Rates Spark: Eyes On The Prize

Bunds and Treasuries were little changed by the end of the day. However that masks the fact that we are still in a highly uncertain and volatile environment - 10Y yields still traded in a 6 to 7bp range intraday. Today's US jobs data may add to volatility, but the overarching theme should remain central banks' drive to normalize policies.

Today's US jobs data holds downside risk, but no concerns for the Fed

Rates markets remain torn between bouts of flight to safety and the developed market central banks' ambitions to normalize policies in the face of accelerating inflation. Fed Chair Powell had just confirmed in his testimony to Congress that the Fed is next in line to embark on a series of rate hikes. In this context the US job market data would normally constitute a key data event - and source of volatility - as markets' hike expectations are formed. And indeed, the disappointing ISM non-manufacturing reading yesterday, in particular its employment component dropping into contraction territory, has added some spice to today’s release.

In the end though the Fed as well as markets may look through any disappointment in the jobs data today. For one the main issue since the pandemic is one of labor shortage rather than lack of demand. Second, inflation remains the overarching concern that is only aggravated by geopolitical crises, its impact on energy prices and prolongation of supply chain disruptions.

Today's US market report comes as the Fed has all but committed to hike in March

Source: Refinitiv, ING

Crucial ECB meeting lies ahead next week for EUR rates markets

EUR rates market are looking ahead to a crucial week, with the ECB meeting on Thursday. The ECB has by now entered a communication blackout period, but with the ECB accounts of the February meeting released yesterday one of the last messages to markets was a decidedly hawkish one. The last meeting did pre-date the latest geopolitical escalation which has since also triggered some more cautious tones by ECB officials, but the underlying push is to normalize policies if circumstances permit.

The ECB is likely to refrain from plotting out a concrete normalization path. Tightening policies amid high uncertainty and given the proximity of the conflict zone would be reckless. Still, postponed normalization is not a cancelled normalization. Unless we see severe flight to safety we think that 10Y Bund yields should remain in positive territory going forward, and even the 2Y Schatz yield should be closer to 0%.

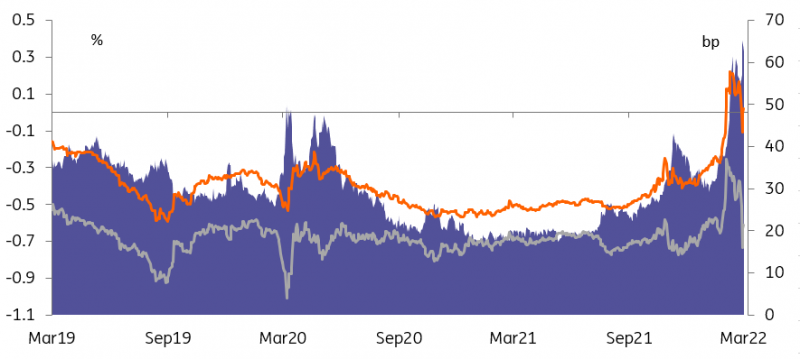

Bunds continue to trade rich versus swaps

However, the aforementioned German 2Y paper in particular has felt the impact of collateral scarcity which has prompted the German debt agency to intervene by adding €2.5bn to a €6bn bond maturing March 2024. The increased volume will be used for “short-term repo and securities lending transactions” to counter delivery difficulties seen in that security. Core investors have had to contend with collateral scarcity for some time already which in connection with a flight to safer assets has driven spreads versus swaps to record wides, but a later statement by the agency confirmed suspicions that sanctions and the freezing of assets are also aggravating the collateral scarcity issue.

The 2Y asset swap spread had made new highs yesterday. Though also at their widest levels since 2Q 2017, one should note that at least if spreads versus ESTR are considered, there was no push beyond recent peaks. This in turn means that the spreads of Euribor-based swaps versus overnight indexed swaps (OIS) have widened. In the 2Y tenor this basis has widened by more than 8bp to now 20bp since early February, the widest level since July 2020. That this is also happening as the ECB pushes towards normalization is no coincidence in our view. But Euribor/OIS spreads are a widely watched money market funding stress indicator that have also been on the move alongside cross currency basis swaps as the geopolitical crisis escalated.

Sanctions have contributed to a worsening of bond scarcity

Source: Refinitiv, ING

Today’s events and market view

The main event today is the release of the US jobs market data. Market consensus is looking for a payrolls increase of 415K, although the recent disappointing ISM services has flagged downside risks.

However, we think that Treasury markets should be focusing on the overarching policy normalization drive of the Fed as recently confirmed by Fed Chair Powell.

In the Eurozone the main data point is the January retail sales figures, though the relevance of such data for the further outlook in light of the geopolitical crisis and its impact on consumers via energy prices should be diminished.

Disclaimer: This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information ...

more