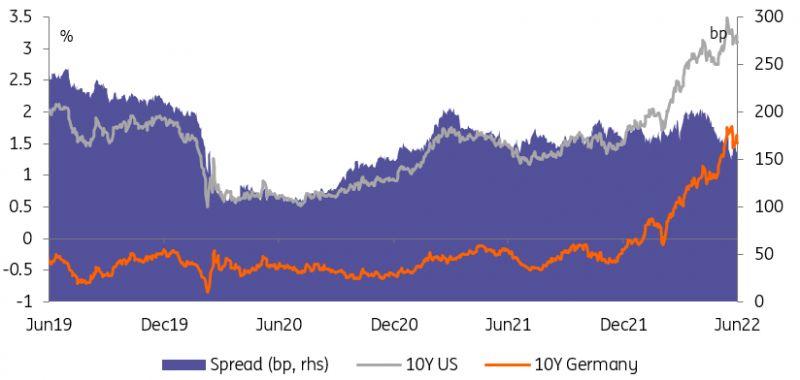

The ECB being further behind the curve means a tighter US-Germany spread

Source: Refinitiv, ING

The ECB has not yet reached peak hawkishness

More Council members have now floated the possibility of a 50bp hike at the upcoming July meeting. This hawkish twist was blunted yesterday by a slower than feared German inflation estimate. Admittedly, the bar for such a larger move from the European Central Bank appears rather high given its unusual explicitness regarding a 25bp hike in July, but curbing near-term hike expectations on the back of German inflation data may seem premature as data was heavily impacted by government relief measures. The contemporaneous surge in Spanish and Belgian inflation readings are a better indication of the direction of travel. And fiscal measures to dampen the impact of rising prices can even prove a two-edged sword as highlighted by the ECB’s Wunsch. Looser fiscal policies than envisaged by ECB forecasts may require an even more forceful tightening response.

As such we see yesterday’s rally of the Bund curve led by the 5y sector dropping almost 15bp by the end of the day also as a sign of recession fears gaining traction, inspired by US markets. The distinction being that unlike the Fed the ECB still has to start the actual delivery of rate hikes and may not even have reached its peak hawkishness just yet. With a potentially even more front-loaded tightening we think it is EUR rates that hold the most upside. They are more likely to see new highs than their US counterpart.

The ECB is still hesitant to take a bolder approach – be it reinvestments or the ultimate backstop

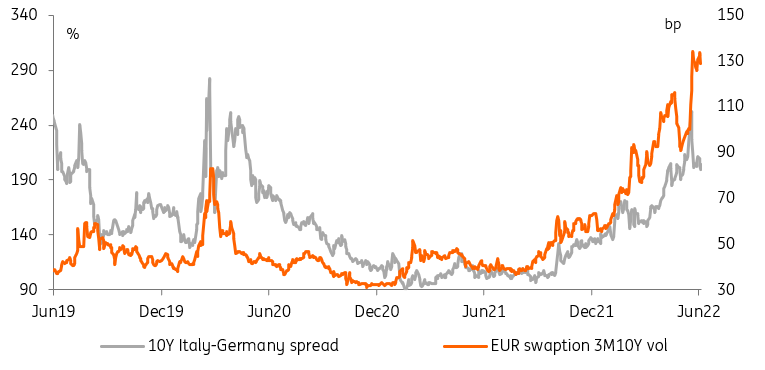

Pierre Wunsch’s remarks on the feedback loop between fiscal measures and ECB tightening lead over to the discussion surrounding the ECB’s anti fragmentation efforts – as he summed it up: “The end game is higher deficits and higher interest rates, and therefore also a higher risk of fragmentation”. The good news is that markets appear to take comfort in the more proactive approach taken lately by the ECB and are looking forward to the July meeting where a new instrument to serve as ultimate backstop for sovereign bond markets is expected to be outlined. The 10Y BTP/Bund spread has tightened further and is now closing in on 185bp and therefore its narrowest levels since late April.

Starting 1 July, Lagarde has announced the ECB will utilize the flexible reinvestments of the pandemic emergency purchase program holdings, which it still sees as its first line of defence against any unwarranted widening of bond spreads. Bloomberg reported that the ECB wants to give national central banks’ market operations desks ample leeway in refraining from providing bond targets or thresholds. Crucially though, the flexibility does not extend as far as allowing for the frontloading of purchases. This means desks will have to cope with (non-periphery) redemptions not necessarily coinciding with the need to intervene in the periphery. A more active management of redemptions – for instance reinvesting non-periphery redemptions in short dated bills – may create more flexibility in that regard but will have other undesired effects as duration is then shortened in these markets.

Thanks to the ECB, peripheral spreads have de-coupled from implied volatility

Source: Refinitiv, ING

Regarding the ultimate backstop, which is the upcoming anti-fragmentation tool, we remain underwhelmed by the rough outlines that are emerging from various leaks so far. A Reuters report yesterday suggested that spread backdrop could have a limited envelope and duration. For sure the ECB has to prove its new tool against potential constitutional challenges, but if either parameter is not perceived as being generous enough it can create more problems down the road. We still think the more the ECB is prepared to buy, the less it will end up having to buy.

Today’s events and market view

The recession fear narrative appears to have regained the upper hand and the impact of central banks’ hawkish posturing is having a reduced reach out the curve. US data today may well play into this theme, with personal spending data expected to show a drop in real personal consumption. Meanwhile the PCE deflator – the Fed’s preferred inflation measure – could rise to 6.4% year-on-year.

While yesterday’s rally of EUR rates may also signal recession fears the distinction to the US remains that the ECB still has to even kick off its tightening cycle. This morning French CPI data should serve as another reminder that a large task still lies ahead for central bankers and markets still have room to price in bolder action.

In primary markets Italy auctions a new 5Y bond while also reopening its 10Y benchmark and a floating rate note, in total for up to €7bn across all three lines.

Comments

Log in or sign up to join the conversation.